Image Source: Pixabay

The coming week features inflation reports from China and India plus Australia’s labour data. Japan also reports first quarter GDP and we have two central bank decisions to look out for.

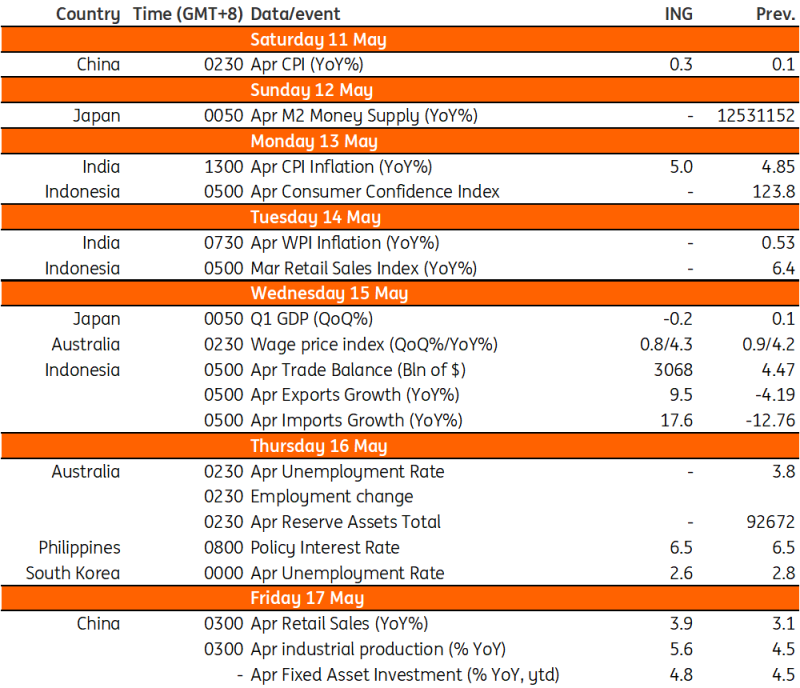

India's inflation to inch higher?

April inflation may creep higher again after the slight decline in March on lower gasoline prices and could touch 5.0% year-on-year again. This is still below the upper limit of the Reserve Bank of India's inflation target (6%) and reflects a mix of seasonal food price increases partially offset by the lower retail gasoline prices in March, which may partially spill over onto the April data. There are no rate policy-relevant ramifications from this.

Australia's labor report out next week

The quarterly wage price index for the first quarter of 2024 could show a slight decline in sequential growth (0.8% quarter-on-quarter from 0.9% in the fourth quarter of 2023), as hinted at in the Reserve Bank of Australia's recent statement. This noted that wage growth had peaked. However, the annual rate of wage growth could still tick higher as the first quarter growth rate in 2023 was quite weak. We look for the annual growth rate to rise to 4.3% YoY from 4.2%. April labor data will also be published. This is volatile data and even the trend is hard to fathom. Any substantial deviation from the median forecast could be leaped upon by traders looking for direction after the latest “anything is possible” RBA statement.

Japan's GDP report

This year's first quarter GDP should be the highlight of the week. It is expected to contract 0.2% QoQ seasonally adjusted mainly due to the production disruption in January and February as a result of the safety scandal. Monthly data showed a gradual normalisation from March, but overall the interruption is likely to distort not only production but also investment. Private consumption should improve on the back of better goods and services spending.

China's inflation and central bank meeting

The week ahead features many of the major data releases for China. First up is the CPI and PPI inflation data over the weekend. We’re expecting CPI inflation to trend a little higher to around 0.3% YoY, remaining in positive territory for the third consecutive month. Inflation is likely to remain low in the second quarter of 2024 before picking up more noticeably in the second half of the year. China’s credit data will be released as well, and here we are looking for a continued slowdown of aggregate financing and new RMB loans as loan demand remains tepid. M2 growth will likely remain little changed from last month’s 8.3% YoY. Finally, China’s major economic activity releases will be out next Friday, where industrial production, retail sales, and fixed asset investment are all expected to see a small increase in YoY growth in April. Markets will be watching the housing price data release closely, and given recent growing optimism, we could see a bottoming out of property prices in tier one and two cities. We expect that second quarter economic growth should remain above target, buoyed by a favorable base effect and policy rollout.

In terms of monetary policy, the People’s Bank of China’s medium-term lending facility rate decision is also due next Wednesday. We are looking for no change in the rate this month. The Politburo meeting at the end of April signaled that interest rate cuts are on the table – but a reserve requirement ratio might still be the preferred first option, despite its diminishing effectiveness in stimulating the economy. This is because it would not worsen the interest rate differential between China and its global peers, and would therefore avoid adding to RMB depreciation pressure. A surprise cut could signal weaker-than-expected April data.

Philippine central bank likely to hold rates

Bangko Sentral ng Pilipinas (BSP) meets next week to discuss policy. We expect the central bank to stand pat again and keep rates at 6.5% after April inflation came in slower-than-expected but growth numbers disappointed.

Key events in Asia next week

Refinitiv, ING

More By This Author:

FX Daily: Sterling On The Edge

The Commodities Feed: US Crude Inventories Edge Lower

Asia Morning Bites For Thursday, May 9

Comments

Log in or sign up to join the conversation.