Image Source: Pixabay

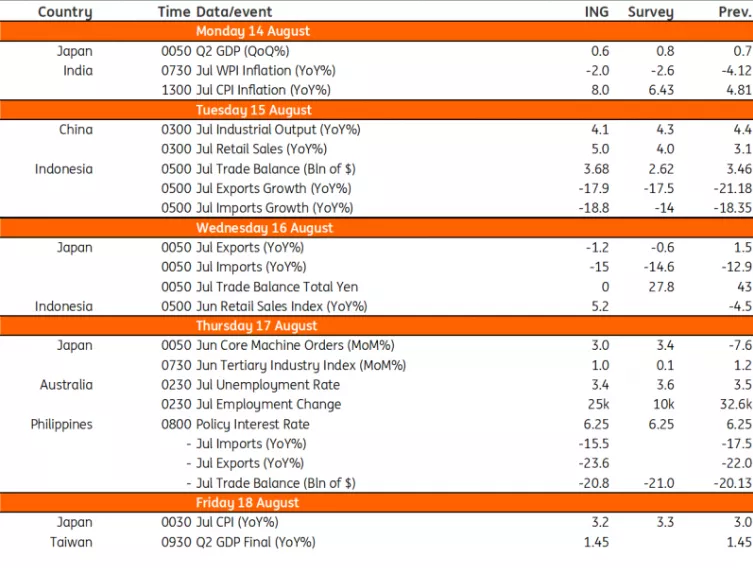

The week ahead features trade and inflation data from Japan, India, and China. We'll also get a Philippine central bank decision and Australia’s unemployment data, which could influence India's move on rates later this month.

Australia's unemployment rate to increase slightly

Australia’s unemployment rate came close to its all-time low of 3.4% last month, falling to 3.5%. Despite that, the Reserve Bank of Australia (RBA) kept rates unchanged last week as the inflation data was more favorable.

Although labor data is an important input into the RBA’s reaction function, we think that the central bank will continue to be subordinate to the monthly inflation numbers, which must grapple with large electricity tariff hikes in July and then much less helpful base effects between August and October.

Japan to release GDP, trade and inflation data

With modest improvement in net exports and a solid recovery in service activity, we expect second-quarter GDP growth to rise 0.6% quarter-on-quarter seasonally-adjusted (vs 0.7% in the first quarter).

For inflation, we believe that private consumption has cooled moderately as the high prices in the second quarter put off consumption demand, though this is likely to be compensated by improved terms of trade as imports fell sharply due to falling global commodity prices.

However, we should expect exports to record a contraction in July, particularly due to base effects. We believe Japan’s inflation should stay at the current level while core inflation is expected to accelerate further, as the previous Tokyo inflation outcome suggested.

Philippine central bank to extend rate pause?

The Philippines' central bank, Bangko Sentral ng Pilipinas (BSP), is likely to extend a pause, but persistent upside risks to the inflation outlook could give Governor Eli Remolona a reason to stay hawkish. Headline inflation has been trending lower and could be within target as early as September. This would be the main reason the BSP holds rates at 6.25%.

However, with global grain and energy prices inching higher, a fresh round of upside risks to the inflation outlook has surfaced. Persistent upside risks will likely translate to the central bank remaining hawkish even if the BSP opts to extend its current pause. We expect the BSP to keep rates untouched but signal a strong willingness to tighten further should upside risks to the inflation outlook materialize.

Inflation to surge in India

India will release its July CPI next week, and we are expecting a steep climb to over 8%, breaching the upper end of the Reserve Bank of India's (RBI's) 2-6% target range. This is due to soaring food prices caused by the erratic monsoon rains: tomatoes experienced a whopping 200% month-on-month increase in July. But this should not bother the RBI too much as food price shocks like this come and go.

The effect of food inflation has also spilled over to exports, where the Modi administration has announced an immediate ban on some non-basmati rice. As such, we are expecting a further decline in India’s export to -23.6%.

Key data on industrial production and retail sales from China

While China’s data has been disappointing lately, the summer season from July may usher in some better news. Data from China Railway show that there was a 14.2% increase in operating passenger trains compared to the same period in 2019. Flight numbers, on the other hand, experienced a slower recovery. They are currently running at about 48% relative to the same period in 2019, but this is still a 12% increase on a yearly and monthly basis. The rise in movement could provide a boost to consumption and strengthen retail sales.

However, the effect is unlikely to spill over into industrial production, and we should continue to see weak growth here. Both the official and Caixin Manufacturing PMI released earlier this month showed that China’s recovery has yet to gain traction.

Key events in Asia next week

Image Source: Refinitiv, ING

More By This Author:

U.S. Inflation Boosts Case For No Further Rate Hikes

The Commodities Feed: Supply Risks From Australia Push European Gas Prices Higher

Rates Spark: Energy And Food Inflation Is Ringing More Alarm Bells

Comments

Log in or sign up to join the conversation.