Image Source: Unsplash

Japan and Singapore will be releasing inflation numbers while the Bank of Korea and Bank Indonesia meet to discuss policy. Other highlights include China’s move on the LPR rates after a surprise medium-term lending facility rate cut.

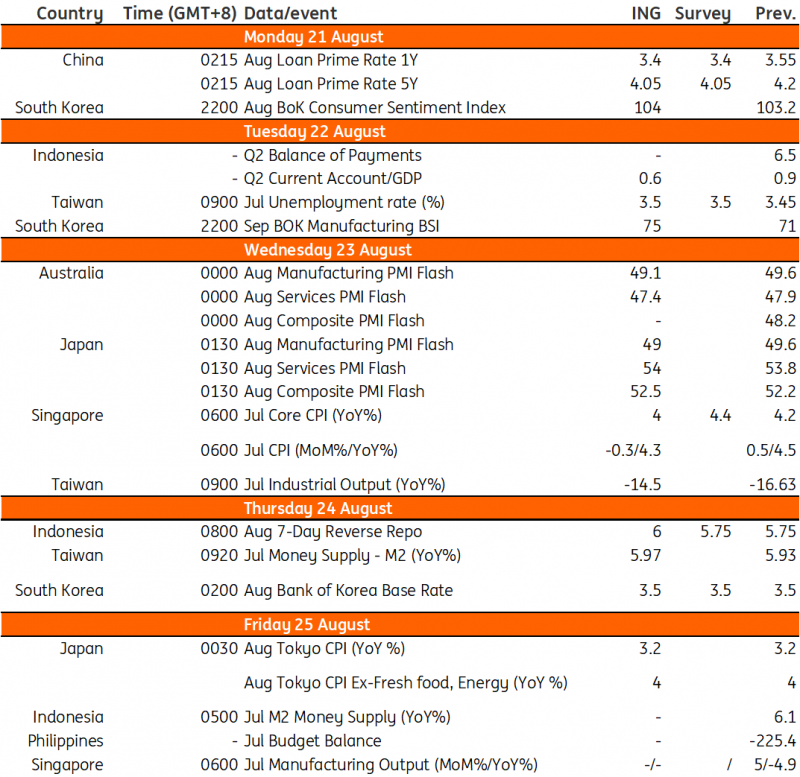

China to lower LPR rates after surprise medium-term lending facility (MLF) rate cut

The People's Bank of China (PBoC) surprised the market on Tuesday with an unexpected cut to its one-year medium-term lending facility loan rates by 15bp to 2.5%. This is the steepest cut seen in three years. The 7-day reverse repo rate was also lowered by 10bp to 1.8%.

This was likely carried out in response to disappointing activity and aggregate finance data. The 5-year and 1-year LPR are likely to follow suit with a 15bp cut.

Taiwan's industrial output and unemployment rate release

Taiwan’s exports for July fell by only 10.4% year-on-year, less than the consensus expectation of a 20.7% decline. Consequently, industrial output for July could come in lower than the consensus forecast of a 14.7% decline.

Taiwan’s unemployment rate reached a 23-year low in June. Given the weak growth so far this year, new graduates may have a more difficult time finding employment than in previous years, leading to a slight increase in the unemployment rate.

Korea expects to keep the policy rate

The Bank of Korea is expected to keep its policy rate at the current 3.5%. However, concerns over inflation by the BoK and a weaker won are expected to be the main reasons for reinforcing the hawkish stance.

Inflation is currently in the 2% range, but the base effect will be reversed in the coming months and will likely help nudge headline inflation higher. The recent KRW move should be a concern for the BoK, as it could push up inflationary pressures and heighten uncertainty in the financial market.

Tokyo CPI inflation is likely to steady

Tokyo's CPI inflation is expected to stay at the current level. With inflation in the 3% range and surprisingly higher-than-expected second-quarter GDP results, the Bank of Japan is likely to consider taking another minor policy change over the next few months.

We think that BoJ Governor Kazuo Ueda’s approach to the FX market will be different from that of the former governor. The continued weakness of JPY is a clear reflection of the yield gap which fails to address the recent solid recovery and relatively high inflation. Rising cost-push inflation may also hurt households’ consumption and investment recovery. The current JPY move does not justify the BoJ’s claim that FX reflects the fundamentals of the economy.

Singapore inflation to drop slightly

Inflation is still on a downward trend but will remain relatively high. July inflation could dip to 4.3% YoY, down 0.3% from the previous month. Meanwhile, core inflation will likely slip to 4% YoY.

Moderating inflation alongside disappointing second-quarter GDP growth numbers – which were revised lower recently – will likely prompt the Monetary Authority of Singapore to consider maintaining its current stance at their upcoming October meeting.

Bank Indonesia ready to resume rate hikes?

Bank Indonesia has kept rates unchanged since February since inflation remains well within its target band. However, given fast-narrowing interest rate differentials with the Fed (currently at 25bps), we believe BI will consider a rate hike at their next meeting.

Currency stability is a priority for the central bank, and Governor Perry Warjiyo believes a stable IDR will help him deliver his price stability mandate. Given a fading trade surplus and renewed pressure on the IDR, we believe there could be a chance for a rate hike next week.

Key events in Asia next week

Image Source: Refinitiv, ING

More By This Author:

FX Daily: Quiet G10 Markets Despite Chinese Turmoil

A Bond Bear Market Made In America

Tightness Takes Hold Of The Oil Market

Comments

Log in or sign up to join the conversation.