It’s Been A Rough Ride!

When I was young my family in the summer used to attend the local speedway. Amateur and Pro car drivers would run around the track at fast speeds. We would also be treated to the occasional demolition derby. Beat up cars would try and destroy the other cars until they were all inoperable but one, and that was the winner! Great fun.

Last week we said that there were signs that we would see a corrective rally given Friday’s action in the markets. We thought there might be some follow-through. There was one Monday and Tuesday, but then several retail company’s earnings reports shed light on fears of a slowing economy resulting in a brutal sell-off on Wednesday.

The market’s demolition derby continued on Friday when all US equity markets were down more than 2% intraday. Then in the last hour of trading, we witnessed a sharp recovery as the shorts closed out positions before the weekend. By the closing bell, the Dow and S&P 500 had closed up on the day, and the Nasdaq recovered most of its almost 3% loss. Fast and furious.

This week was all about concerns of an oncoming recession. Other countries, including China, are reporting similar economic conditions. This has caused many investors to liquidate their holdings in the market and seek cash to preserve capital.

Bull or Bear Market?

As we pointed out last week, the economic conditions are all negative, for the most part.

Inflation is high and trending higher. Ongoing relentless price hikes (gasoline, food, staples, etc.) are causing demand destruction. This means consumers are starting to watch spending for luxury goods and services. Retailers and consumer staples companies had a very rough week (see Big View notes below)

On Friday, the S&P 500 closed down 17.8% on the year.

This close came within a whisker of signaling a bear market (down 20%) intraday on Friday. This was the 8th straight negative week for the S&P 500, as well as the Nasdaq and the 9th for the Dow. The Nasdaq is down 29% year-to-date, and small-cap stocks are down 27%. While the largest S&P companies are down on average 20% year-to-date, the Nasdaq and tech stocks are a different story. Many great technology and Nasdaq traded companies are down as much as 80%.

This is a brutal market.

Since early in the year, we have been warning of this possibility based on our Big View and various technical signals. Our Market Outlook posts this year have been advising readers to either subscribe to our investment models, Mish’s discretionary service, or consider cash as a position to preserve capital.

If you are a subscriber, then luckily you have benefited from our strategies rotating into commodity, energy, and market inverse instruments. This is how most of these strategies have delivered positive returns on the year.

The problem with labeling the current correction as an outright bear market is that overall earnings this quarter have been quite good. According to FactSet, 95% of companies have reported earnings, 77% have beaten expectations, and 73% have beaten revenue estimates. Until companies across the board report significant misses of their estimates (and a contraction of earnings), this may still be a bull market experiencing a stagflation mode with little upside. Defense is still warranted.

It is hard to label markets. Bear markets can be deceptive in many ways. A good example is looking back to March 2008 when the S&P was down approximately 20% and experienced a couple of sudden and dramatic up days. Typical of a true bear market, investors were quick to rush into the market thinking that we were at the bottom. It took another 12 months and the S&P moving down 47% before we actually hit bottom in March of 2009. We have been in a bull market ever since.

Last week we said that we thought you would see a corrective wave up. We still believe that we will see, sometime soon, a powerful and sudden rally to the upside. It is inevitable and necessary to work off what has become oversold conditions. Many investors may think it is the beginning of a new bull phase. Do not count on it. Please be careful. (See our suggested course of action below)

The Long View

It is important for investors to recognize that several things occurred in 2021. Investors poured more money into the market than in the previous 19 years combined. And with our indicators showing market deterioration during the last half of 2021, we were putting out consistent warnings that “something did not look quite right.”

The second thing is companies were buying back stock in record amounts. The estimates were that $900 billion of company capital was committed to purchasing back their own stock.

Last, the Federal Reserve was also propping up the markets coming out of the Pandemic. They too had committed billions (if not trillions) to the stock and bond markets to create easy money accommodation.

In every economic cycle, investors always get giddy and feel that making money in the markets is easy and that they can do no wrong. 2020 and 2021 may be two such years this occurred. So much so that people were leaving their jobs so they could stay home and trade for a living. These are pivotal moments. Mr. Market likes to get everyone involved before it decides to begin the destruction mode. So far, in 2022, we have wiped out trillions of dollars in capital in a short 5 months.

The problem is that many investors get heavily invested near the top. With a brutal market decline, like we are witnessing now, it can take a lengthy period of time for those investors to get back to even. Right now, mass liquidations and outflows are huge and growing. We suspect it is because the average retail investor does not want to get burned again.

It is also showing up with money managers and professionals steering large pools of assets. According to the Bank of America Merrill Lynch Global Fund Manager Survey, hundreds of professional money managers are nearing record bearishness. These folks are now holding more cash than they did during COVID-19 bottom, December 2008 bottom, and the market bottom in 2003. This extreme fear may coincide with either a new leg up or a bear market rally.

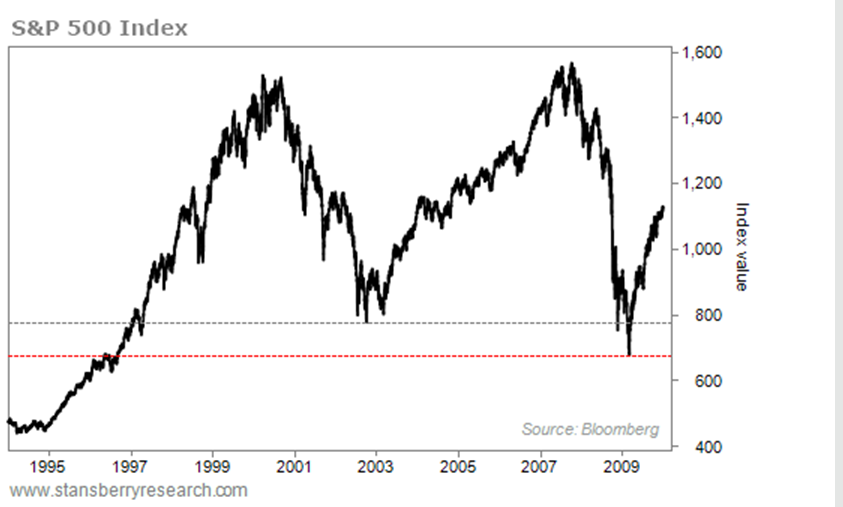

For investors who put money in the market in 1999-2000, it took until 2006 just to get back to even on their investments. Then investors who put money in stock indexes in 2006-2007 had to wait another decade to get back to even. You will see above that both market declines (2001-2002) and 2007-2008 took the markets back to 1996 levels and wiped out more than 10 years of wealth creation. As we have said repeatedly, the markets can be brutal. That is why we continue to make suggestions about how you can put yourself in a position of capital preservation with the potential to reap the benefits of the next good markets.

Remember, if we are in a Bear Market, your #1 goal should be preserving capital and not profiting from it.

Disclaimer: Like to learn more about relative strength methodology? Our most recent free training material can be found more