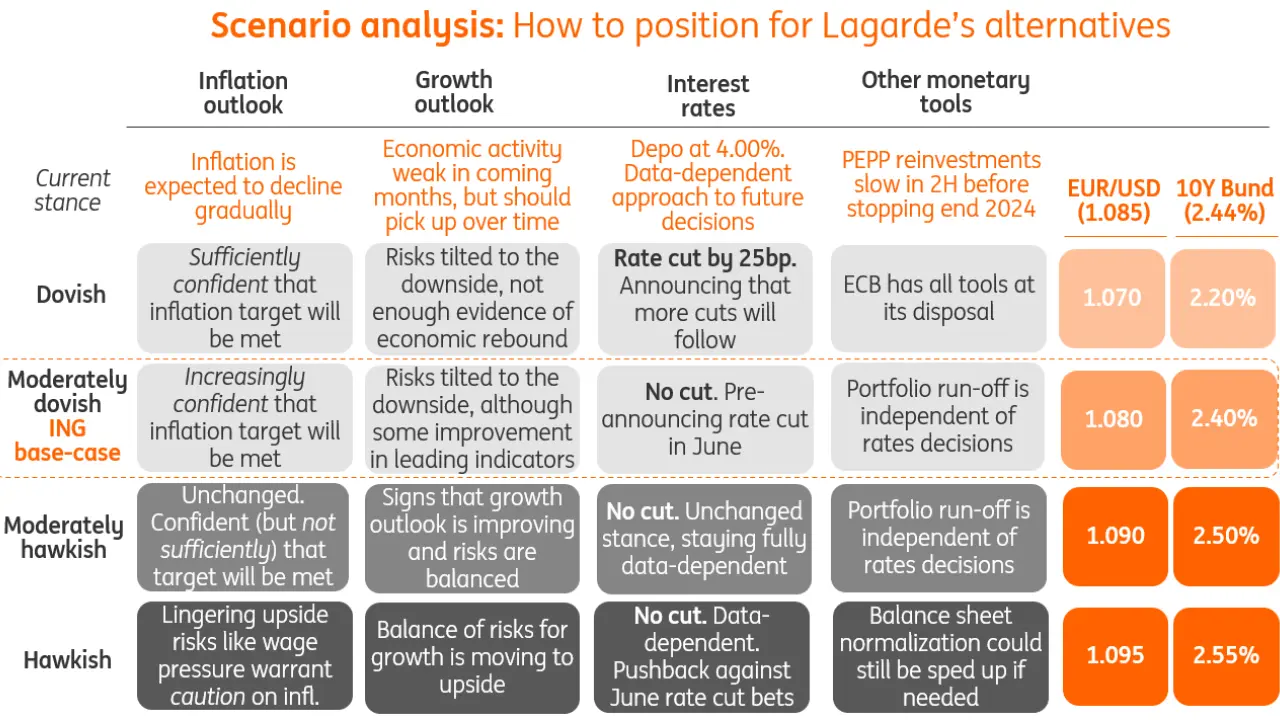

April’s ECB Cheat Sheet: Eyes On The Target

We look at four scenarios and implications for FX and rates ahead of this week’s ECB policy announcement. Our base case is that the ECB will signal it is ready to lower rates in June, reinforcing market expectations on monetary easing this year. For markets, it may be more relevant how the ECB communicates about its plans beyond June though.

(Click on image to enlarge)

Rates: Looking beyond June

Markets are discounting only a minuscule chance that the ECB will cut rates this week, but they seem convinced that June will see the first rate cut – more than 24bp out of a 25bp cut are already discounted. Markets will therefore be more interested in how the ECB communicates about its plans beyond June. Here the market has been looking for around 90bp of overall easing over the course of 2024 for the past couple of weeks. This is slightly more than the 75bp of easing we foresee for the ECB in our base line scenario.

More recently expectations for overall ECB easing were pared back somewhat, though, on the back of markets also reassessing their Fed cut expectations. The impact is still limited at the EUR front end, not least because the market is also still seeing the Fed cutting rates in July, if not in June – Fed easing may be delayed, but not cancelled. However, the Fed’s ability to cut rates anytime soon could be further questioned in the near term if official data remains robust – and more importantly – if US inflation figures continue to come in too hot. Important for EUR rates will be how the ECB is perceived as distancing itself from these dynamics.

Yield levels further out the curve have seen more spill over from US dynamics already. 10Y Bund yields at currently 2.44% are close to the upper end of their recent range. But at the same time 10Y UST-Bund spreads have also widened noticeably, briefly rising above 200bp last week. It is a level that has been topped more lastingly and structurally only when Fed and ECB policy paths diverged. Near term, we think market expectations have room to head into this direction, if only temporarily.

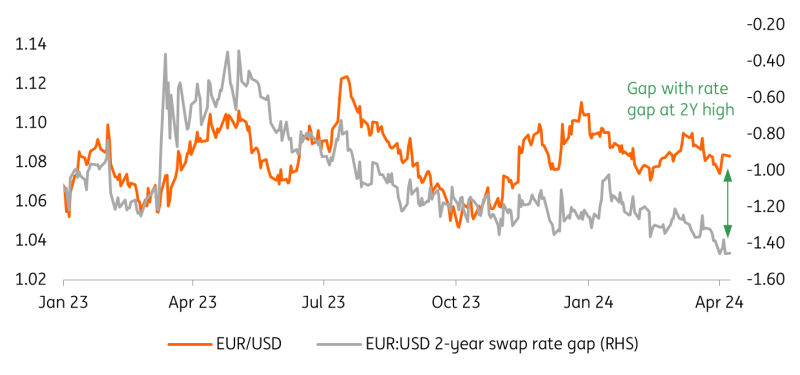

FX: EUR/USD is expensive, even without a dovish ECB

The strong US jobs market figures last Friday have not hit EUR/USD as many would have expected. That is not entirely surprising when looking at EUR/USD performance in the past few months, where we have observed a decoupling between rates and FX dynamics. As shown in the chart below, if we take January 2023 as a basis, we are now observing the highest gap between EUR/USD and its depressed short-term swap rate differential in around two years. The good performance of equities is largely to be blamed for this decoupling, and especially given how global risk sentiment (to which EUR/USD has a positive beta) has been lightly affected by the repricing higher in Fed rate expectations.

EUR/USD and swap rate differential

Source: ING, Refinitiv

At these levels, EUR/USD looks expensive, but what would really be needed to realign it with its lower rate differential? An equity sell-off would be the first intuition, but we also think that the start of the rate-cutting cycle in the US or the eurozone can have a similar effect. The dependence of developed central bank expectations to Fed pricing has contributed to dampening FX volatility and we suspect that tangible signs of policy divergence will be needed to drive larger moves in G10 FX.

A cut by the ECB already this week can send EUR/USD sharply lower. That is the dovish case in our scenario analysis, but not our baseline expectation. It is more likely that the ECB will keep inching closer to signalling a cut in June, which should not change the picture dramatically for EUR/USD, but also continue to reduce the upside potential for the pair in an environment where the Fed is looking less likely to cut in June too. A stabilisation around 1.0800 in the near term remains likely in EUR/USD, although drops to 1.07 or lower look more likely than a break higher to 1.09/1.10.

More By This Author:

Industrial Metals Monthly: Why Copper And Iron Ore Prices Are Diverging

Asia Morning Bites - Monday, April 8

National Bank Of Poland Governor Sticks To Hawkish Bias; Cuts Not Debated

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more