Image Source: Pixabay

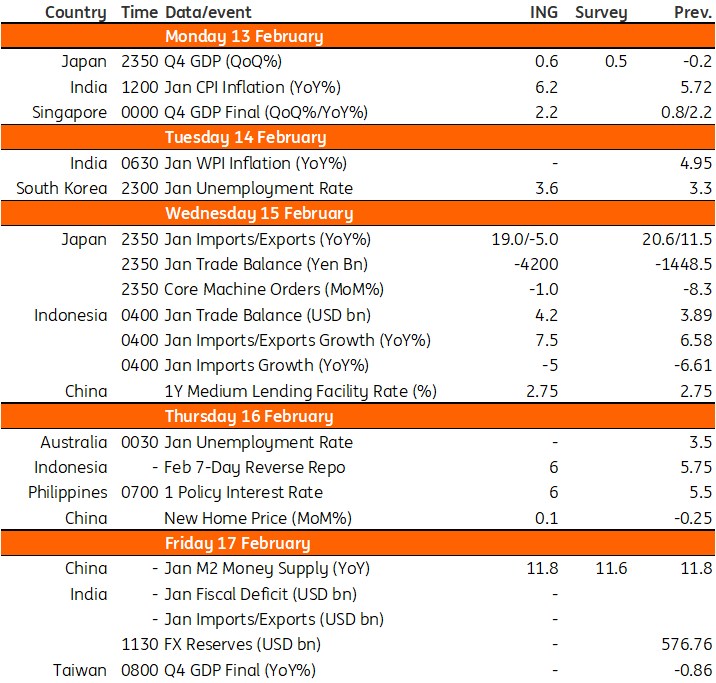

Next week’s data calendar features inflation readings from India, labor data from Australia, Japan’s latest GDP report, and rate decisions from China, Indonesia, and the Philippines.

India’s inflation number to set the tone for RBI rate decision

India's January inflation will probably move higher (6.2%) after the 5.7% year-on-year reading in December. But what will be watched more closely after the latest hawkish central bank statement from the governor, will be the core CPI inflation measure? Any indication that this has moved below 6% could be significant for the Reserve Bank of India's policy, though we think despite a small decline, the ex-food and beverages inflation rate will remain just above 6% YoY.

Unemployment rate key for future RBA policy

January employment data for Australia will add to the balance of knowledge surrounding future Reserve Bank policy. However, it will have to show a further marked deterioration, following last month’s part-time driven decline in employment and rise in the unemployment rate, to offset the RBA’s new-found hawkishness.

After last month’s decline in part-time work, we will probably see that part of the survey moderate, combined with perhaps a smaller increase in full-time jobs of about 10K to deliver a total employment change of 15-20,000. If that is broadly right, we may see the unemployment rate edged up to 3.6% - still very low by historical standards.

GDP data from Japan

Japan’s fourth quarter GDP data will be the highlight of next week. We expect the economy to recover from the previous quarter’s contraction, led mostly by private consumption and investment. The reopening and government travel subsidy programs should lead to a great improvement in hospitality-related activities. However, due to high inflation, the rebound will likely be limited to 0.6% (quarter-on-quarter, seasonally adjusted).

Meanwhile, core machinery orders are likely to shrink again in December amidst weak global demand conditions. Japan’s export growth is also expected to drop in January as the early trade data has suggested. We believe that Japan’s decision to join the US’s tech export ban to China will probably have a negative impact on Japan’s exports.

Weak jobs data expected from Korea

Korea’s unemployment rate is expected to continue to rise to 3.6% in January (3.3% previously) on the back of a slowing economy. There have been several news reports on job losses, mostly from the IT and finance sectors. This could also be due to severe weather in January, where agricultural and construction-related employment has been negatively impacted.

China to gauge economic reopening before adjusting policy stance

The People's Bank of China will announce the 1Y Medium Term Lending Facility (MLF) interest rate next Wednesday. We expect no change to policy as the economy has started to recover. The central bank should take time to observe the pace of recovery and determine if there is a genuine need for further cuts to the policy rate and Required Reserve Ratio.

Meanwhile, new home sales should show a stable month-on-month change as we have seen a slight price pick up in tier-one cities like Beijing, Shanghai, Guangzhou, and Shenzhen while home prices of lower-tier cities were still sluggish.

Indonesia to see a rise in trade surplus

Recent trends within Indonesia’s trade sector should extend into another month. Exports will likely remain in expansion while imports are expected to contract. This will result in the trade balance remaining in surplus of roughly $4.2Bn. The projected trade surplus however will be lower than the highs recorded in 2022 with the current account possibly slipping back into deficit territory.

Regional central banks look to tighten policy further

Bank Indonesia (BI) is scheduled to hold its second policy meeting for the year. BI Governor Perry Warjiyo has hinted that this current rate hike cycle could come to an end if inflation were to slow and the Federal Reserve were to turn more dovish. BI could still opt to hike by 25bp next week given renewed hawkish signals from the Fed while also ensuring core inflation heads much lower before pausing.

The Bangko Sentral ng Pilipinas (BSP) will also meet next week to discuss policy. After the blowout January inflation report, we believe that the central bank has no choice but to hike policy rates to combat above-target inflation. Governor Felipe Medalla has previously hinted at a potential shift in tone, but surging price pressures will likely mean that he doubles down on the hawkish rhetoric by hiking rates 50bp.

Key events in Asia next week

Image Source: Refinitiv, ING

More By This Author:

FX Daily: The Waiting Game Is On

Riksbank Hikes By 50bp Amid Concerns About Weak Krona

The Commodities Feed: U.S. Oil And Product Stocks Grow

Comments

Log in or sign up to join the conversation.