How Did We Know The S&P 500 Was Going To Give Up Its Gains? What's Next?

Although equity futures rose sharply on Wednesday morning and CPI data proved innocuous, those gains were quickly erased once Wall Street opened to greater volumes. We’ll get to the CPI data in a moment, but knowing those gains were quickly going to be erased didn’t demand a crystal ball, and I’ll show you why!

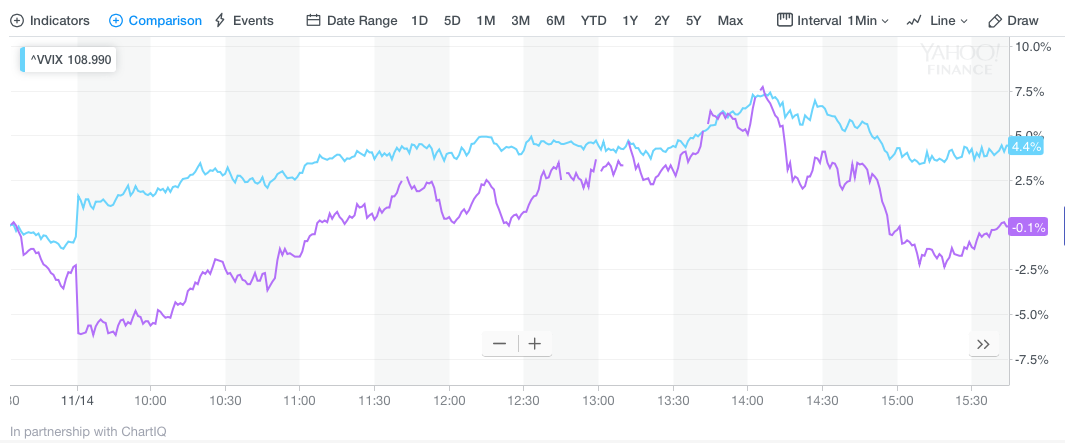

The chart positioned above is of the Volatility of Volatility index or VVIX (blue line) with a VIX chart laid over it (purple line). As you can see, toward the left hand of the chart, VIX fell 2.5% at the market open, but VVIX was up 2.5% at the market open. VVIX rising is an indication that hedge funds are doing just that, hedging with VIX options, which pushes the index higher. VVIX tends to lead a volatility spike and assumes its end before the VIX actually plunges. Given the divergence at the market open on Wednesday between VVIX and VIX, it was unlikely the S&P 500 was going to maintain its gains without VVIX falling in line with the VIX. It's also why Finom Group had a much higher short order on VXX shares than that from the opening hours of trade. (See bottom of article for the trade)

When it was all said and done, Wall Street had another rough trading session with the Dow Jones Industrial Average (DJIA) falling as much as 300+ points before ending the day down 200 points. The tech-heavy Nasdaq (NDX) was down 64 points or .9% with the S&P 500 (SPX ) off 20 points or .76 percent. In a week where the S&P 500 weekly expected move was $50, the index has already completed a nearly $80 move.

While investors ponder the divergence between the stock market and the economy, yields have fallen during the current market pullback. Criticisms and concerns have been squarely place on the Fed, as the central bank seems hell-bent on lifting rates. Late Wednesday evening, Fed chairman Jerome Powell spoke with the Dallas Fed President Rob Kaplan and participating audience members. What investors desire to hear most, given the market’s declines of late, is some potential for the Fed to pause rate hikes after December’s .25 bps hike. Unfortunately, Powell’s statements didn’t lend clarity, regarding a pause, during the Q&A session with Kaplan.

“I’m very happy about the state of the economy right now. We’re in a good place, and I believe our economy can grow and grow faster.

He said, however, that the Fed is at a point where it has to take risks from moving either too quickly or too slowly “seriously,” and he did identify risks to the economic outlook. Twice he noted that the global economy was slowing, which Powell called “concerning.”

Moreover, the slowing housing industry, which Powell pointed out is not simply about rates but also a scarcity of lots and labor was also mentioned. Powell noted that many Americans have never lived in an environment of high mortgage rates.

CNBC’s Jim Cramer pounced on the comments from Fed chairman Powell. Since October, Cramer has insisted that the Fed show some reasonable language that suggests the Fed isn’t on autopilot and won't’ hike through global economic slowdowns.

"It's the first time that I've actually heard Jay Powell say, 'You know what? We've got to be careful, because there are signs of the economy slowing,' whether it be because of tariffs, whether it be just because genuine economic activity seems to be cooling off.

He gets that the tightenings have had an impact and that maybe he shouldn't keep tightening, because the impact is going to get worse and worse and worse for the economy," the "Mad Money" host continued. "And he said he did not want to be responsible for setting us back.

I need everybody to think that things are going to be awful," he said. "The bear market that everyone is talking about? Well, it's got to be universally accepted and people have to keep leaving. And if they don't, then what's going to happen is someone's going to say, 'You know what? I heard Powell. I'm going to stay in.' Every weak hand has to go."

Interest rates have been on the rise, as the Fed has committed to its path of rate hikes that will end 2018 with a total of 4 rate hikes. Mortgage rates have climbed during this period, which has resulted in a sharp drop off in demand for new mortgages and new home sales since the beginning of 2018. I have also suggested that if the stock market underperforms going into the December rate hike, the Fed’s language will indicate a pause in rate hikes come 2019. I discussed this potential for a Fed pause in a recent interview with Dale Pinkert of Forex Analytix.

“We all like to pronounce that the Fed doesn’t bow to the equity market sentiment and direction, but it does. It always has. The market tends to fall with economic conditions and rise accordingly. Right now the market is clearly telling the Fed to pause, rate hikes are curbing the demand for housing and mortgages, this affects the banks and we can see that in the financial sector performance. While most economic indicators have remained quite strong, not to mention earnings growth, the Fed has to consider the potential for economic activity to slow as it tightens and into 2019. Therefore, I’m of the opinion the investors will see some divergence in the Fed’s language on the subject of future rate hikes in 2019. Any, even slight, indication along this line will provide a serious move higher for equities. Until then, it’s gonna be choppy.”

So how about that CPI data released on Wednesday? The headline was much more sensational than the reality of the data, which came with provisions for future reads on inflation. The consumer price index climbed 0.3% in October to mark the biggest advance since January, the government said Wednesday. It also matched the forecast of economists polled by MarketWatch.

The increase in the cost of living over the past 12 months rose as well, to 2.5% from 2.3%. The rate of inflation is still below a six-year high of 2.9% set three months ago. What matters most is the core CPI and that actually fell in October. The yearly increase in the so-called core rate, a figure closely watched by economists, dipped to 2.1% from 2.2 percent. That’s the smallest increase since April.

“The rebound in CPI inflation to 2.5% in October, from 2.3%, was mostly driven by a rise in gasoline prices which will be more than reversed over the next couple of months,” said Andrew Hunter of Capital Economics. “The rest of the report supports our view that underlying inflation is unlikely to rise much further from here.”

One of the major factors that caused the increase in CPI during the month of October was gasoline. The good news is, the falling price of oil is likely to result in lower prices and less pressure on inflation in the next few months. Gasoline prices at the pump are down, on average, $.17 over the last 3 weeks and since October’s. Still, the cost of rent, used cars and trucks, medical care, home furnishings and car insurance also increased. These are major household expenses.

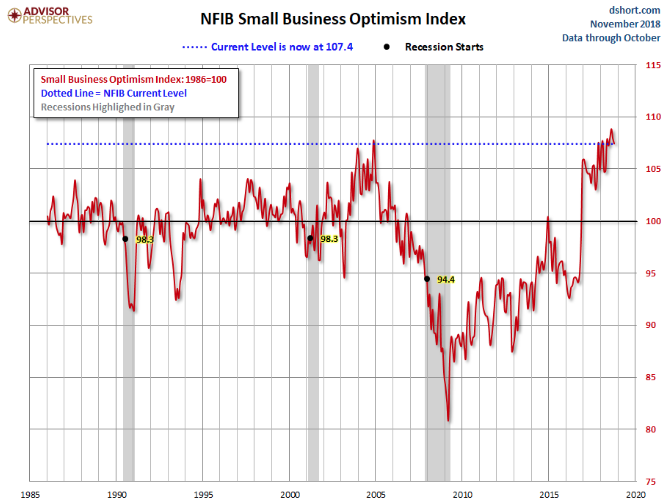

Other economic data proving more beneficial to investors came from The National Federation of Independent Business small-business optimism index. The NFIB declined 0.5 point to a seasonally adjusted 107.4 in October. While down MoM, it remains near all-time highs.

“Small business optimism continued its two-year streak of record highs, according to the NFIB Small Business Optimism Index October reading of 107.4. Overall, small businesses continue to support the three percent-plus growth of the economy and add significant numbers of new workers to the employment pool. Owners believe the current period is a good time to expand substantially, are planning to invest in more inventory, and are reporting high sales figures.

For two years, small business owners have expressed record levels of optimism and are proving to be a driving force in this rapidly growing economy,” said NFIB President and CEO Juanita D. Duggan. “The October optimism index further validates that when small businesses get tax relief and are freed from regulatory shackles, they thrive and the whole economy prospers”.

At present, there remains no clear and present danger to the economy despite how the market performance has proliferated since October. Thursday marks the last day of hedge fund redemptions for the fiscal year and may provide the market with one less risk-off issue to contend with. Coming up before the opening bell on Wall Street is the latest reading on the consumer through monthly retail sales. Economists polled by MarketWatch expect retail sales to have grown .5% ex-autos in October. Also prior to the opening bell will be the Q3 2018 results from Wal-Mart (WMT ). Wal-Mart’s results come after a rather strong Macy’s (M) Q3 report found its stock falling sharply on Wednesday.

Macy’s reported third-quarter adjusted earnings of 27 cents per share, ahead of the 15-cents FactSet consensus. And revenue was $5.40 billion, meeting the FactSet guidance. Same-store sales on an owned-plus-licensed basis grew 3.3%, also ahead of the FactSet consensus for 2.6% growth. Macy's now expects fiscal 2018 same-store sales on an owned-plus-licensed basis to rise 2.3% to 2.5%, versus previous guidance for an increase of 2.1% to 2.5%. Sales are now expected to be up 0.3% to 0.7% versus previous sales guidance for flat to 0.7% growth. And adjusted EPS is expected to be $4.10 to $4.30, up from $3.95 to $4.15 previously.

So why did Macy’s find its share price grossly depreciated after smashing bottom-line estimates and boosting its guidance, margins. Its gross margin rate of 40.3% of net sales was flat to last year. Macy’s has greatly reduced its store count over the last couple of years and also greatly reduced its inventories, selling more direct to consumer during these reductions in both operations and retail sq. footage. The retailer stated it will continue on this path of reducing physical selling space. Usually, when a business trims the fat, gross margins improve, not stay flat and not fall. That may be the issue investors are concerned with for the long haul. Macy’s is essentially attempting a “shrink to grow” strategy… a strategy that has not ever worked in the big-box department store history of retail sales. The retail landscape is littered with bankrupt retailers that have attempted this strategy over the past decades.

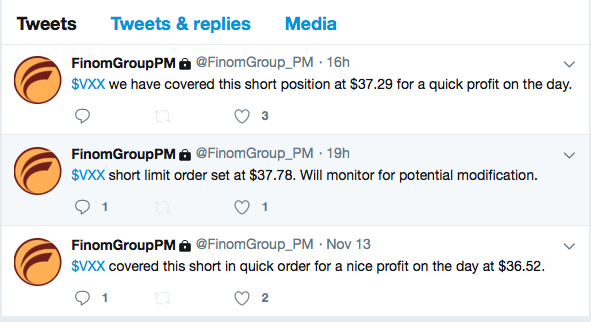

Regardless of what comes from the market action on Thursday, as always, I will look to trade when the opportunity represents itself. During the market’s heightened level of volatility, I have been building volatility exposure and trading the complex daily. The following screenshots identify these trades from the previous two days and through my private twitter feed at Finom Group (for whom I am employed).

Double like this.

Nice.