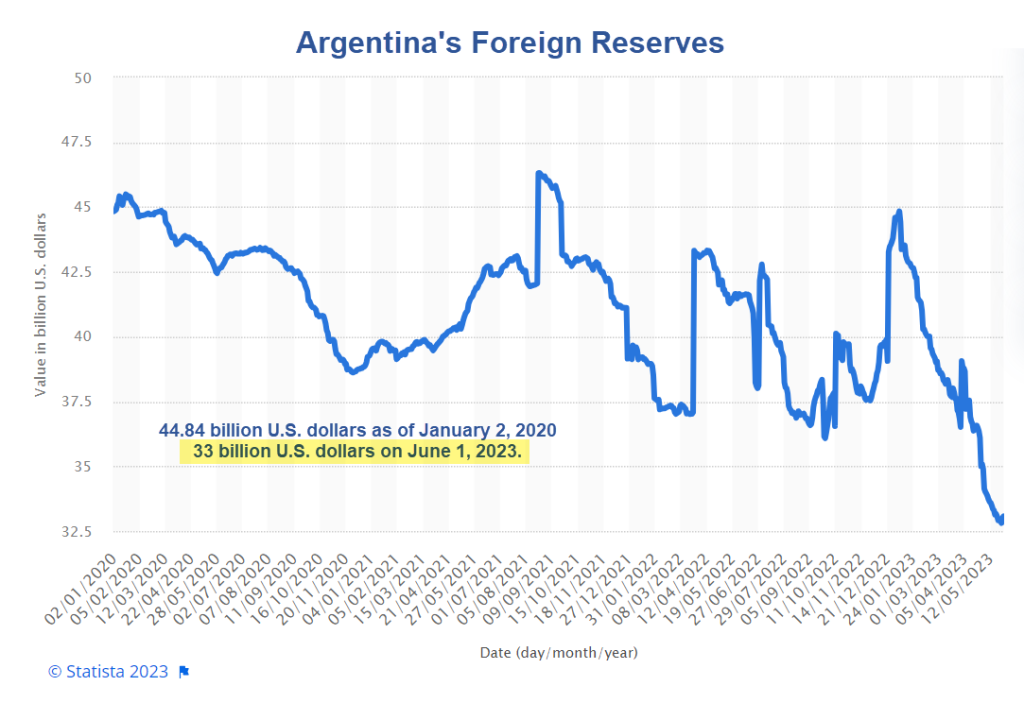

Image courtesy of Statista, annotations by Mish

Congratulations Argentina!

This morning I commented Congratulations Argentina for Electing the World’s First Libertarian President

Polls Wrong Again

It was supposed to be a very close election. But the polls got it wrong again.

Libertarian Javier Milei whomped Peronist Economy Minister Sergio Massa, by a margin of 56-44 percent.

Milei is pro-US dollar with plans to adopt the dollar and end Argentina’s central bank.

Thank you very much Steve for your support !! 💪

— El Derechista (@elderechistaok) November 20, 2023

I commented …

It was a promise capitalism and free market reforms, not the dollar, that decided the election.

Dollarization will be hard. And unless that’s doable by decree, he may not even be able to get the legislature to do that.

It’s moot if Steve Hanke is right or I am right because the key question is the same.

What is the Way Forward?

Milei cannot do this by decree. Argentina’s legislature would have to agree.

The Wall Street Journal discusses the setup in Argentina’s New President Wants to Adopt the U.S. Dollar as the National Currency

I strongly agree with some of the article and strongly disagree with other parts. And I have my own ideas about what Argentina should do and whether the IMF can help.

Let’s start with comments by President-elect Javier Milei. “Closing the central bank is a moral obligation,” Milei said late Sunday. “Never in pesos,” he said during the campaign. “That garbage isn’t even useful as fertilizer.”

The Hurdles Via WSJ

A major hurdle for Milei’s plans to swap out the peso is a divided congress in which no political faction holds a majority. The left-leaning Peronism movement that will rule Argentina until Milei’s Dec. 10 inauguration, as well as the center-right Together for Change coalition founded by former President Mauricio Macri, each hold less than half of the seats in the senate and lower house.

In his victory speech, Milei thanked the center-right coalition for helping secure his win, but he didn’t mention dollarization. It remains unclear how independents and moderates, who make up the remaining seats of the legislature, will respond to Milei’s agenda.

The courts are another challenge. In September, Supreme Court magistrate Horacio Rosatti told Spanish newspaper El País that replacing the peso with a foreign currency would be unconstitutional and violate national sovereignty.

Won’t Be Easy

I am in total agreement with all of the above.

In a report Sunday, Goldman Sachs economists said, “As with everything in economics, there is no free lunch, and adopting, preserving and benefiting from dollarization could be challenging.”

Assuming the legislature goes along, there is a Constitutional question.

But let’s assume for the moment Milei clears those hurdles.

Disagreement Over Flexibility

Without its own currency, Argentina would lack monetary tools to cushion external shocks, economists say.

“Argentina has no flexibility to absorb shocks like a sharp decline in export prices, agricultural price volatility, oil price increases, the impact of war on demand for your exports, political instability leading to withdrawal of deposits,” said Martin Castellano, head of Latin America research at the Washington-based Institute for International Finance.

Q: How does dollarization change that?

A: It doesn’t, other than improve things.

Argentina now has no flexibility to deal with export prices, oil prices, or anything else. It’s only method of trying was the printing press that led to hyperinflation.

In this regard, lack of currency printing press flexibility is a great thing.

And preventing runs on banks is easy, don’t lend out more dollars than people have on deposit and don’t leverage into borrow-short, lend-long duration schemes.

The US ought to try that. It would have prevented the collapse of Silicon Valley Bank.

The IMF Chimes In

Economists say the country doesn’t have the funds to carry out as ambitious a proposal as dollarization. In recent years, the country has lost access to global debt markets.

“To begin with, you need access to capital markets to convert the entire monetary base into dollars, and you don’t have them,” said Alejandro Werner,an economist who served as head of the Western Hemisphere department of the International Monetary Fund.

In general, the IMF is the problem, not the solution. It demands of bankrupt countries that they pay back everything the country owes in dollars.

Argentina’s External Debt June 2023

(Click on image to enlarge)

Debt vs Reserves

- Argentina has $262.2 billion in external debt.

- Argentina has $33.0 billion in foreign reserves.

The peso is worth about 10 cents on the dollar on the black market and the debt to reserves ratio shows why.

CATO Explains Dollarization

Please consider The Economist Gets It Wrong on Dollarization in Argentina

In a recent article, The Economist assures that inflation‐ridden Argentina should not and cannot dollarize. The publication’s anti‐dollarization stance is part of a broader warning against free market economist Javier Milei, who gained a surprise victory in last month’s primary elections and vows to dollarize the Argentine economy if he wins the presidency later this year.

The Economist misunderstands the most fundamental aspects of Milei’s plan to dollarize Argentina and shut down its central bank. This is, in fact, the best thought‐out and most urgent part of his political platform. It affirms, for instance, that “Argentine banks and households would need a float of dollars to get up and running, which Mr. Milei has no way of providing.”

As we explain in our recent policy brief, Argentina’s central bank might lack dollars, but Argentine citizens and companies do not. Private sector actors do try to shield themselves from the country’s frequent bank runs by holding dollars in other jurisdictions or under their mattresses. At the end of 2022, Argentines held over $246 billion in foreign bank accounts, safe deposit boxes, and mostly undeclared cash, according to Argentina’s National Institute of Statistics and Census. This amounts to over 50 percent of Argentina’s GDP in current dollars for 2021 ($487 billion). Hence, the dollar scarcity pertains only to the Argentine state.

To dollarize, Argentina needs to replace the peso‐denominated monetary base with the equivalent in U.S. dollars at — or slightly above — the free market rate of exchange. Dollarizing at a rate far above that of the free market would be counterproductive because it would produce even higher inflation levels for a prolonged period. On the other hand, dollarizing at a rate below the free‐market exchange rate would lead to a bank run because depositors would act to protect their savings from a forced devaluation.

In Argentina’s particular case, there is an official exchange rate—currently ARS $365—which most people cannot access. Hence, the black market exchange rate, known locally as the “blue dollar,” is the closest approximation to what a free‐floating peso would be worth in dollar terms. At the moment, ARS $740 will buy you one blue dollar.

The Mechanics of Dollarization

In both Ecuador and El Salvador, which dollarized in 2000 and 2001 respectively, dollarization involved parallel processes. In both countries, the most straightforward process was the dollarization of all existing deposits, which can be converted into dollars at the determined exchange rate instantly.

As Argentine economist Nicolás Cachanosky explains, when you dollarize deposits, the danger of a bank run is minimized insofar as dollarization takes place at the market rate and monetary transactions continue to take place within the banking system.

Crucially, in both Ecuador and El Salvador, dollarization not only did not lead to bank runs; it led to a rapid and sharp increase in deposits, even amid economic and political turmoil in Ecuador’s case. With the mere announcement of dollarization in January 2000, Ecuadorians began to deposit their dollars in banks even though the latter were so beleaguered they were paying negative interest rates.

What Argentina Shouldn’t Do

It is impossible for Argentina to pay back what it owes and should not even try.

Nor should Argentina accept any onerous strings from an IMF bailout.

The IMF accurately states Argentina does not have access to capital markets. But getting access via the enormous strings the IMF imposes is a mistake.

Anyone dumb enough to loan Argentina money despite repetitive bouts of hyperinflation deserves to lose that money.

What Argentina Should Do

- Argentina should declare all its foreign debts null and void.

- Adopt procedures along the lines of what CATO suggests above.

Stopping Bank Runs

The US does not have a gold-backed dollar. That went away long ago. President Nixon put the final end to it in 1971.

Unfortunately, we do not even have a 100 percent dollar backed dollar. This led to numerous borrow-short, lend-long schemes including the the recent run on Silicon Valley Bank.

Making a Truly Safe Bank

I have a number of suggestions on how to make a safe bank starting with a 100 percent dollar backed dollar.

For discussion, please see The Perfect Solution to the Banking Crisis Is to Make a Truly Safe Bank

One simple regulatory rule would have saved SVB, that being a 100% reserve requirement on deposits instead of a 0% reserve requirement on deposits.

Fed Policy, Zero-Reserve Banking

My follow-up article was Fed Policy: It’s Not Fractional Reserve Banking, It’s ZERO Reserve Banking

Money that is supposedly 100% payable on demand was in fact NOT payable on demand. It’s like leasing your car to two people simultaneously, banking on the notion one will not show up.

I recommend Argentina avoid this mistake.

More By This Author:

Question Of The Day: Why Does The Fed Value Its Gold At $35 Per Ounce?Falling Rent Is Extremely Rare, Yet Economists Keep Expecting That

NAHB Housing Sentiment And Traffic Head Toward the Post-Pandemic Low

Comments

Log in or sign up to join the conversation.