Image Source: Pixabay

Next week features several economies across the region reporting inflation and trade numbers. Meanwhile, China also reports its latest PMI readings and India releases GDP figures.

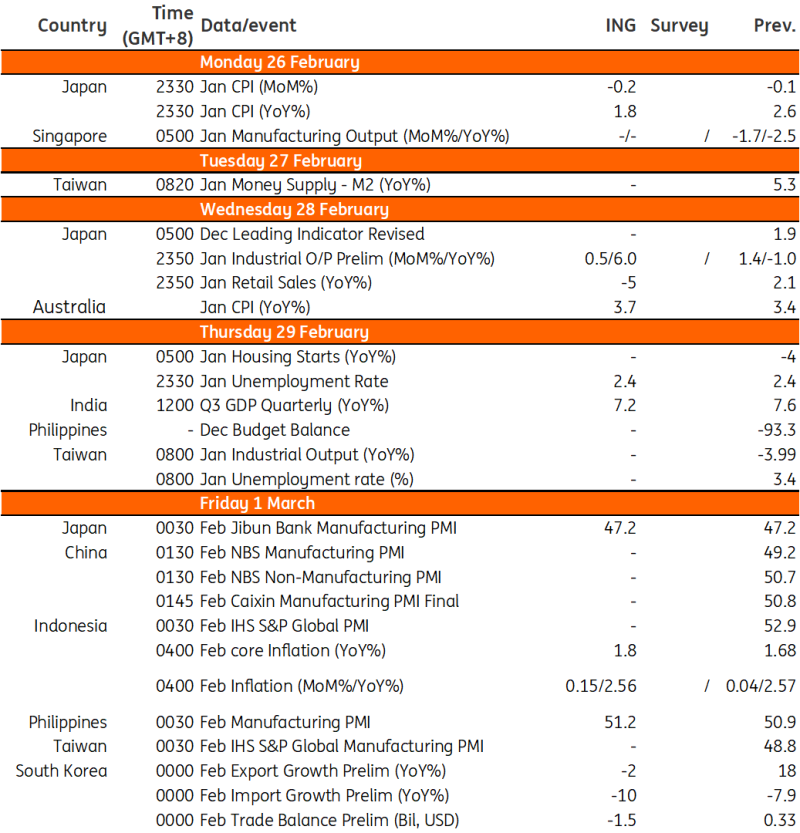

China’s PMI could remain in contraction territory

China's February PMI will be published next Friday. We expect the manufacturing PMI to remain broadly stable, dipping slightly from 49.2 to 49.1. The Lunar New Year effect could act as a drag on the February data as factories shut down for the break. This year’s eight-day holiday is also a day longer than normal. The PMI will likely come in below the critical 50 threshold for the fifth consecutive month, but the non-manufacturing PMI on the other hand should paint a more favorable picture. A strong recovery in travel and tourism over the Lunar New Year period bodes well for services sectors, and we expect an uptick from 50.7 to 51.0.

Australia’s inflation could tick higher

January’s inflation data will probably unwind some of the December decline, as we are not expecting a repeat of the big drop in prices that followed the December 2022 price spike. That should take inflation from 3.4% year-on-year to 3.7%, with a chance that it comes in even higher. With the Reserve Bank of Australia (RBA) mulling the need for further possible rate hikes at their February meeting, the narrative on rates in Australia may shift from when and how much the RBA will start easing back to whether rates have peaked after all.

India’s GDP growth to settle at 7.2%

Fourth quarter GDP data for 2023 will ease back from the 7.6% YoY rate in the third quarter, but should still deliver a respectable growth rate of around 7.2% YoY. That would also leave calendar 2023 GDP growth at 7.2%, the fastest growth rate of any major economy last year. Forward-looking indicators – together with another supportive Union budget for the coming calendar year – should maintain growth close to current levels in 2024.

Japan data deluge next week

Japan’s consumer prices are expected to drop quite sharply in January due to a high base last year. By expenditure type, service prices should slow down, partially offset by higher fresh food prices.

Given upbeat January exports results, we expect January's industrial production to rise modestly. The production disruption caused by the earthquake should have some impact, but this will probably be offset by strong output growth in vehicles and semiconductors. Retail sales, however, are expected to deteriorate based on an early vehicle sales report.

Lastly, Japan’s jobless rate is expected to remain unchanged at 2.4% in January, suggesting tight labor market conditions. We believe the upcoming data set will point to an economic recovery for the quarter.

Korea’s trade data

Early February trade data suggests exports momentum is continuing in February. The Lunar New Year holiday will likely skew the headline exports figures, but the daily average exports are expected to rise solidly. Semiconductors should remain the main driver.

Taiwan’s export’s likely to sustain momentum

January's export orders will be published next Tuesday. For December, we observed a recovery of actual exports to 11.8% YoY, but export orders saw a surprisingly large drop, down -16.0% YoY in Dec. With strong January exports continuing at 18.1% YoY, we expect an uptick in the export orders in this month’s data. The unemployment rate and industrial production data will also be published on Thursday, where we expect the moderate recovery trend to continue with a slight drop in unemployment and a recovery of IP.

Indonesia inflation likely to remain subdued

Price pressures in Indonesia are expected to remain manageable, with inflation likely to settle at roughly 2.6% YoY, up only by 0.2% from the previous month. Despite inflation staying relatively stable, Bank Indonesia's recently lowered inflation target (1.5-3.5%) suggests it may need to remain cautious and hold policy rates at current levels for now.

Key events in Asia next week

More By This Author:

Eurozone PMI Shows Improving Economy As Services Inflation Weighs On ECBThe Commodities Feed: US Crude Oil Inventories Exceed Expectations

FX Daily: FOMC Minutes Suggest Fed Is In No Rush

Comments

Log in or sign up to join the conversation.