Aluminum Sees A Perfect Storm In The Energy Crisis

The aluminum (JJU) industry’s ability to swiftly respond to strong demand and higher prices is being hampered by the ongoing energy crisis and the move to decarbonization. The risk to prices is more skewed to the upside, particularly in any further supply squeeze.

Concurrent forces squeezing aluminum supply

The current supply squeeze in aluminum reflects both the power crunch and the Chinese government's ‘dual-control' policy, but is ultimately tied to decarbonization goals. China has emphazised its ‘dual carbon’ goals (for carbon emissions peaking by 2030 and achieving carbon neutrality by 2060). We need to view these factors separately.

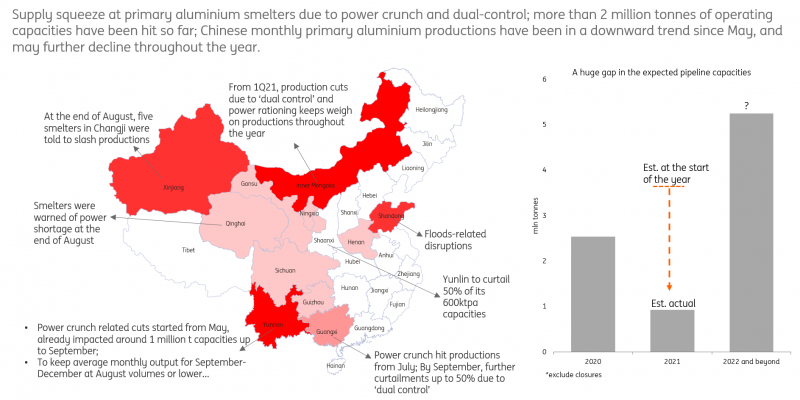

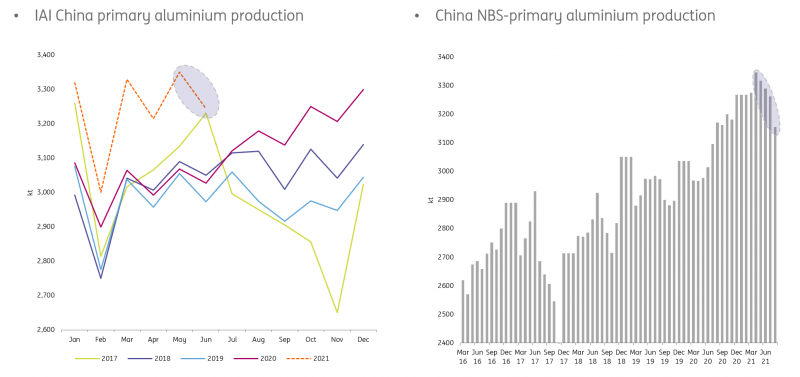

In September, the power crunch escalated further - 20 Chinese provinces were hit, and cities in Northeast China even saw households facing blackouts . There are mandates by local authorities asking smelters to curtail productions throughout the remainder of the year, including in Yunnan, Guangxi and Xinjiang. As of September, more than two million tons of operating capacity have been hit, and pipeline capacities have been further pushed back (see Fig 1). Meanwhile, the latest data suggests that production has been declining every month since May (Fig 2).

Fig 1. Power shortage escalates and affects wider regions

Source: ING

Fig 2. Increasing disruptions hit China primary aluminum productions

Source: IAI, NBS

However, the situation is dynamic not static

In China, the authorities vowed last week to tackle the power shortage issue ‘at all costs’. Today there's a document circulating that the local government from Inner Mongolia, a key coal production region, has ordered more than 70 miners from the region to dig more coal. Yet it remains to be seen how this would help to alleviate the crunch. A key uncertainty is that the winter heating season is only starting next month. Demand for coal and electricity is set to rise further in the coming months. Going forward, supply constraints include: (1) as we highlighted in our last update, the coming dry season in Yunnan is likely to see hydropower generation fall from this month, and (2) there are likely to be the usual winter cuts in northern China over the winter. Last December, the market saw disruptions on the alumina side which gave aluminum prices a nudge higher.

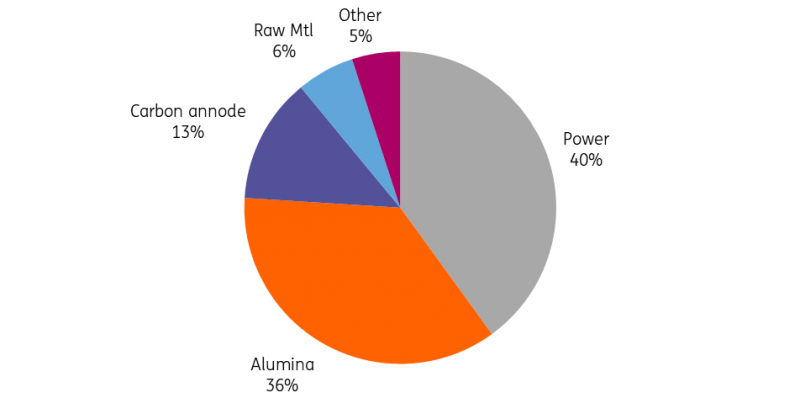

Elsewhere, surging energy prices from Europe, especially for natural gas and power, add to risks of margin squeezes at smelters. In the aluminum smelting cost breakdown, electricity accounts for around 40% (Fig 3). So far, the announced cutbacks due to energy prices are relatively small. The situation in Europe is worth monitoring - if energy prices stay higher for longer then the risk of further cutbacks adds to more aluminum supply losses, on top of those from China.

Fig 3. aluminum Smelting Cost Components

Source: IAI, CINA

Producer margins may have peaked

The energy crisis - with surging energy prices and the dual control measures in China - has seen the turmoil spread to other markets. The prices of many raw materials have risen, so quickly eroding producers’ margins.

Alumina costs, representing almost 35% of the total in aluminum smelting, had remained muted before August. Then supply began to tighten in China, hit by the same factors as those afflicting primary aluminum. The Guinea coup in early September further fanned alumina prices, gaining more than 38% over the last month.

Prices of other inputs such as carbon anode have risen to the highest on record for the China market. Meanwhile, for suppliers of aluminum value added products (VAP) that need other metals as ingredients for making the products and selling to the downstream, magnesium and silicon prices have risen sharply recently. This has also curtailed production.

Demand destruction is a short term concern

As the above supply-side dynamics continue to unfold, there are growing concerns that energy prices and metal product prices might derail any economic recovery post-pandemic.

We had noted in our daily update that the power crunch has evolved into a double-edged sword that hits both supply and demand. The situation is worse than what we saw in March - when dual-control started to impact supply in Inner Mongolia - and in June when power shortages forced smelters to curtail operations from Yunnan. Downstream and hence demand are now being affected, although we still need to wait for more evidence to corroborate the level of demand destruction. While there is a risk to short-term demand, we remain constructive on aluminum demand over the medium to longer term. We see increasing demand from packaging and energy transition-related sectors, including vehicle lightening and renewable energy.

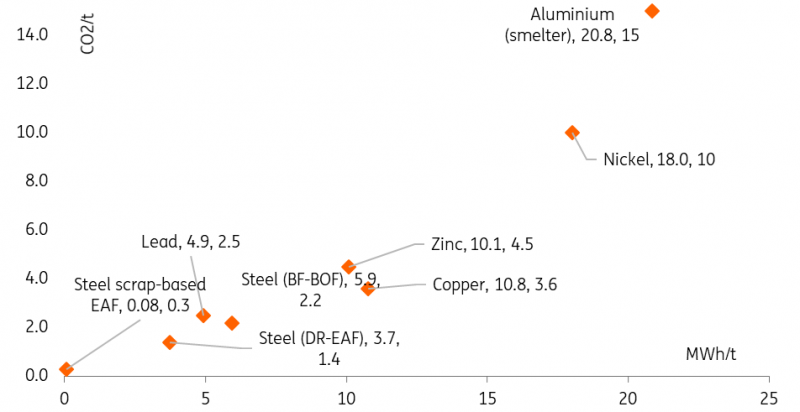

Fig 4. Carbon and energy intensity per ton of metal produced

Source: TPI, BloombergNEF, ING

Investing commodities, cyclical play to structural play

The market is now faced with rising concerns over stagflation pressure within economies, and rising macro headwinds could take some wind out of commodities’ sails. What we have seen in the market since Q2 is a rising tide lifting all boats. However, now it’s probably better to analyze each metal individually, as we have probably shifted away from a cyclical change towards a structural one, where we might see sticky divergence among metals. For high energy intensity and high emissions metals (in terms of their production process; Fig 4), their industry’s ability to flexibly respond to demand surges and high prices has diminished. (We discussed in May in our note aluminum is entering a new era).

Given the nature of primary aluminum production, we remained structurally bullish on aluminum. However, due to the recent escalating power issues, we have lifted our aluminum forecast to $2,950/t for 4Q21 (based on LME 3M quarterly average). Still, we expect prices to return above $3,000/t over the next six months. Key downside risks include any major reversal in the current decarbonization push and policies in the traditional fossil fuel mining sector - such as a big boost in coal supply that could alleviate the power issue and demand destruction.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does ...

more