Image Source: Unsplash

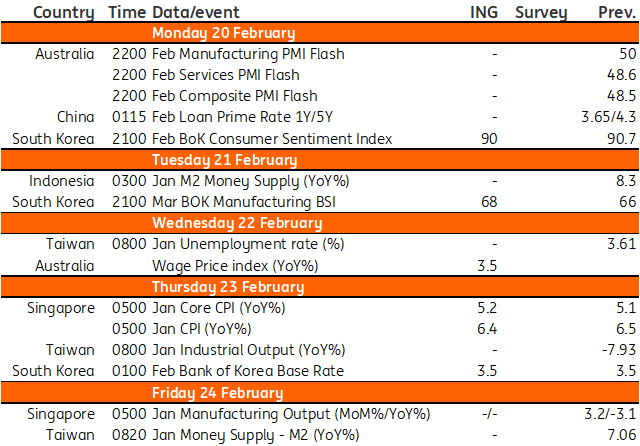

Some of the highlights in Asia next week include Australia’s wage data, the BoK meeting, Taiwan's export orders, and Singapore’s CPI.

Australia’s wage price index will provide direction for policymakers

Australia is set to release fourth-quarter wage price index data on 22 February. This was a keenly watched data point in 2021 when the Reserve Bank of Australia (RBA) tied its cash rate target to wage growth rising to a level consistent with target inflation of 3.5-4%. In the last quarter, the wage price index grew by 3.1%, which means that there is still room to inch higher, while inflation is currently running at 8.4% YoY.

If the wage price index grew by 1.0% in the fourth quarter from the third – as it did in the third quarter from the second, the index would finally reach 3.5%. Although this very lagging data point is mainly of academic interest, a rising number would still encourage hawkish rhetoric from the RBA.

BoK to pause on Thursday?

The Bank of Korea will meet on Thursday. We believe that the BoK’s rate hike cycle ended with the 25bp hike in January. But given that January's consumer price index picked up again, we are expecting the BoK to maintain its hawkish stance.

China's loan prime rates to remain unchanged

Chinese banks will announce possible changes to loan prime rates (LPR) next week. Given that the economy is recovering and that the People's Bank of China left the 1Y Medium Lending Facility rate (MLF) unchanged, we predict that the chance for a change in the LPR is small. Moreover, banks have been told by the government to offer lower interest rates on mortgages to provide support to the economy. This would result in banks not having enough room to squeeze net interest margins.

Weak semiconductor demand could hurt Taiwan’s economy

Export orders and industrial production will likely give clues about how bad semiconductor demand was in January. We expect declines of around 10-20% year-on-year for both. Final GDP data should show a slight yearly contraction; the advance estimate was -0.86% YoY. We expect Taiwan to enter a mild recession in the first half of this year given the weak demand for semiconductors, the main pillar of the economy.

Singapore CPI Inflation report

We could see headline inflation tick lower, but core inflation will likely remain elevated at 5.2% YoY as the latest increase in the goods and services tax kicks in. Finance Minister Lawrence Wong announced a fresh round of subsidies to help households deal with the rising cost of living. Wong believes inflation will remain elevated for at least the first half of the year.

Persistent price pressures should keep the Monetary Authority of Singapore (MAS) in hawkish mode although it needs to strike a delicate balance as slowing global trade threatens to negatively impact the export sector.

Key events in Asia next week

Image Source: Refinitiv, ING

More By This Author:

FX Daily: Hawks In The Ascendancy

RBNZ Preview: 50bp Hike, But The Peak Is Close

Rates Spark: Crucial Levels Ahead

Comments

Log in or sign up to join the conversation.