Image Source: Pixabay

Next week features inflation readings from Australia and Indonesia plus several reports from China, Japan, and Korea. The Bank of Japan also meets to discuss policy.

Quiet week for greater China

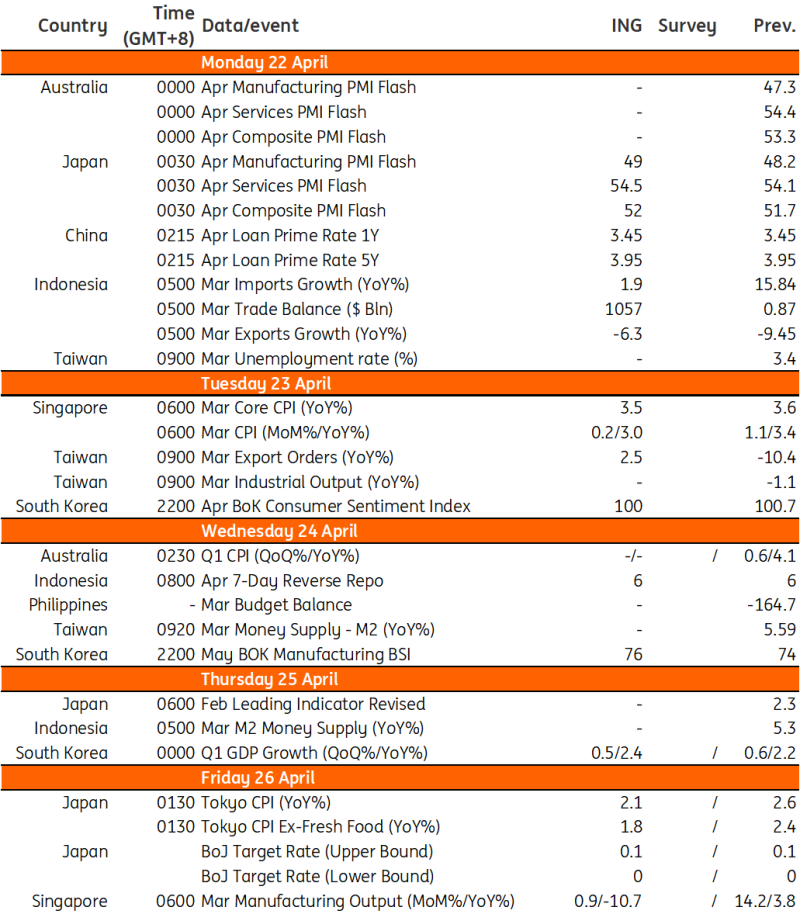

It looks like a relatively quiet week ahead for China after some major releases this week. The People’s Bank of China’s loan prime rate update will be on Monday. Given the recent stronger-than-expected economic data, ongoing efforts to stabilise the yuan, and the earlier MLF decision, we expect one-year and five-year rates to remain unchanged at 3.45% and 3.95%, respectively.

In Taiwan, export orders and industrial production data will be published on Tuesday. We expect export order growth to recover to positive territory after a sharp drop in February. Separately, Hong Kong will publish its inflation and trade data on Tuesday and Thursday.

Australia CPI inflation

Australia’s April CPI index likely rose by 0.5% month-on-month. This will leave annual inflation at 3.4% for a fourth consecutive month, just above the Reserve Bank of Australia's 2-3% inflation target. Markets have been scaling back their bets on RBA cuts this year, but this could encourage easing expectations at a time when US Federal Reserve rate cut expectations are being scaled back.

Flurry of data from Japan: PMI, Tokyo CPI, and the BoJ meeting

We believe that strong wage negotiations and solid demand for IT and automobiles are likely to push up the upcoming PMI numbers, supporting our view of a cyclical recovery in the near term.

Tokyo CPI should remain choppy. Headline inflation is likely to cool quite sharply to below 2.0% year-over-year mainly due to last year’s high base though we expect it to rebound again in May. Slower CPI inflation could give the Bank room to pause on its decision to raise rates for a few more months.

We expect the BoJ to keep its policy target unchanged, but the market’s focus should be on its quarterly outlook report. Given higher inflation in the first quarter, stronger-than-expected wage growth, and a weaker-than-expected yen, we expect the inflation outlook to be revised up, while car-related production disruptions could lead to a slight downward revision to growth. We believe that the BoJ’s rate hike expectations will grow as the year progresses.

India’s PMI could pullback

India’s April manufacturing PMI is due a slight statistical pullback from the current level of 59.1 after three months of gains, but this doesn’t merit any concern and should still be consistent with strong growth. We expect the service sector PMI to remain close to the 61.2 level recorded for March.

Korea: CSI, BSI, and GDP

This week, we will have survey data from Korea. These surveys were conducted before the Iran/Israel dispute and the re-acceleration of the Korean won's depreciation, so the results do not reflect recent events. With weak asset markets and fresh food and gasoline prices rising, consumer confidence is likely to slide again but the CSI index may remain above the neutral level.

Meanwhile, we expect manufacturing sentiment to rise on the back of strong global demand for IT, but non-manufacturing sentiment is likely to weaken as domestic demand conditions remain sluggish. This trend will be well echoed in the 1Q24 GDP data. We expect GDP growth to moderate only marginally from 0.6% quarter-on-quarter (seasonally-adjuted) in 4Q23 to 0.5% in 1Q24. Exports should remain a growth driver, but construction and investment may drag down overall growth.

Singapore inflation

Singapore reports March inflation next week. We expect core inflation to stay elevated at 3.5% YoY, although this will be slightly slower than last month’s 3.6%. This should keep the central bank on notice and we continue to expect the Bank to extend its pause with any tweaks only likely possible by the October meeting.

Key events in Asia next week

Refinitiv, ING

More By This Author:

National Bank Of Hungary Preview: Now Is Not The Time To Surprise MarketsFX Daily: Prospects Grow Of Joint Asian FX Intervention

Rates Spark: Differing Degrees Of Decoupling

Comments

Log in or sign up to join the conversation.