Image Source: Pexels

The Reserve Bank of Australia is likely to cut its cash rate by 25bps to 3.6%. Meanwhile, markets await data on Chinese inflation, industrial production, and retail sales, South Korean unemployment, and Japanese GDP.

Australia: Weaker data should alter RBA's cautious stance, giving way to a rate cut

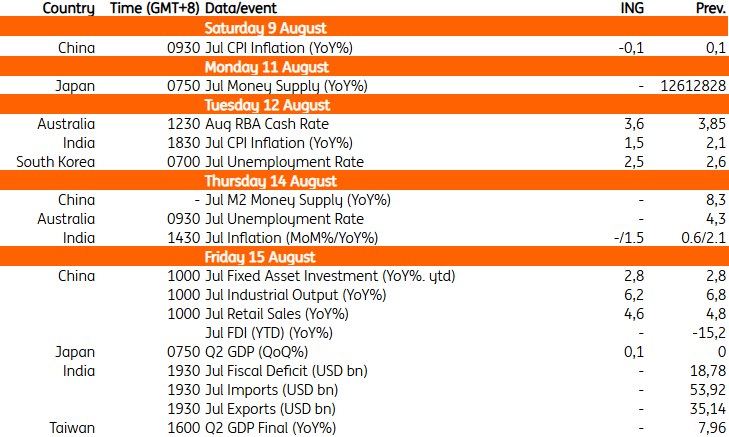

We expect the Reserve Bank of Australia (RBA) to cut the cash rate by 25 basis points to 3.6% at Tuesday’s policy meeting. Recent data on growth and inflation came in softer than expected, reinforcing the case for easing.

In a surprise move last month, the RBA held the cash rate steady at 3.85%, defying both market consensus and our own expectations. The decision reflected the central bank's desire for more evidence that inflation is tracking sustainably toward its 2.5% target. Since then, both the second-quarter inflation and June employment data undershot expectations. This suggests the RBA's cautious stance in July may give way to a rate cut.

China: Deflation returns as activity continues to moderate

China releases its July inflation data this Saturday. Consumer price index inflation is expected to teeter back into deflation at -0.1% year on year as downward pressures persist. Measures to tackle excessive price competition are unlikely to have an impact in the early going.

The July data dump is scheduled for Friday, showing that economic activity may have continued moderating. Housing prices saw an accelerated downturn in the last few months. With little fresh policy support, this weakness could continue into July. Industrial production comfortably beat forecasts in June, but it’s likely to have slowed to around 6.2% YoY. Retail sales have recovered year to date amid trade-in policies. But it’s possible we could be nearing the peak of policy impact. We expect retail sales to moderate to 4.6% YoY. Finally, fixed asset investment has been on the disappointing side, with private investment sidelined amid continued uncertainty. We expect growth could remain around 2.8% YoY ytd.

South Korea: Unemployment rate expected to decline

South Korea’s jobless rate is expected to decline to 2.5% in July from 2.6% in June. Despite weak hiring in the construction and manufacturing sectors, services related to leisure and eating out are expected to increase. Government cash handouts may have added some temporary jobs in services. Also, the government's job programme continues to support hiring in the social welfare and health sectors.

Japan: Modest GDP growth outlook

Japan’s second-quarter GDP release on Friday will be closely monitored. Following a slight contraction of 0.04% quarter-on-quarter, seasonally adjusted, in the first quarter, the economy is expected to recover modestly, producing an estimated 0.1% growth. Exports weakened considerably in the second quarter, and inventory changes are expected to have a negative impact on overall growth. Nevertheless, high-frequency data indicate a recovery in services and private consumption, supporting a moderate upturn in 2Q25. The odds of an October rate hike by the Bank of Japan are likely to be adjusted depending on the data.

Key events in Asia next week

More By This Author:

FX Daily: Diverging Central Bank Stories

The Commodities Feed: Potential Trump-Putin Meeting Weighs On Oil

Rates Spark: A Triple Tail In The U.S.

Comments

Log in or sign up to join the conversation.