The current economic scenario carries lots of uncertainties for investors, but a few select businesses are benefiting from increasing demand in these unprecedented times. Fastly (FSLY) is delivering accelerating growth during the pandemic, and the company offers abundant potential in the years ahead.

Accelerating Revenue Growth

Fastly provides a Content Delivery Network (CDN) on an edge cloud platform. In essence, the company is in the business of making the internet faster and more secure. In times of global pandemic and shelter-at-home policies all over the planet, it is more important than ever to keep the internet running smoothly and safely.

The technology can be complex, but the company's mission is quite straightforward:

"Our mission is to fuel the next modern digital experience by providing developers with a programmable and reliable edge cloud platform that they adopt as their own."

Fastly counts among its customers many of the most successful and renowned internet players in the world, including names such as Shopify (SHOP), Yelp (YELP), Twitter (TWTR), Spotify (SPOT), New York Times (NYT), Airbnb, and Vimeo, among many others.

Source: Fastly

Management considers that its market opportunity is large and growing. The company estimates that the total addressable market opportunity could be worth around $18 billion in 2019, and grow to $35.8 billion by 2022.

These kinds of estimates from management necessarily carry a large degree of error and should always be taken with a grain of salt, especially in an uncertain economic environment. However, the financial reports for the first quarter of 2020 confirm that Fastly is benefiting from accelerating growth, and the business looks stronger than ever during challenging times for the global economy.

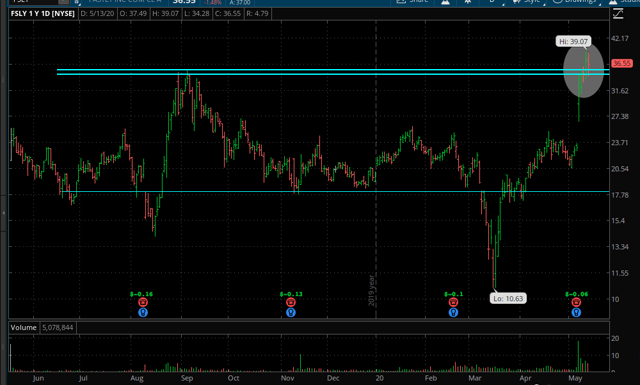

Total revenue during the first quarter of 2020 reached $63 million, an increase of 38% year-over-year. Dollar-based net retention rate was 133% during the quarter; the net retention rate - which includes the impact of churn rate - was 130%. This is indicating that customers continue to spend more with Fastly, which is a positive reflection on the company's ability to deliver value to those customers.

In a sign of confidence, management also raised guidance for the full year of 2020. Fastly increased revenue guidance to the range of $280 million to $290 million, from $255 million to $265 million.

Management highlighted, during the conference call, how the social distancing measures have produced an acceleration in demand over the short term, yet the company's growth engines are ultimately supported on long-term drivers.

In the words of CEO Joshua Bixby:

"As social distancing measures increased over the March period, we continue to see increased traffic across the internet and our platform, which certainly provides an additional boost to our results, but more than anything our first quarter results were driven by Fastly’s strong business fundamentals and the quality of our offerings, which we believe will continue to attract the best of the web.

Fastly is a platform of choice for innovators. We are partnering with the most technologically advanced and creative companies who we believe will not only weather this storm, but will continue to thrive in this environment. Companies are increasingly recognizing the importance of digital transformation, not only to survive during these uncertain times, but also for long term success. As we're seeing this trend accelerate and evolve, we believe we are best positioned to partner and grow with these companies as they look for a trustworthy and modern platform."

The company is making a big bet on serverless computing with its Compute@Edge offering, which is still in beta and moving to limited availability. This new business could be a powerful growth engine and a major source of competitive strength for Fastly, and it will probably have a positive impact on the company's profit margins over the medium term.

Risk, Timing And Valuation

Fastly's most attractive growth opportunities come from edge computing solutions. The company has outstanding technologies in this area, but it also faces competition from companies such as Cloudflare (NET), Akamai (AKAM), Microsoft (MSFT), and Amazon (AMZN).

Wall Street analysts generally have a simplistic view of competitive dynamics. Just because a company has competition from large rivals does not mean that it will be crushed by such competition. On the contrary, a smaller and deeply focused player can many times deliver more innovative solutions with superior speed and flexibility than larger rivals. Besides, when the market opportunity is large and growing, it can provide enough room for multiple successful players to do well in the long term.

But, it will be very important to watch the competitive dynamics in the industry over the medium term, because this is arguably the biggest risk being faced by investors in Fastly's stock. If the company fails to keep its technological edge over the competition with permanent innovation, then the whole bullish thesis for Fastly falls apart.

Fastly is also losing money at this stage. The company is clearly making progress in this area, and management is confident about the prospects for reaching profitability in the medium term, but this still remains to be seen.

The timing can seem tricky at first glance. The stock has been moving sideways over the past several months, and then it made an explosive move to new highs after reporting much better than expected earnings and increased guidance last week.

However, make no mistake, it is not too late to buy Fastly. If the company continues to grow well and gain market share versus the competition, the stock has plenty of room for upside potential from current levels.

The table shows some key statistics for Fastly versus Akamai and Cloudflare. To begin with, Fastly is materially smaller in terms of both revenue and market capitalization, so it has a lot of room to gain size if the company continues delivering solid performance over time.

Besides, the price to sales growth - which is calculated by dividing the price to sales ratio by the revenue growth rate - is lower in the case of Fastly than in Akamai or Cloudflare.

| FSLY | AKAM | NET | |

| Market Capitalization | 3,465.60 | 15,466.82 | 8,454.56 |

| Revenue Trailing 12 Mo | 217.83 | 2,951.41 | 316.55 |

| Sales Growth TTM | 38.20% | 7.24% | 48.91% |

| Sales Growth | 38.20% | 7.24% | 48.91% |

| Price to Sales | 16.01 | 5.29 | 26.07 |

| PSG | 42 | 73 | 53 |

Data from S&P Global via Portfolio123

There are many things that could go wrong with Fastly, but valuation should be no impediment for the stock to deliver solid returns if the company's fundamentals remain strong.

The Bottom Line

When you find a company with high growth prospects and still at a relatively young age, the risks are always substantial, especially in a business operating in a highly dynamic landscape and facing intense competition. In this particular case, competitive pressure first, and lack of profitability a distant second, are the main risk factors to watch.

Even if the stock is trading at new highs, valuation should not be a problem as long as the business keeps growing well. Fastly is still relatively small, and the stock price is not excessive at all in comparison to the company's growth opportunities.

Besides, the company is run by a leadership team with plenty of skin in the game and a solid track record of delivering consistent growth and innovation over the years. This reinforces the idea that Fastly will be able to stay nimble and continue delivering the right solutions to its customers over time.

Fastly has a lot of room for sustained revenue growth and expanding profitability over time. In such a scenario, increasing sales and a larger share of revenue being retained as profits could provide a double boost to earnings growth over time.

In a nutshell, Fastly is a high-risk investment, no doubt about that. But, upside potential could more than compensate for the risk, if things work out well for investors over the years ahead.

Comments

Log in or sign up to join the conversation.