Image Source: Unsplash

Regional PMI readings and inflation reports will be the highlight for the coming week.

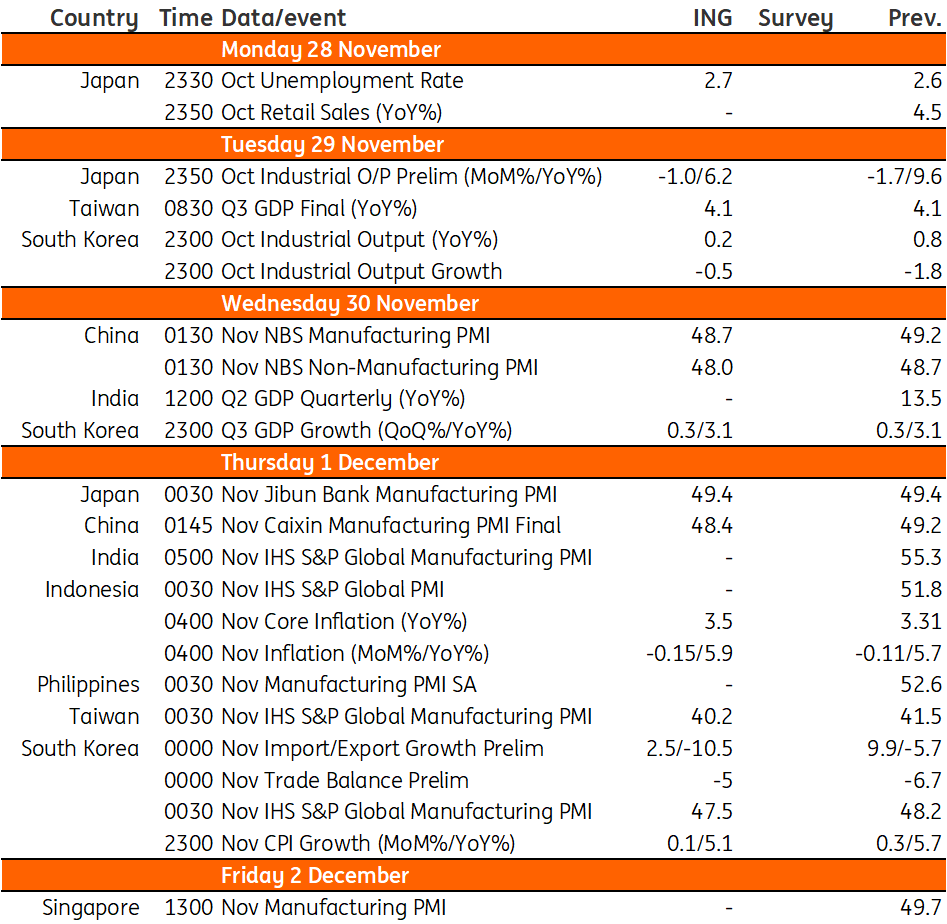

Regional PMIs

Both official manufacturing and non-manufacturing PMIs for China should be in a deeper contraction in October as the number of Covid-19 cases increased, affecting both factory and retail activities. This should also be reflected in the Caixin manufacturing PMI numbers which could show a bigger contraction, as smaller factories are more adversely affected given the challenging logistical situation.

Meanwhile, PMI indices for both South Korea and Taiwan should edge lower due to stalling demand for semiconductors from the US, Europe, and China.

Inflation from Australia, Indonesia, and South Korea

Next week we have Australia's October CPI inflation. Inflation data has typically only been released quarterly so this provides us with much more insight into the evolution of prices and provides much more timely updates than we have been used to. We think the outcome will probably be close to the recent month-on-month rate of increase, which would keep it roughly in line with the same period last year and leave inflation at about 7.3%. That could be interpreted as the peak, so markets may respond positively to that.

Inflation in Indonesia will likely pick up further, with core inflation likely accelerating to 3.5% year-on-year while headline inflation should settle at 5.9% year-on-year. Elevated price pressures have kept Bank Indonesia (BI) busy lately with the central bank recently tightening by 50bp. We expect inflation to inch higher in the coming months which could ensure that BI will stay hawkish going into 2023.

Meanwhile, inflation in Korea is expected to decelerate quite sharply to 5.1% YoY, mainly due to base effects. Fresh food and gasoline prices stabilized during the month while pipeline prices suggest a further deceleration in the coming months.

Growth numbers from India

India releases 3Q22 GDP data next week. The second quarter figure was buoyed by base effects and came in at 13.51%, which although admittedly very high, was a disappointment, and led us to downgrade our GDP forecasts. We have 6.3% YoY penciled in for the third quarter, as well as for the full calendar year 2023. Deficit data for October is also due, and will likely show that a modest improvement in India’s debt to GDP in 2022/23 remains on track. Something in the region of INR40,000 crore would be in line with recent deficit trends.

Other key data releases

In Korea, November exports will likely be disappointing as suggested by preliminary data reports. We expect a contraction of 10.5% YoY in November as semiconductor exports and exports to China remain sluggish. Slowing export activity should translate to industrial production contracting for a fourth straight month. Semiconductor and steel production will likely be a drag, but auto production should rebound.

In Japan, the jobless rate may edge up to 2.7% (vs 2.6% in September), but overall labor market conditions remain healthy. However, given the disappointing third-quarter GDP report, September industrial production is expected to drop 1.0% month-on-month, seasonally adjusted, with weak external demand pressuring manufacturing activity.

Asia Economic Calendar

Image Source: Refinitiv, ING

More By This Author:

FX Daily: Dollar Approaching Support Levels

Turkey’s Central Bank To Announce Additional Measures In December

FX Daily: Doves And Turkeys

Comments

Log in or sign up to join the conversation.