Interesting times lie ahead for 2026. Technology can't be expected to carry the markets again next year, and a decent correction - or more likely a sideways shift - is something to watch for. Given this slow down, there are 495 stocks (outside the top 5 tech stocks that have carried the index) in the S&P that look ready to take up the slack. The breakout in the equal weighted S&P should stick into 2026, but it will need to hold 7,795 breakout support (and 20-day MA) if this isn't going to morph into a 'bull trap' and a likely move back to 7,500. Such a move wouldn't be terminal, but it will leave traders scrambling for guidance.

The index best positioned to make a run is the Russell 2000 (IWM). It cleared its own breakout in mid December before it drifted back to $250 support. It will probably take until the New Year, when traders return from their holidays, before the index can reassert its authority - backed by some decent volume.

If the S&P and Nasdaq slow their respective advances off the back of weakness in technology stocks, then we can start to look for the next test of 200-day MAs, and ideally, an undercut to help mark the next major buying opportunity. In both indices, we are seeing a strong advance in their respective 200-day MAs that will help narrow the relative % gap between the index and this moving average. The S&P is trading at breakout resistance as both 20-day and 50-day MAs come up fast as potential catalysts for buying.

The Nasdaq is narrowing into an bullish, symmetrical triangle with technicals on the verge of returning net bullish. Given that, I would be looking for an upside breakout, but then we need to consider how far it can extend beyond its 200-day MA before we have to start looking for that correction again.

Driving the Nasdaq will be the Philly Semiconductor Index SOX. Since October, it has morphed into a trading range, and as of the end of 2025, it's caught in the middle. I have drawn two measured moves lower that would take it to around 5,400, and undercut its 200-day MA if 6,400 support was broken. I would view the support break a strong possibility for 2026, and more likely than a push above 7,500 (and its measured move target of 8,500); but the market will decide.

When we look at the Fib retracements for the Semiconductor Index on the monthly time frame, we see a primary target at the concentration around 5,400 and the 2024 peak, with a secondary (unlikley) target at 4,200.

(Click on image to enlarge)

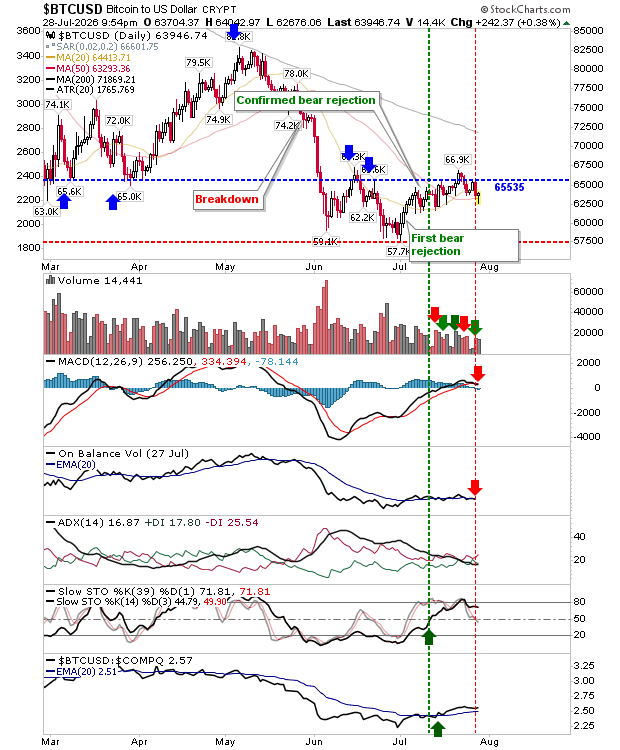

Bitcoin is in an odd position. It has sold off hard and is oversold, but the past few days have delivered two upward 'spikes' that point to supply and a desire for lower prices, but bears haven't been able to follow through on this. Add to this, technicals are returning bullish, most notably, stochastics [39,1].

As we look to weekly charts, we see a lateral shift in the trend, but no change in pace. The only difference is that support has turned resistance (for indices other than the Nasdaq), but all indces are hugging the line. Ideally, I would like to see 50-week MAs tested, as they were in 2023 (and lost in the early part of 2025), if only to reset the rally.

One of the struggles I have been tracking is the AAII Investor Sentiment survey. I have been looking for a shift to a net bullish trend in sentiment, as happened in the latter part of 2023, but there have been many false starts. Will this time be different? Note position of the two vertical blue lines. The one caveat is that the 2023 rally launched off the 200-day MA. If we see a comparable move here it will quickly become extended.

(Click on image to enlarge)

Volatility (VXN) has been suggesting a bounce in the making, which would be bad news for the Nasdaq/Nasdaq 100. This is the largest red flag for tech stocks as any bounce would last most of 2026 and send these indices spiralling. As things stand now, there isn't much room for this metric to go lower, so buyer beware.

Another metric to watch is the relationship between consumer staples and discretionary ETFs. We had a major 'buy' signal in 2023 (similar to 2009), and we now are running into the first of the overbought peaks as marked by the red circle (like in 2011). While it's hard to discern what happened in the S&P in 2011/12, what followed was a modest correction before the rally kicked off in earnest. This is the most bullish outlook for the index as it would suggest another major period of growth awaits the S&P, perhaps taking advantage of money shifting out of tech stocks.

(Click on image to enlarge)

Another bullish marker - this time for the Dow Industrials - is the Dow Theory indicator. When the relationship between the Dow Industrials and Transport index is rising, it's bullish for both indices. What I like about this is the bullish break in stochatics (red oval) to coincide with the successful double bottom in this relationship. There is lots of room for upside here, which is good news for the Dow.

Breadth metrics tell another story, but neither one that is bullish nor bearish. Nasdaq metrics are caught in the middle, with the most bearish being the Percentage of Nasdaq Stocks above the 200-day MA, which has struggled to get past the 50% mark. In addition, the Percentage of Nasdaq Stocks above the 50-day MA has recently dropped below 50%. Together, they reflect growing pressures in member stocks that could signal a broader decline. However, the most bullish metric is the Percentage of Nasdaq Stocks on point-n-figure 'buy' signals; this metric is key for driving breakouts in the index, and it's well positioned to help the Nasdaq to get to new highs as it sits close to 60%. Will there be one more push to a new all-time high before things turn sour again?

The 2-year yield curve tells a less bullish story. Yield inversion is never a good thing for markets. We saw a modest one before the subsequent market crash caused by the financial crisis. While I'm not sure we will see a crash, we have to consider a significant sell off cannot be ruled out. The current political climate has left the economy vulnerable to the kind of shock triggered by banking fraud in 2008. I would not be surprised if the Trump administration is allowing another one to develop under its watch. At the end of the day, markets don't tolerate bullshit, and if there is pain to deliver, it will deliver it.

If market indices do go pear shaped, there may be fresh opportunities in the commodity market. The Pring Infaltion:Deflation ratio has broken from a long term decline and is now in the early phase of a new bullish trend. This is a long term shift, and one to watch for the years ahead.

Higher commodity prices mean unhappy consumers. The Michigan Consumer Sentiment Index has been in the toilet, running at levels below that at the worst of the 2008 credit crisis. We are slso seeing a gradual uptick in unemployment. Together, a recession is the likely outcome, which will deliver its own shock to the indices.

(Click on image to enlarge)

So, we have a mix of metrics that give bulls and bears something to play with. I would argue, the more bullish metrics tend to be near term (i.e. for 2026) and the bearish ones influence beyond 2026. There may be an AI-driven crash driven by overinvestment in the sector (much like Y2K), but a leaner sector will emerge and it will bring about a new bull market. More likely to kill this market is a traditional financial scandal, driven by a lack of oversight from Musk's DOGE gutting and Trump's corruption. Investors should care nowt about with either; if you are investing for a pension, or have an investment window beyond 5 years, just keep on buying and take advantage of any selloff if offered.

More By This Author:

Breakouts In Russell 2000 And Equal Weight S&P Remain Stalled, But Not DefeatedLoses Undercut Russell 2000 Breakout, But No Real Damage Done

Breakout In Dow Jones Industrial Follows Yesterday's Breakout In Russell 2000

Comments

Log in or sign up to join the conversation.