Image Source: Pixabay

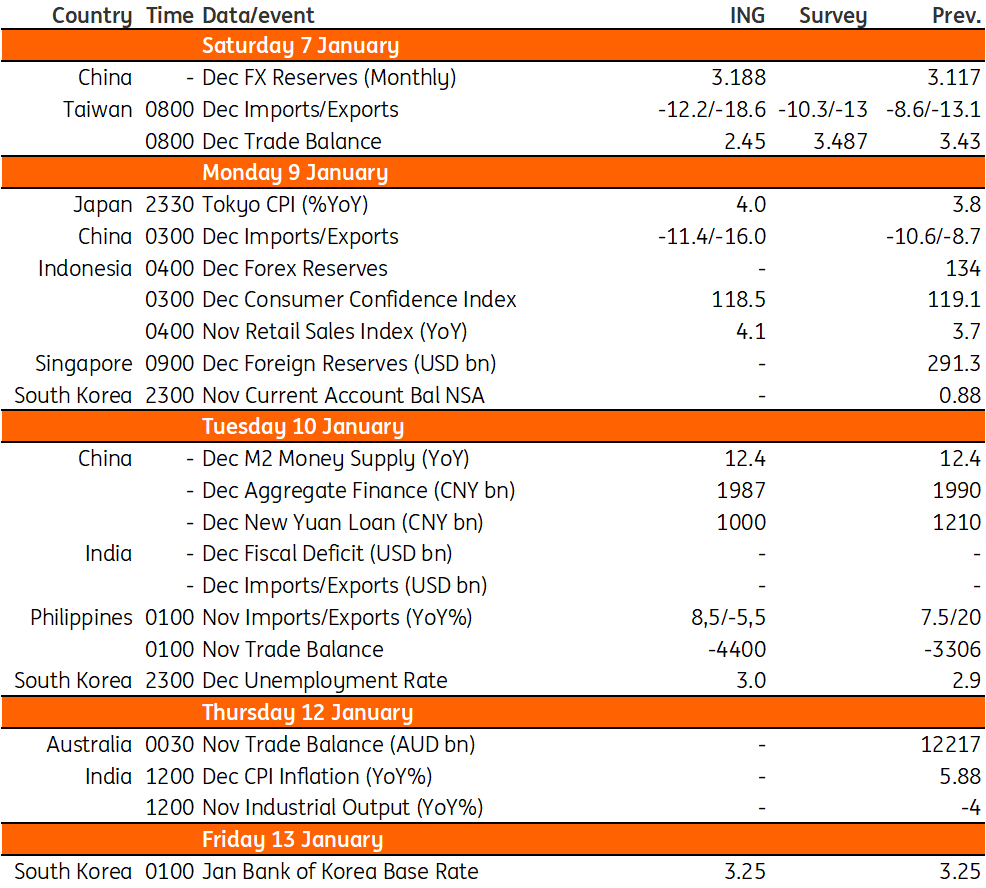

Next week’s data calendar features China's growth numbers, inflation readings from Australia and India, plus a key central bank meeting.

Is inflation finally on the downtrend?

The new monthly Australian inflation series should show a further small decline in the inflation rate to 6.8% year-on-year, down from October’s 6.9% rate – still too high for the Reserve Bank of Australia to stop tightening, but moving in the right direction.

And in India, further falls in food prices and stable gasoline should bring the price level down by 0.1/0.2% month-on-month, although similar falls last year mean that the inflation rate could hold up at around 5.9%YoY for a second month – still, within the Reserve Bank of India’s target range and indicating that we may be closing in on peak rates.

China activity and loan data due in the coming days

China will announce loan data between 9 and 15 January and activity data and GDP data between 10 and 27 January. Loan growth should have slowed in the last month of 2022 even after the People's Bank of China cut the required reserve ratio (RRR) to absorb liquidity. The impact of the RRR cut in December should be reflected in loan growth data for January and support economic activity post-reopening.

China also reports activity data and we expect retail sales to face a deeper contraction on a yearly basis. Meanwhile, industrial production could turn from positive growth to mild contraction in December. This suggests that growth was supported mainly by fixed-asset investments for the period. As a result, GDP growth for the fourth quarter of 2022 should fall into a slight year-on-year contraction.

BoK could surprise with a pause

Bank of Korea (BoK) will meet next Friday. The market expects a 25bp hike, but we maintain our minority view that the BoK will likely stand pat this time. Since the last meeting, both inflation and inflation expectations decelerated quite meaningfully while the Korean won stabilized under the 1300 level despite a widening yield gap between the US and Korea.

The BoK is expected to use the rate hike card more carefully as there is little room left to raise interest rates in this cycle given sluggish exports and economic activity. However, given the recent rise in gasoline and power prices, upside risks remain high and thus the BoK should retain a hawkish tilt despite the pause.

Philippines exports likely to reverse recent surprise gain

Exports are expected to revert to contraction following a surprise jump in the previous month. Electronics form the bulk of outbound shipments from the Philippines and given slowing global demand we could see the overall exports sector fall back into the red. Imports on the other hand should continue to expand, resulting in the trade deficit widening to roughly $4.4bn.

Key events in Asia next week

Image Source: Refinitiv, ING

More By This Author:

FX Daily: Seasonal Trends In Focus

U.S. Jobs Numbers Could Soon Start To Turn

Rates Spark: Champagne Hangover

Comments

Log in or sign up to join the conversation.