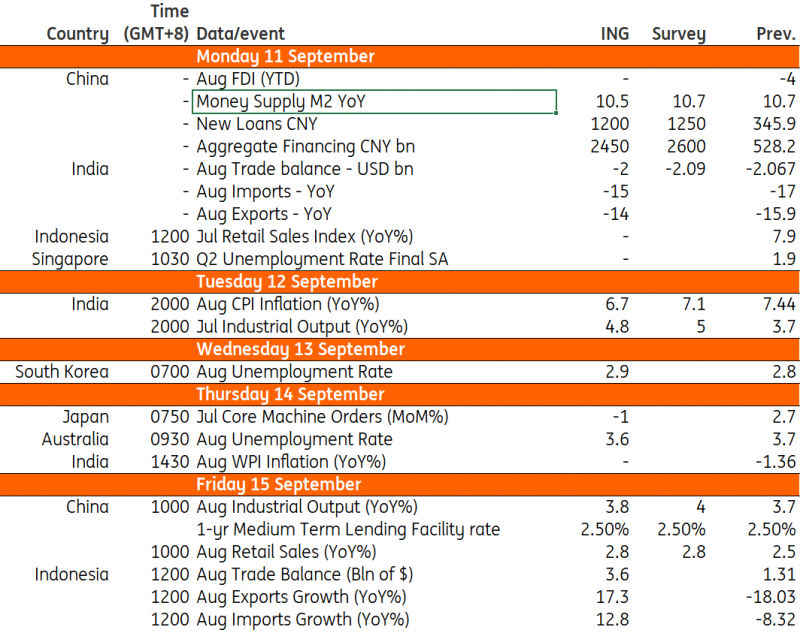

Next week is rather quiet, with only a few countries in the region releasing major data reports. China will be in the spotlight with several data releases, followed by India’s inflation number, Australia’s employment survey and Indonesia’s trade data.

China data dump: M2, industrial production, retail sales, aggregate financing

China will release a huge batch of data next week, the highlights of which will be industrial production and retail sales figures for August. Taking cues from the PMIs released recently, we could see a moderate improvement in industrial production at 4.8% year-on-year (from 3.7% in July). For retail sales, as it is approaching the end of the summer holiday season, we could see slower growth of 2.8% (from 2.5% in July).

India: CPI inflation

India’s inflation is likely to come down as prices of tomatoes have fallen by more than 50% month-on-month. However, the price of another crucial food staple – onions – shot up by more than 20% MoM. The net result of this is that the CPI inflation rate for August should slow to 6.7% year-on-year (from 7.44% in July) – still above the top of the RBI’s upper inflation target.

Australia: employment change, unemployment rate

Australia will release its labour report for August next week. We expect a partial reversal of the full-time job losses recorded last month, and some decline in the part-time jobs reading, resulting in a 15K increase in total employment. A similar partial reversal of last month’s unemployment surge, coupled with ongoing increases in the labour force, could see the unemployment rate dip back down to 3.6% after last month’s 3.7% print.

Indonesia: trade data

Exports and imports will remain in contraction for Indonesia while the overall trade surplus should improve slightly for August. Exports could fall by 17.3%YoY while imports could fall by 12.8%YoY. Resurgent global energy prices could impact both exports and imports with the overall trade balance registering at $3.6bn. The trade balance could provide some support for the Indonesian rupiah which has been under pressure of late.

Key events next week

(Click on image to enlarge)

Refinitiv, ING

More By This Author:

Key events in developed markets and EMEA For The Week Of September 11US Household Wealth Leapt $5.5 Trillion In The Second Quarter

FX Daily: Resistance To Dollar Strength Is Futile

Comments

Log in or sign up to join the conversation.