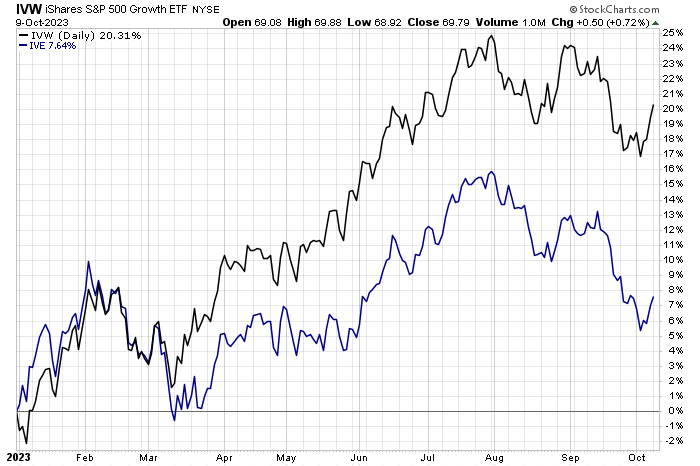

It wasn’t that long ago that several brave forecasters were advising that 2023 would be the year that value stocks regained their leadership credentials that the historical record suggests is the prevailing trend. Measured in relative terms for 2023, however, growth shares continue to dominate the performance race, based on a set of factor ETFs through Oct. 9.

This year’s leader is iShares S&P 500 Growth ETF (IVW), a large-cap fund that’s up more than 20% year to date. Its value counterpart (IVE) is far behind with a relatively modest 7.6% gain so far in 2023.

Despite the weak run for value, some analysts keep hope alive that this risk factor will one day reclaim its performance glory.

“While there are no crystal balls, there doesn’t seem to be any strong evidence that the value premium is dead,” wrote Larry Swedroe at Buckingham Strategic Wealth, in late September. “The poor recent performance has been due to changes in what John Bogle called the ‘speculative return’ (the change in relative valuations).”

Meanwhile, the small-cap factor is suffering even more this year. Even worse for fans of value: small-cap value is posting the deepest shade of red year to date with a 3.3% decline for our set of factor funds.

Claro Advisors senior vice president Jeff Corey says the negative results for small caps this year should come as no surprise. “Investors tend to look for quality during times of market volatility, and that consists of stocks with strong balance sheets, significant profit margins, stable business models, and growing dividends, and those are characteristics that are not typically found in the small caps space,” he advised last week.

If the renewed conflict between Israel and Gaza is an indication, market conditions that will favor small caps don’t look set to emerge in the near-term horizon.

Higher interest rates are helping either. Although large companies face stronger headwinds when borrowing costs rise, the pain is greater for smaller companies, according to recent research from Ned Davis Research, which advises that these firms are paying a record level of interest expense.

“This is new, uncharted territory for small caps,” says Ed Clissold, Ned Davis’s US strategist.

Consider too, per Financial Times, that “small caps have broadly weaker balance sheets than their large-cap counterparts. Debt as a multiple of profits is higher and interest payments take up a larger share of earnings.”

But perhaps the level of pain will at least stop going up, or so a Federal Reserve official suggests.

“If long-term interest rates remain elevated… there may be less need to raise the fed funds rate,” says Lorie Logan, president of the Federal Reserve Bank of Dallas and a current voting member of the central bank’s rate-setting committee.

More By This Author:

Will US Stock Market’s Outsized Leadership Persist In Q4?Several Corners Of Bond Market Manage To Shine This Year

Is Hard-Landing Risk Rising (Again) For The US Economy?

Comments

Log in or sign up to join the conversation.