Image source: Pixabay

1Q24 GDP was weaker than expected

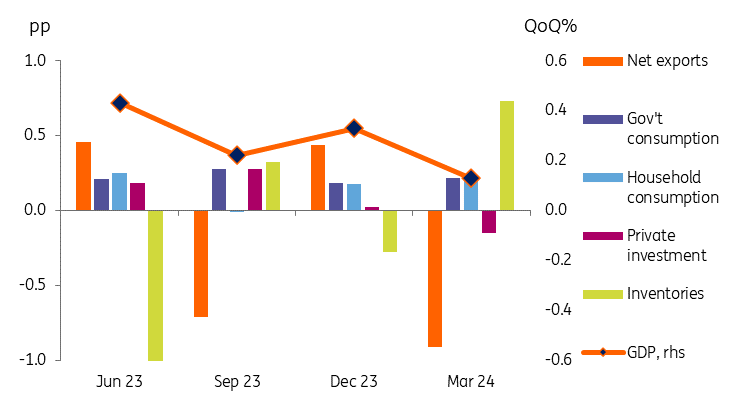

At just 0.1% QoQ, the first quarter 2024 GDP result continues a remarkably steady slowdown in sequential growth since the fourth quarter of 2022, when GDP grew at a 0.8% QoQ pace. There was an upward revision to the 4Q23 growth numbers, which now show 0.3% growth, up from an initially reported 0.2% figure. But the year-on-year growth rate still fell to 1.1% YoY, and further declines look likely in the coming quarters.

Contributions to QoQ GDP (pp)

Fixed investment declines

Although the net export figure was a much bigger drag this quarter (-0.9pp) than in 4Q23 (+0.4pp), we need to consider net exports together with inventories, as much of the import drag shows up as an offsetting inventory gain. When we do this, the combined inventory/trade contribution dipped from a positive 0.1pp boost in 4Q23 to a 0.2pp drag in 1Q24.

Household spending growth provided an ongoing, albeit small (0.2pp) boost to GDP. Household consumption remains weak, but it is not collapsing.

Private fixed investment was a more obvious culprit for the slowdown in the latest quarter. Investment provided no boost to growth in 4Q23 and deteriorated to a 0.2pp drag this quarter.

Until rates start to come down, the outlook for investment in Australia remains fairly bleak. And with inflation remaining much stickier than would be ideal, the prospects for any cuts this year look dim.

We stripped the last remaining rate cut from our forecasts this month, and are now waiting for further inflation data to consider how far back in 2025 to put the first cut, or even if we need to consider further hikes.

This isn't an ideal situation for the Reserve Bank of Australia (RBA). The RBA will take economic activity and the labour market into consideration when setting policy. But in the end, if growth is weakening, but inflation is beginning to rise again, it will be hard for the RBA to turn a blind eye to it and leave rates where they are. A slowdown in the inflation run rate - and soon - is needed to dispel thoughts that rates may not yet have peaked.

More By This Author:

Asia Morning Bites For Wednesday, June 4Services Lead Hungary’s Economic Recovery

Czech Wage Growth Increases Well Above Expectations

Comments

Log in or sign up to join the conversation.