Rotating Between SPY And IEF Based On Valuation And Fundamentals

Picking the right individual names in an asset class is important, but selecting the right asset class at the right time can be even more crucial. When the stock market is booming, most individual stocks will tend to do well. Conversely, when the stock market is crashing, even the best stocks in the market will tend to move in the wrong direction.

This article will be analyzing a quantitative strategy that rotates between stocks and bonds using the SPDR S&P 500 Trust ETF (SPY) and the iShares 7-10 Year Treasury Bond ETF (IEF). The strategy is based on earnings numbers as a key valuation metric and as a measure of overall fundamental trends.

The main idea is not that investors should replicate this overly simplistic quantitative strategy in real life, but rather showing how valuation and earnings expectations can be remarkably effective tools to make better decisions in the market.

The Concept Behind The Strategy

The main idea behind the strategy is quite simple. When stocks are attractively valued in comparison to bonds and earnings estimates are moving in the right direction, we want to own stocks via SPDR S&P 500. On the other hand, when stocks are relatively expensive or earnings are declining, we want to own bonds via the iShares 7-10 Year Treasury Bond ETF.

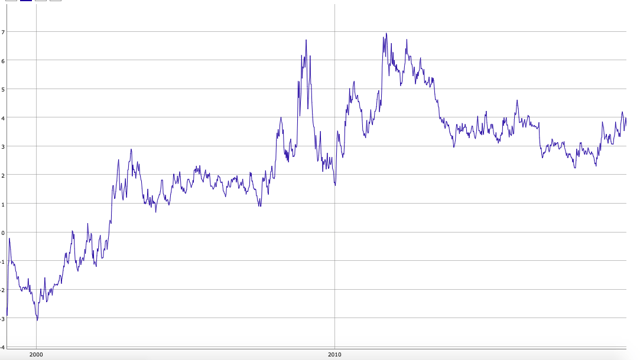

As a valuation metric, the strategy uses the equity risk premium, which in this case is defined as the difference between the earnings yield for companies in the S&P 500 versus the 10-year Treasury bond yield. The larger the earnings yield of the stock market in comparison to bond yields, the more attractively valued stocks are.

In order for the quantitative system to be invested in SPY, the equity risk premium needs to be above 1%, meaning that stocks are relatively well-priced in comparison to bonds.

In addition to analyzing if stocks are cheap or expensive, we also need to consider that the main trends in earnings expectations can have a big impact on subsequent returns. If earnings are declining due to a recession or some kind of economic problem on the horizon, this generally pushes stock prices lower, regardless of the initial valuation levels.

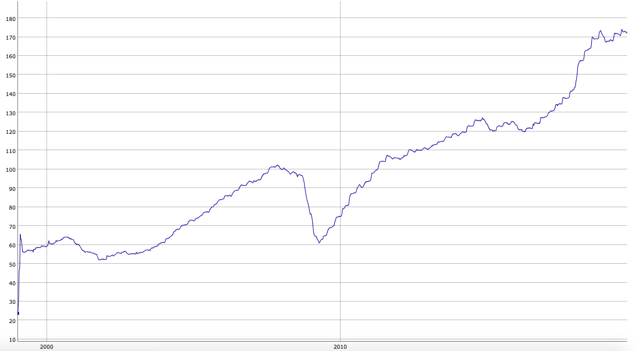

To measure fundamental trends, the strategy requires the 5-day moving average in earnings estimates for companies in the S&P 500 to be above the 21-day moving average in order to buy the SPDR S&P 500 Trust ETF. Since earnings for a particular year can be too volatile, the strategy uses a blended metric that considers both earnings estimates for the current year and the next fiscal year.

Wrapping up, when the equity risk premium is above 1% and earnings estimates are increasing, the quantitative strategy is invested in the SPDR S&P 500 Trust ETF. Conversely, when the equity risk premium is below 1% or earnings expectations are declining, the strategy moves to bonds by investing in the iShares 7-10 Year Treasury Bond ETF.

Analyzing Performance

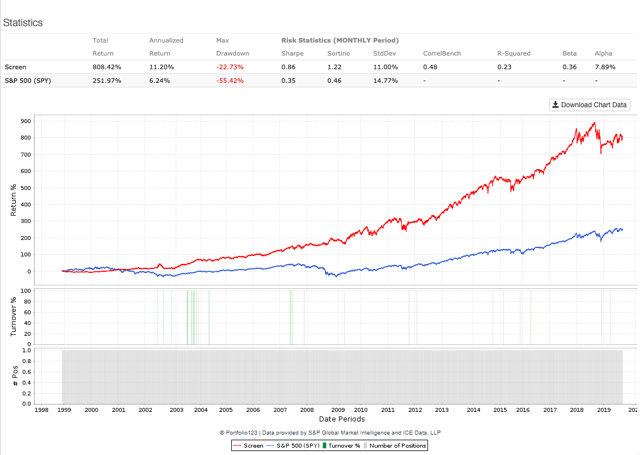

The backtest begins in January 1999, and the strategy is rebalanced every week. The quantitative strategy produced a total return of 808.42% versus 251.97% for the SPDR S&P 500 Trust ETF in the same period. The strategy alpha amounts to 7.89% annually.

In simple terms, a $100,000 investment in the quantitative strategy in January 1999 would currently be worth $908.400 million, while the same amount of capital allocated to the SPDR S&P 500 Trust ETF would be a much lower value of $352,000.

Data from S&P Global via Portfolio123

Even more important, the maximum drawdown - meaning the maximum decline in portfolio value from the peak - is 22.73% for the quantitative strategy versus a much larger drawdown of 55.42% for buy-and-hold investors in stocks. The strategy's ability to protect the portfolio during bear markets for stocks is arguably its main strength.

Looking at returns over different periods, we can see that the strategy has underperformed versus a buy-and-hold position in SPY over the past five years. This is because stocks have substantially outperformed bonds in this period, and pullbacks in stocks have been relatively shallow.

In a bull market for stocks, rotating between stocks and bonds tends to produce subpar returns. However, it is important to keep in mind that the strategy is focused on optimizing risk-adjusted returns as opposed to maximizing returns alone.

| Strategy | SPY | |

| Annualized | 11.20% | 6.24% |

| Five Year | 60.39% | 75.28% |

| Total | 808.42% | 251.97% |

| Sharpe Ratio | 0.86 | 0.35 |

| Sortino Ratio | 1.22 | 0.46 |

| Max Drawdown | -22.73% | -55.42% |

| Standard Deviation | 11.00% | 14.77% |

| Correlation | 0.48 | - |

| R-Squared | 0.23 | - |

| Beta | 0.36 | - |

| Alpha (annualized) | 7.89% | - |

You have to expect false signals from time to time, meaning periods in which the strategy goes for safety, but the pullback in stocks is ultimately shallow and short-lived. No strategy can provide the right signals on every occasion, and these kinds of strategies are ultimately about reducing portfolio risk, not so much about increasing returns.

Some observations regarding the historical allocations for the strategy:

- From January 1999 until January 2003, the strategy was allocated to bonds. First because stocks were overvalued in 1999, and then because earnings expectations were declining during the recession in 2001 and 2002.

- Due to declining earnings during the great recession in 2008 and 2009, the strategy was also allocated to bonds from June 2018 until July 2009.

- These two protective moves during big markets produced massive benefits in terms of historical performance for the quantitative strategy.

- The strategy also produced several false signals, especially since the financial crisis in 2009. But most of those false signals were short-lived; none of them lasted for more than two months.

- IEF has delivered mostly solid returns in the past two decades because interest rates have remained low. On the other hand, we need to consider that a false signal being allocated to IEF could be much more damaging if interest rates start rising in the future.

In simple terms, most of the outperformance produced by the quantitative strategy was due to avoiding deep bear markets during the tech bubble and in the financial crisis. In times of smoother returns for stocks, a strategy such as this one will most probably underperform versus buy-and-hold. We also need to consider that performance could suffer if we enter a period of rising interest rates in the future.

Reading The Data

The quantitative strategy is based on remarkably simplistic assumptions, being either 100% in stocks or 100% in bonds depending on absolute values for the equity risk premium and earnings trends. This is only to illustrate how these concepts work and what kind of performance they tend to produce in the long term.

A more reasonable approach for investors to implement in real life would be keeping a well-diversified allocation and reducing exposure to stocks when the equity risk premium is low, meaning that stocks are relatively overvalued or when earnings expectations are declining.

The chart below shows how the equity risk premium is currently above 3.7%, substantially above the 1% threshold employed by the quantitative strategy. By historical standards, stocks look attractively valued in comparison to bonds.

Data from S&P Global via Portfolio123

Earnings expectations tell a more complicated story. Analysts are currently expecting a decline in earnings for 2019, and this is due to the global economic slowdown and the trade war uncertainty to a good degree. But earnings for 2020 are still expected to increase, so the blended metric is still in an uptrend.

Data from S&P Global via Portfolio123

The equity risk premium is very supportive of stocks, while the main trend in earnings expectations is softening but still rising when considering 2019 and 2020 together. Because of these factors, the strategy has been long in SPY since May of this year.

Nobody can know for certain what the future will bring for SPY and IEF, and all kinds of strategies have weaknesses as well as strengths. However, hard data is indicating that stocks are more attractive than bonds when considering both valuation and fundamental trends.

Disclaimer: I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in ...

more