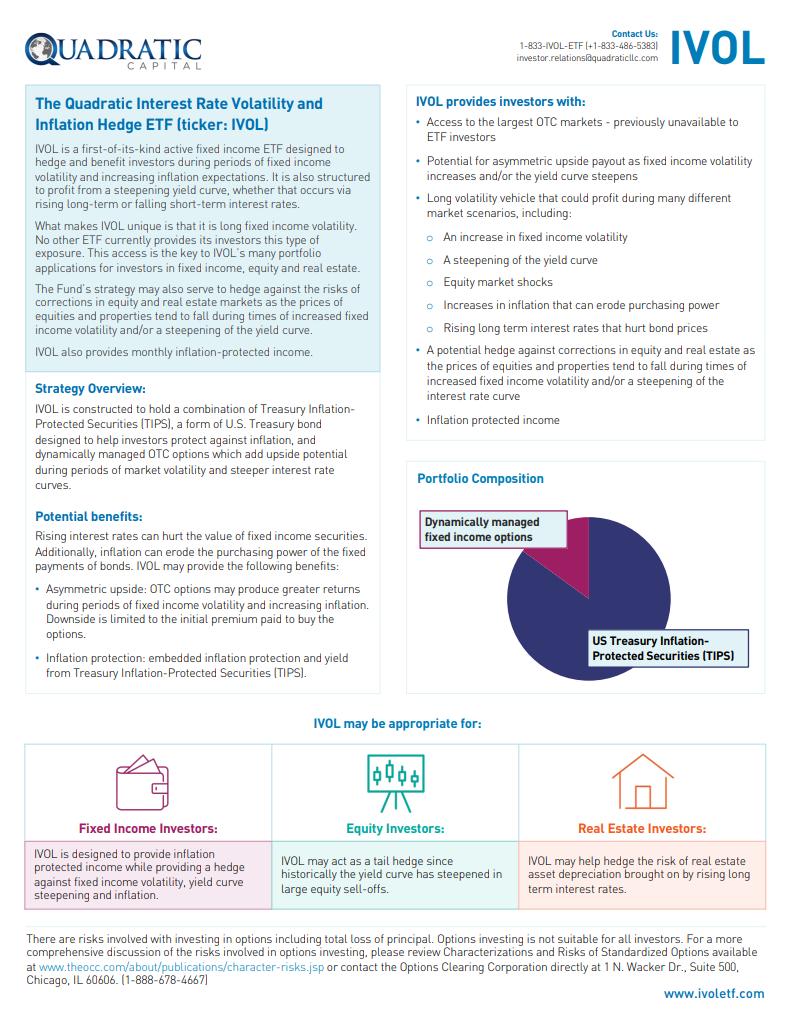

IVOL: My Dream ETF

Is it finally here? Has the latest round of poor ISM economic releases unleashed the long-awaited it’s-too-obvious-to-ignore slowdown the bond bulls were pining for?

The market certainly thinks so. Have a look at the US 2-10 yield curve spread:

(Click on image to enlarge)

In late September we were threatening inversion, but the last couple of poor ISM economic releases has steepened the yield curve by almost 15 basis points. That’s not crazy by any means, but it signals the market expects the Fed to chase the front end down.

I have long believed that curve steepeners were one of the best trades out there so it feels good to have the market agree with me a little.

Many ask, how do you play the steeper yield curve without trading futures? Well, you could calculate the durations of various fixed income ETFs (SHY, IEF, TLT) and properly ratio hedge them. However, that’s a capital eater. And it’s not elegant. Kind of like showing up at a classy affair in a Canadian tuxedo.

And no, putting a tie on that outfit only makes it acceptable if you are a 14-year-old Ryan Gosling who will grow into a man so good looking that he turns down the “Sexiest Man Alive” title numerous times.

So, what’s an investor to do?

Lucky for us, Nancy Davis’ Quadratic Capital has the answer. The Quadratic Interest Rate Volatility and Inflation Hedge ETF (ticker IVOL) is just the ticket. It’s kind of my dream ETF. Like the feeling of watching a young Noah Calhoun come back to Charleston or a dapper Sebastian Wilder wooing Mia Dolan, I am more smitten than my teenage daughters.

(Click on image to enlarge)

This product is designed for inflation hawks who forecast increased fixed-income volatility and a much steeper curve.

Although just as Ryan Gosling was a disaster on defense in ‘Remember the Titans’, for true bond bears, IVOL is not quite perfect. Let’s go through how it works and discuss some of the ways you can pair it with other instruments to achieve a payoff profile unique in the listed ETF world.

IVOL Makeup

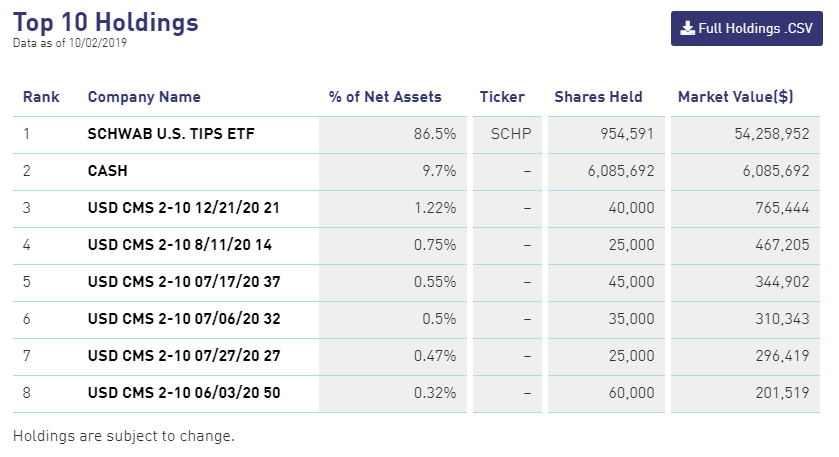

Let’s dig into the composition of the IVOL ETF to understand better how it will behave under various scenarios. On the IVOL website, the holdings are listed on a daily basis. Here are yesterday’s positions:

(Click on image to enlarge)

The vast majority of the fund is made up of Schwab U.S. TIPS ETF. This is a listed ETF that trades under the symbol SCHP.

But then we scroll down a couple of rows and we are confronted with a whole slew of funky looking tickers.

USD CMS 2-10 12/21/20 21?

You stick that symbol into your Think-or-Swim quote system and nothing is found. What is this dark magic? What kind of voodoo are they dabbling in?

And herein lies IVOL’s compelling story. These are over the counter options unavailable to retail investors.

They are options on the 2-10 yield curve. The date represents the option’s expiry and the final number is the strike in basis points.

It’s not an easy trade to understand by any means. Options on the curve steepening? Surely those must be expensive. It sounds so exotic.

However, they aren’t expensive. Far from it. They are actually quite cheap. Which is why shrewd macro funds like Brevan Howard have set up single-purpose entity funds to gain exposure to this trade. I have long wanted to participate in this market (Can Someone Please Help Me with the Timing?), but alas, the ‘tourist has no ISDA. Relegated to licking the glass as the cool kids dine at the yield-curve-option buffet, I have made do by trading futures. Sure it gets me my exposure, but I don’t get to take advantage of the cheap vol in the yield curve space to get that truly asymmetric payoff. Until now. And the best part? I don’t even have to trade the options. Nancy and her crew will do it for me (which is even better as I would probably just mess it up with a view).

The team at Quadratic are continually monitoring and trading the yield curve options so that there is always a desired amount of gamma. This is not a case of buying the options and letting them decay downward with the trade either working or not. The IVOL ETF is designed to have continual gamma at all points of time and price. This involves active portfolio management.

If I had my way, the ETF would be 100% curve steepener options. That’s how much I love that trade. The problem with that solution is the volatility would be enormous.

To tamper down the swings, the vast majority of the portfolio is invested in TIPS. I understand the logic. US treasury protected securities offer some of the highest real yields in the world. If you believe the Federal Reserve will lower rates and create an economic rebound that both steepens the yield curve and also creates inflation, then the IVOL portfolio is ideal. Buy IVOL and forget about it.

However, if you are of the opinion that the next big crisis will emanate out of the bond market, then the TIPS portion of the portfolio is worrisome. I explain my reservations about owning TIPS outright in the article Inflation Breakevens: A Core Holding.

But I love, love, love the option portion of the IVOL portfolio. It offers an exposure unique in the listed world.

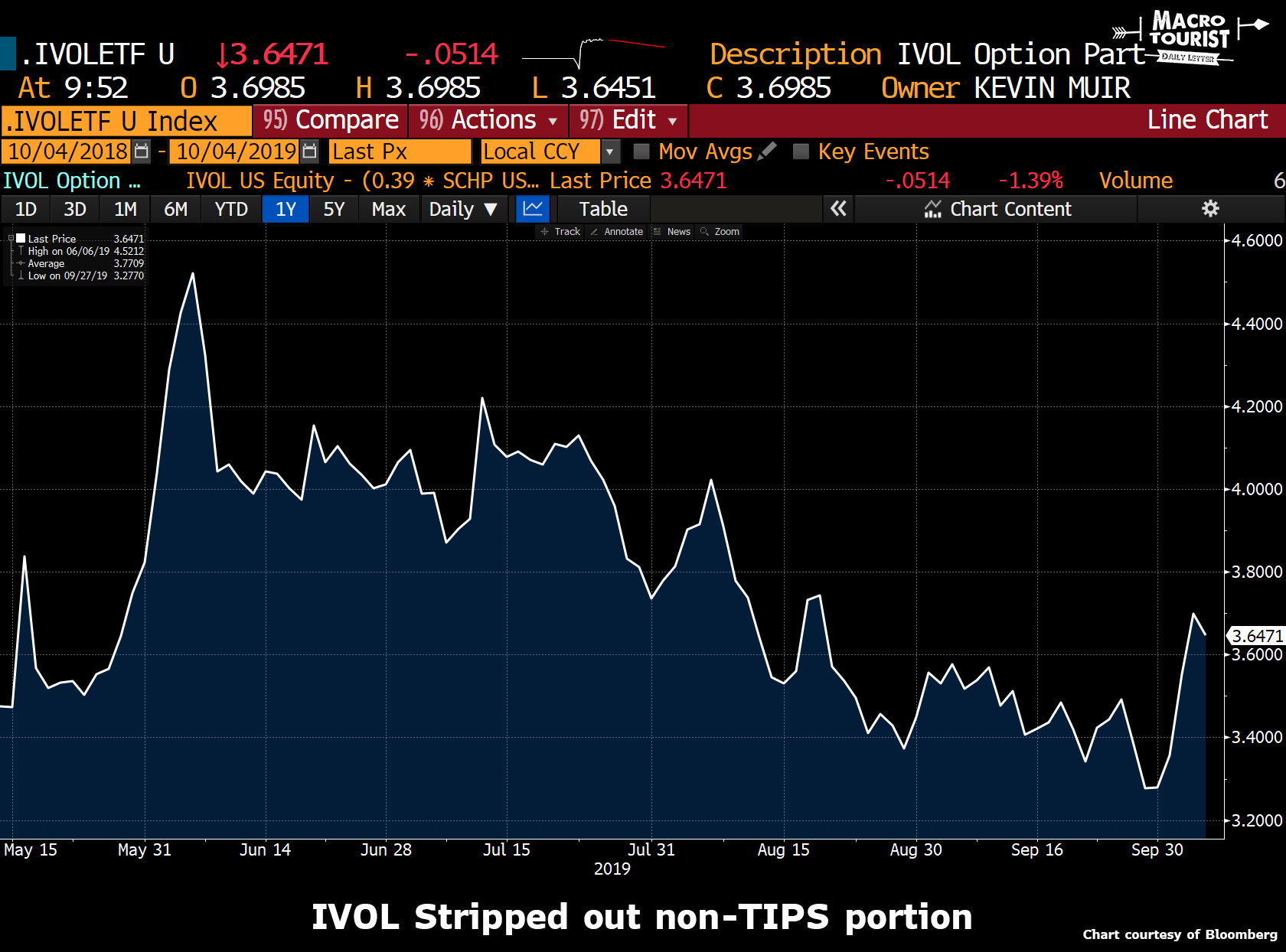

The different ways to hedge IVOL

So what’s the solution? Just because I have my hangups being long bonds doesn’t mean I need to give up on IVOL.

One way to deal with my bond aversion is to hedge out the SCHP. That’s easy and clean. We know approximately the number of SCHP per share of IVOL. Hedge the proper amount and you are left with exposure to the option portion of the IVOL book.

Here is a chart of this stub piece:

(Click on image to enlarge)

A week ago this part was trading for a song. With the recent move steeper in the yield curve there was a surge in the non-TIPS stub portion.

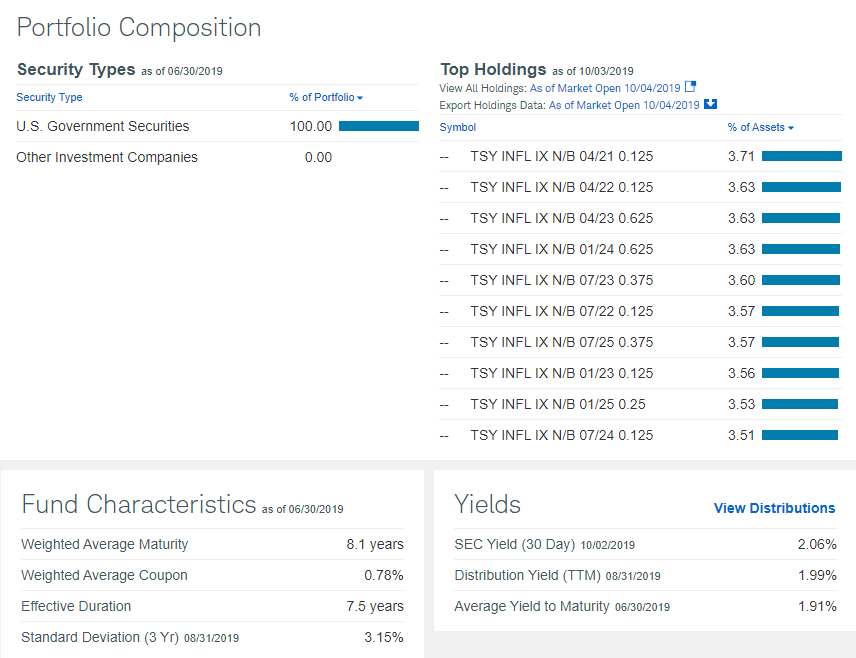

Another option is to combine my belief that inflation breakevens will rise with my affection for IVOL’s option portion. Approximately 86% of the IVOL portfolio is the Schwab TIPS ETF. A long position in inflation breakevens consists of long TIPS and short the proper amount of government treasury bonds.

To help us with the calculations, here is the composition of the SCHP ETF from the Scwab website:

I can combine my two favorite trades - long steepeners with long inflation breakevens by shorting 86 cents of 7.5-year duration t-note futures. Now that’s truly my dream ETF position.

Now I understand everyone likes their burger dressed a little different. What’s delicious to some is gag-worthy for others. That’s what makes a market. So I am not expecting everyone to want to hedge out the long TIPS portion of the IVOL. In fact, those interested in IVOL probably shouldn’t bother and instead, consider using it as a fixed-income complement (replacement) in a well-balanced portfolio.

But no matter your preference, IVOL deserves a good look as that yield curve option exposure is one of the most unique trades available to retail investors.

Disclosure: None.