Image Source: Pixabay

The Reserve Bank of Australia is likely to stand pat at next week's policy meeting. Plus, we'll get PMI readings from the region.

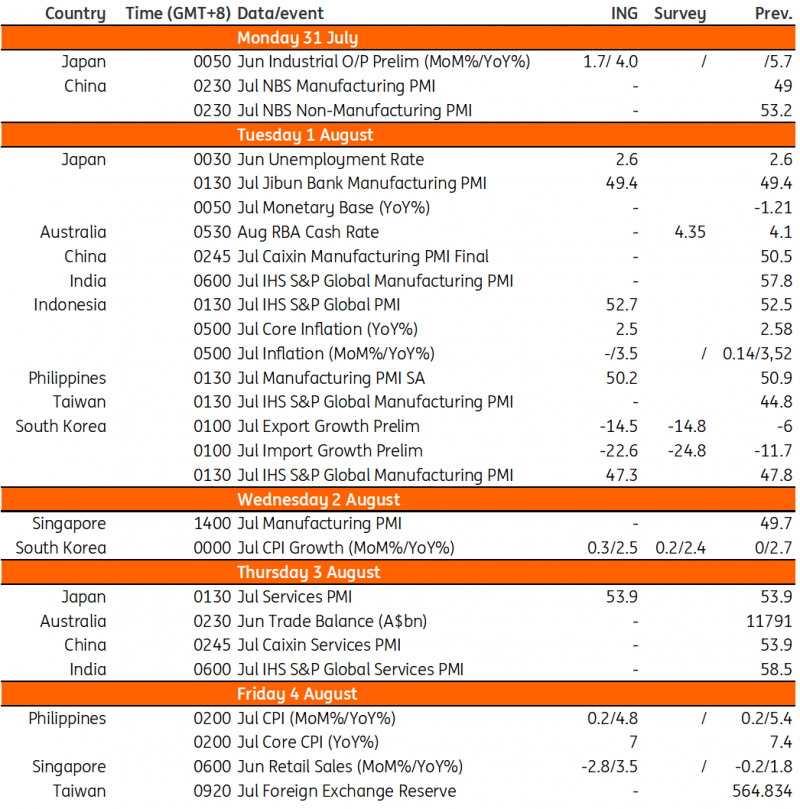

RBA likely to maintain rates as inflation slows

The Reserve Bank of Australia (RBA) can use the latest inflation data as an excuse to leave the cash rate target unchanged at 4.1% this month. But while the figures are being touted as “better than expected” the truth is that the monthly June figure was still running hot, and with base effects almost used up, there may well be more convincing periods in the months ahead for the RBA to deliver further tightening. Our current thinking is that the bank will maintain rates at the current level until September, which could respond to inflation backtracking higher, or just not making sufficient downward progress.

The latest data from the Australian Bureau of Statistics shows that the CPI for the second quarter fell to 6.0% year-on-year, lower than the 6.2% consensus. This is also the lowest quarterly rise since September 2021. As both headline and trimmed mean inflation are now below the central bank’s forecast, this gives it a good reason to believe that it is time to stop.

China's PMI likely lower again

Both the manufacturing PMI released by Caixin and the official numbers are expected to dip further as the government has yet to roll out any concrete policy to boost growth. While a weak yuan could provide a lift to the export sector, it also reflects the general pessimism that has taken hold in the economy. This has led to many consumers delaying spending; thus, we should see the services PMI also drop for a second month as the effect of "revenge spending" fizzles out.

Slowing global demand weighing on India and Taiwan

Last month showed the first decline in India’s manufacturing PMI after several months of expansion. This is a sign that India may be losing a little steam as rate hikes worldwide are finally impacting the global economy.

The shrinking global demand and semiconductor downturn also affect Taiwan, which has seen its PMI contracting for several months. We expect Taiwan’s PMI to remain in contraction.

Trade and inflation numbers from Korea

Korean exports are expected to decline for the tenth straight month on the back of sluggish semiconductor and petroleum exports. Export details to the US and the EU should be monitored more carefully, as this could signal how consumers cope with rate hikes.

Consumer inflation should stabilize further down to 2.5% year-on-year in July (vs 2.7% in June), mainly due to the high base last year. Meanwhile, recent floods and a rebound in global oil prices should push up food and energy prices on a monthly basis.

Japan reports activity data next week

Monthly activity data should be closely watched in order to gauge whether Japan’s recovery can be sustained in the second quarter. Surveys and other forward-looking data suggest that both industrial production and retail sales will gain in June, supported by solid catch-up demand and improvement in the global supply chain.

Indonesia’s inflation is likely steady while Philippine price pressures ease further

Both the Philippines and Indonesia will report inflation next week. Inflation in Indonesia returned to target earlier this year and we expect both headline and core inflation to remain well-behaved. Headline inflation should be flat at 3.5%YoY while core inflation could dip to 2.5%YoY from 2.6%.

Meanwhile, in the Philippines, headline inflation will continue its slide helped along by favorable base effects. Philippine inflation could edge lower to 4.8%YoY (from 5.4%) while core inflation could likely trend lower to 7.0%. Despite moderating price pressures, both Bank Indonesia and Bangko Sentral ng Pilipinas will likely keep rates untouched for the time being to provide support for their respective currencies.

Singapore retail sales could bounce in June

Retail sales, which have been a bright spot for Singapore’s economy, could extend their gains for another month. June retail sales could rise by 3.5%YoY although this will be down 2.8% from the previous month. Slowing inflation coupled with the influx of foreign arrivals should provide some support, especially in services related to leisure and recreation.

Key events in Asia next week

Image Source: Refinitiv, ING

More By This Author:

Goldilocks GDP Feeds The US Soft Landing Narrative

The ECB Switches Off Autopilot

ECB Hikes Rates By 25bp

Comments

Log in or sign up to join the conversation.