Image Source: Pixabay

Concerns over escalating US-China trade tensions are rising as China hits back against US tariffs with retaliatory measures. South Korea's January unemployment data and a rate decision in the Philippines will also be in focus over the coming week,

China: Retaliatory measures, still leaving room for de-escalation

The big thing to watch in the coming days is if and when China and the US hold their high level meeting. At the time of writing, the US has implemented an additional 10% tariffs on Chinese goods entering the country, though exemptions on goods already in transit could take some time before the first products are actually subject to these new tariffs. China has also announced retaliatory tariffs set to take effect on 10 February, which seems to open a short timeline for potential talks to de-escalate.

In terms of data releases, China will release its January CPI inflation data on Sunday morning. We're expecting a modest uptick in the year-on-year number to around 0.4% YoY, as we expect food inflation to see an uptick from the Lunar New Year effect, but non-food inflation is likely to remain weak as price competition remains cutthroat. The People's Bank of China is also set to publish January’s credit activity data sometime in the next week.

South Korea: Unemployment data amid a quiet week

The unemployment rate is expected to have fallen in January. We think the domestic political situation has stabilised, while Lunar New Year-related jobs may have increased before the long holiday at the end of January. In addition, the government's efforts to support growth may have led to an increase in public service jobs at the start of the new fiscal year.

Philippines: Inflation in the target range, forecasting a 25bp rate cut

January CPI inflation stayed well within the Bangko Sentral ng Pilipinas (BSP) target band of 2-4%. The real policy rate at 2.5%+ remains high, especially when GDP growth is expected to remain below the government’s target of 6-7%. Overall, we expect the BSP to cut again by 25bp in its upcoming policy meeting.

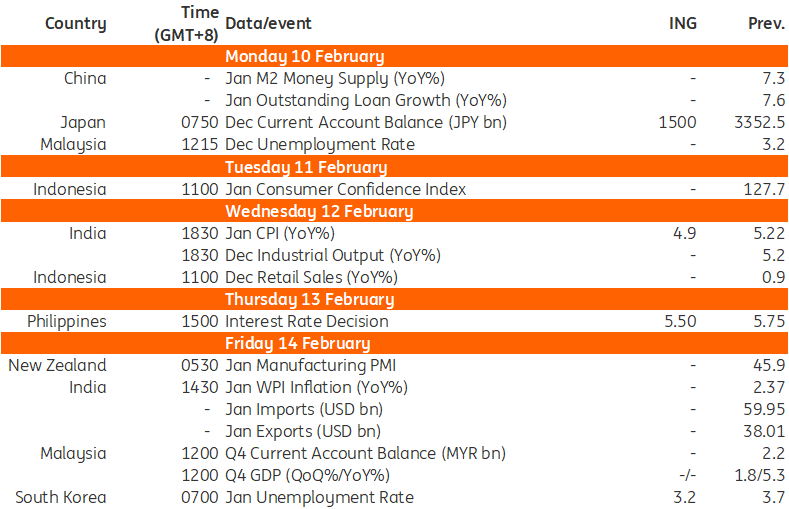

Key events in Asia next week

Source: Refinitiv, ING

More By This Author:

FX Daily: Payroll Revision RiskThe National Bank Of Poland Governor Sees No Scope For Interest Rate Cuts In 2025 But His Tone Was Softer

Rates Spark: Bessent And Payrolls Key As We End A Tumultuous Week

Comments

Log in or sign up to join the conversation.