With 13F season now over, it's time to take a look at Goldman's quarterly Hedge Fund Tracker which analyzes the exposure and positions reported by the hedge fund universe. Sadly for the "smart money", the results were ugly.

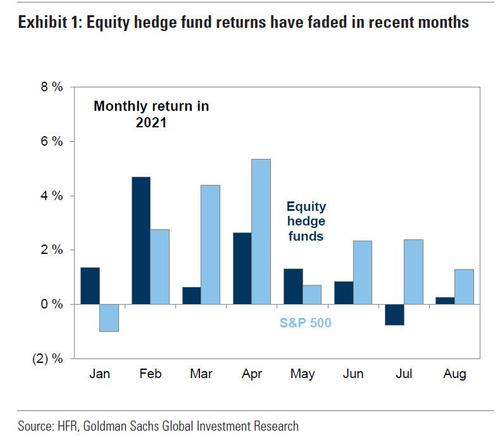

After a blistering start to 2021, when the surging market lifted all boats and longs (while crushing those parked in popular shorts such as GME and AMC) hedge fund returns have slipped in recent months according to Goldman's resident in house hedge fund expert, Ben Snider. Indeed, according to HFR, while the typical US equity hedge fund has returned 11% YTD, virtually all - or 10% - of that return was generated in just the first four months of the year with the last 4 months representing a painful grind for most hedge funds. The result is even worse for equity fundamental long/short hedge funds - according to Goldman's Prime Services desk, this universe has returned just 4% YTD.

There are several reasons for this startling underperformance, but the main ones are substantial exposure to China, underperformance of highly crowded tech names, and generally a lack of desire to reposition out of losers and into winners.

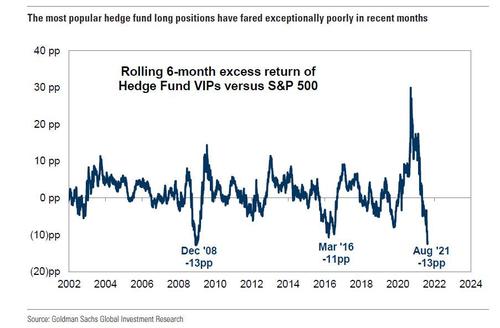

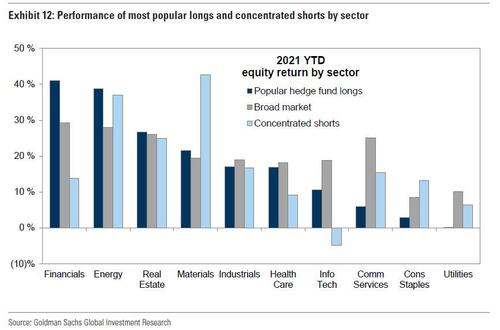

Before we dig deeper we will remind readers of our nearly-decade old market mantra of how to trade this broken market, first laid out in 2013: go long the most shorted stocks and short the most popular and crowded longs. This strat, which has generated significant alpha in 8 of the past 9 years, has continued to perform, and accordin to Goldman, "one factor weighing on hedge fund returns has been the extraordinarily weak performance of the most popular hedge fund long positions."

Indeed, Goldman's Hedge Fund VIP list (GSTHHVIP) has lagged the S&P 500 by 13% points during the past six months, matching the second half of 2008 as the worst six-month stretch for the basket relative to the market in its history of nearly 20 years. In other words, while the broader S&P is at all time highs, for most hedge funds this market is as bad as it was in the immediate aftermath of the Lehman crash!

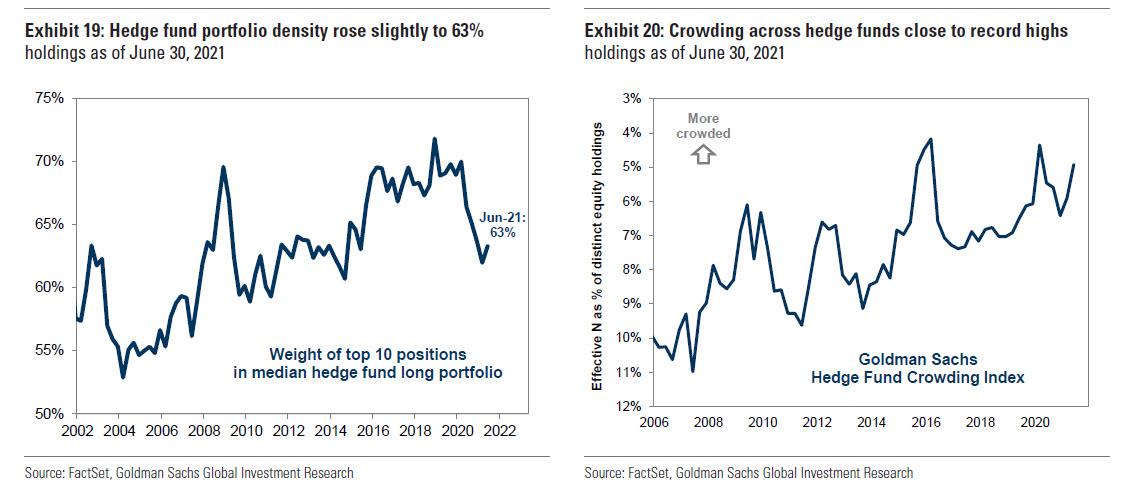

Perhaps some hedge funds did learn their lessons from the past year, and tried to avoid herding into especially popular positions, but most were unsuccessful and as Goldman adds, although hedge funds are currently less concentrated in their top positions than they generally have been during the last few years, the typical fund has over 60% of long equity assets in its top 10 stocks, underscoring the importance of VIPs for overall hedge fund returns.

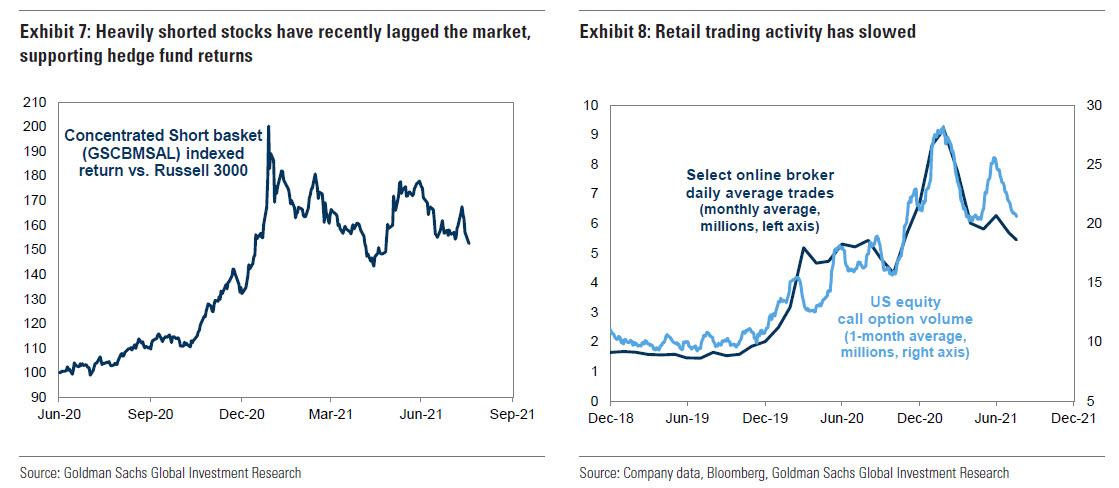

Meanwhile, a basket of stocks with the highest short interest as a share of float (captured by the Goldman GSCBMSAL ticker) has underperformed the S&P500 by 16% ince late June alongside a decline in retail trading activity.

Before we get into the composition of the VIP basket, a quick look at leverage and portfolio management.

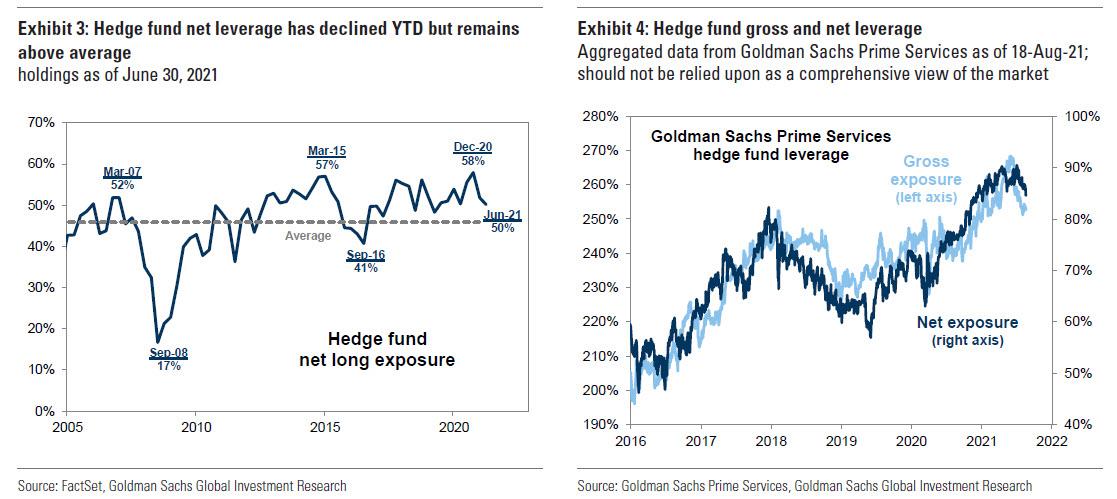

In contrast with other periods when the most popular long positions exhibited similar underperformance, hedge funds have maintained relatively elevated net leverage, convinced the fate of their favorite stocks will turn around. Aggregate hedge fund net leverage calculated based on publicly-available data registered 50% at the start of Q3, below recent highs but above the long-term average. Higher-frequency exposures calculated by Goldman's Prime Services desk show hedge fund net and gross leverage that have declined in recent weeks and now rank below averages of the past year but near the 80th percentile of the past three years.

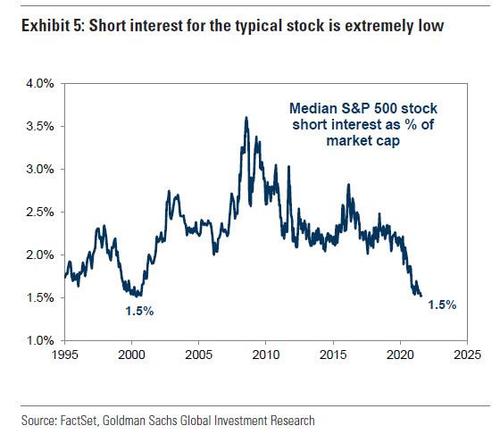

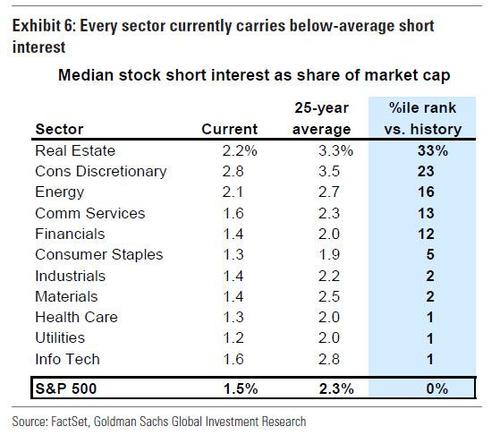

Mirroring the decline in hedge fund gross leverage, short interest across the market has continued to decline from extremely low levels. Drilling down, the median S&P 500 stock currently carries short interest equating to just 1.5% of market cap, matching the degree of short interest near the Tech Bubble peak in 2000 as the lowest on record.

Short interest in every sector ranks low relative to history.

On the other side of the book, while funds have reduced their short exposures after the Q1 short squeeze fiasco, the most concentrated short positions have recently lagged the market - contributing to hedge fund alpha – alongside a decline in retail trading activity. Online broker data and call option volumes indicated a resurgence in retail trading activity during June. At the same time, a basket of the most concentrated short positions (GSCBMSAL) outperformed the market. Since late June, however, measures of retail trading have declined, and the most concentrated short positions have lagged the broader market.

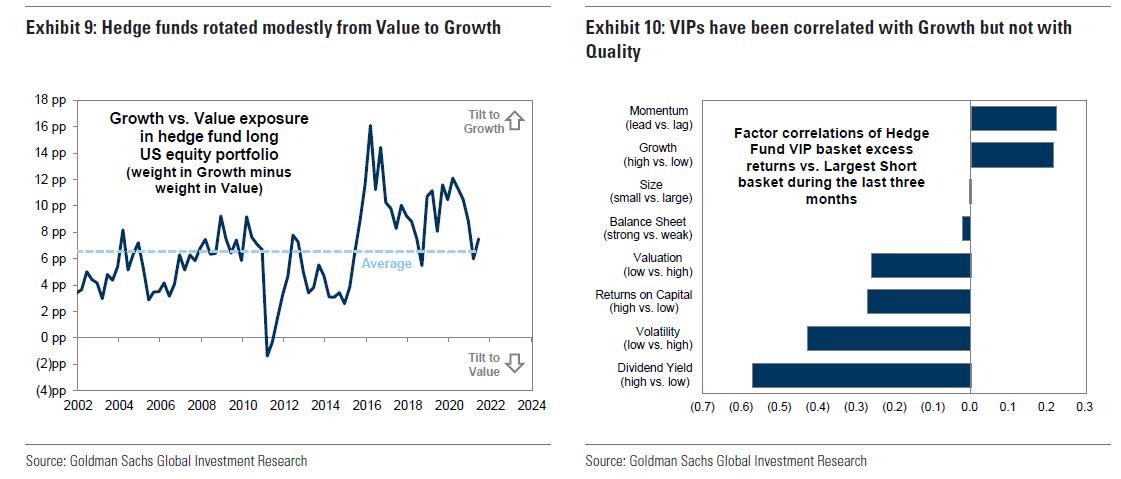

Shifting attention to the factor level, Goldman founds that funds inched toward Growth during 2Q, ending a sharp year-long rotation toward Value. Although the shift was small, the tilt to Growth in hedge fund long portfolios is now back above its 20-year average. Similarly, the excess returns of the bank's Hedge Fund VIP list have been positively correlated with Growth but negatively correlated with Value during the past three months. This Growth tilt has proven beneficial for fund returns; since the end of June our sector-neutral, long/short Growth factor has returned +3% vs. a -3% return for our Value factor.

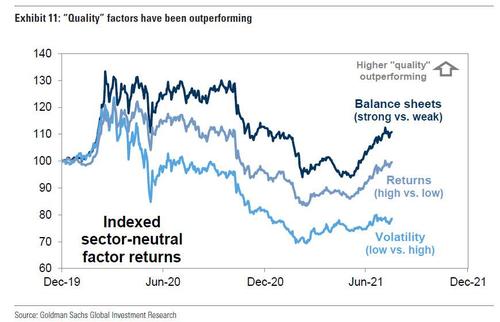

At the same time, however, the most popular hedge fund long positions have also been tilted away from “quality” factors, which have outperformed in the last few months. Hedge Fund VIPs have recently been negatively correlated with the bank's sector-neutral Balance Sheet, Returns on Capital, and Low Volatility factors, each of which has rallied since late in 2Q.

On a sector basis, the most popular hedge fund long positions have outperformed both concentrated shorts and the broad market in Financials, Energy, and Real Estate. However, these sectors represent a relatively small portions of all hedge fund portfolios, collectively accounting for jus 15% of hedge fund gross exposure. Indeed, Goldman's headline Hedge Fund VIP list contains just 3 Financials stocks (BRK.B, WFC, WLTW).

Next, we take a closer look at the core issue behind recent (and continuing) hedge fund underperformance: concentration, crowding and turnover.

According to Goldman, hedge fund portfolio concentration rose slightly in 2Q 2021 but remains far below pre-COVID levels. The typical hedge fund holds 63% of its long portfolio in its top 10 positions, slightly above the historical average but well below the 70% share at the end of 1Q 2020. Coinciding with the increase in concentration within hedge fund portfolios in 2Q, crowding across hedge fund portfolios also rose in the quarter, and Goldman's crowding Index now stands close to the highs registered in early 2016 and 2020. This is what happens when all hedge funds sit down at "idea dinners" to discuss the same handful of trades, and then put them on collectively at the same time.

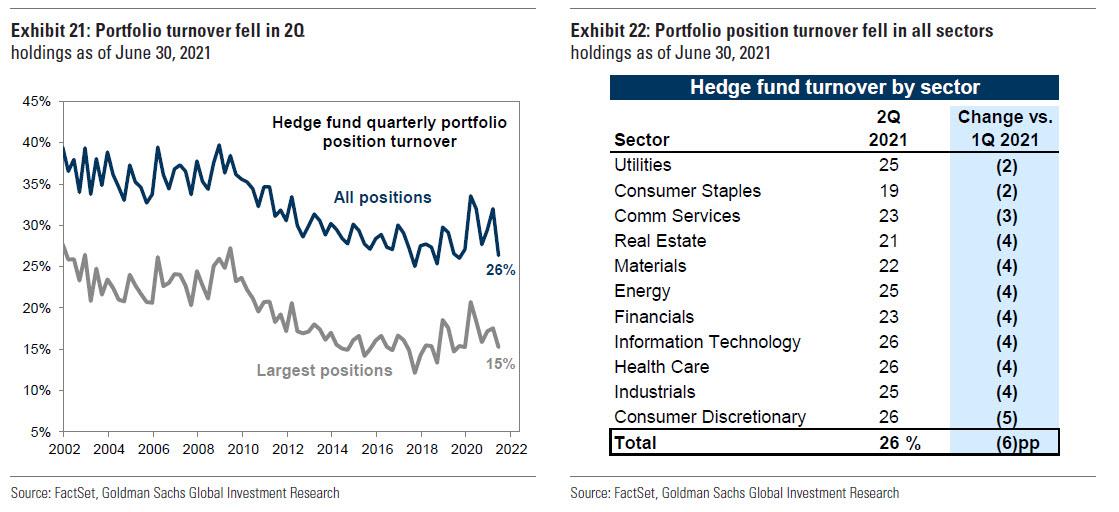

Another notable finding: portfolio position turnover reversed its recent trend and declined in 2Q 2021. The average fund turned over 26% of distinct equity positions in 2Q, and turnover decreased in all 11 sectors. This means that despite underperformance, most hedge funds did little to no changes to their top holdings.

With that in mind, we next shift to the two main reasons for the continued stock-picking agony among hedge funds: these can be summarizes as two - China and Amazon.

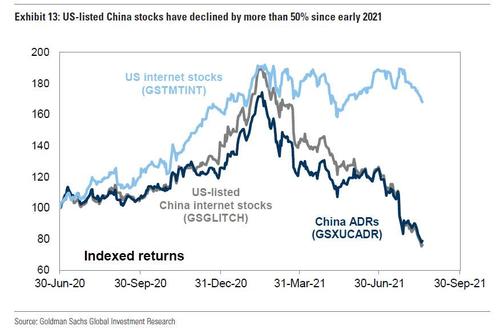

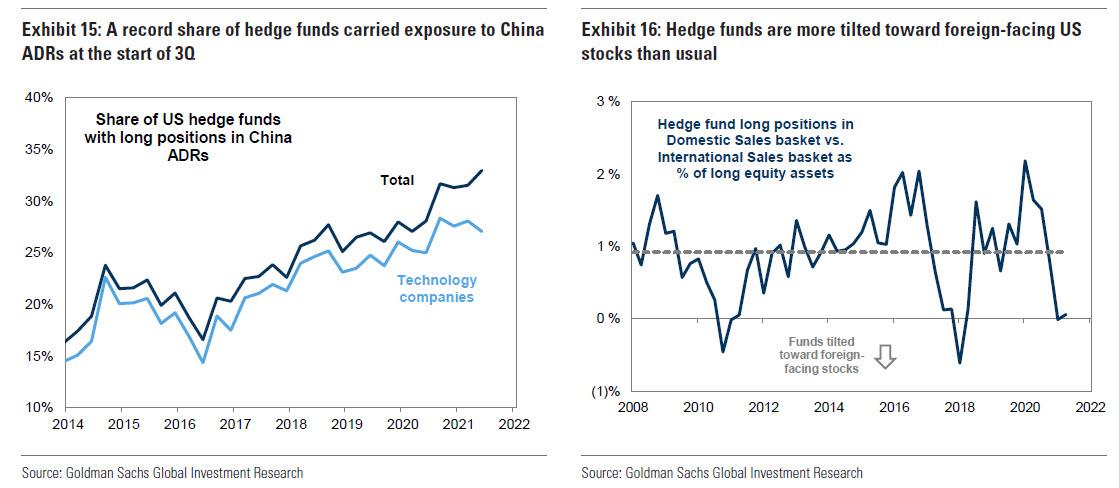

Looking at China first, the sharp declines across US-listed China stocks have been a significant headwind for hedge fund returns in recent months. One third of hedge funds in Goldman's analysis held a China ADR in their long portfolio at the start of 3Q, contributing to the recent headwinds against hedge fund returns. Since the middle of February, a basket of China ADRs (GSXUCADR) has declined by 55%, with all but one of the stocks generating a negative return (UXIN being the exception) and 40 of the 46 stocks declining by more than 20%.

Making matters worse, the group has declined by 37% since the end of June, the date of fund positions disclosed in the most recent filings, suggesting even more pain for hedge funds who refused to liquidate crippled Chinese stocks. According to Goldman strategists there is more than $300 billion in outstanding US institutional investor exposure to China ADRs.

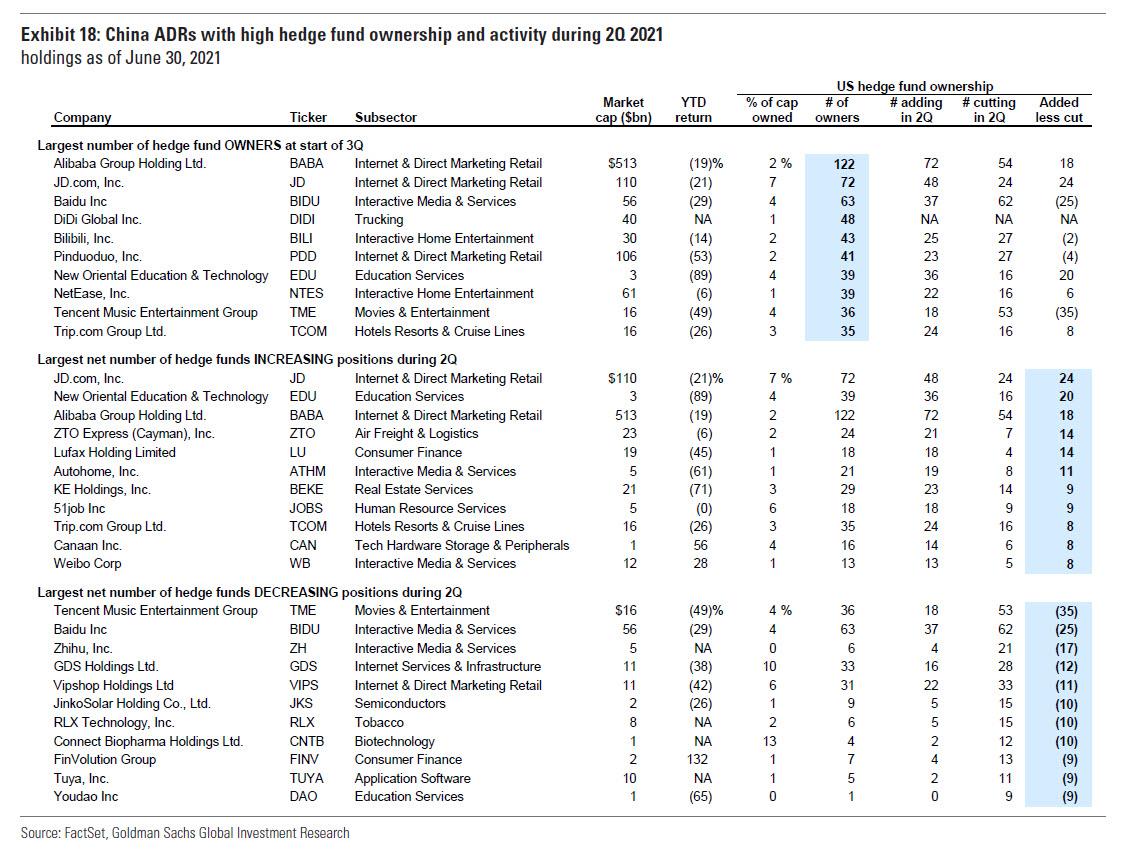

Some more details: at the start of 3Q 2021, a third of the US hedge funds in the Goldman sample held a long position in at least one China ADR. The overall popularity of China ADRs registered as the highest in data history, making clear that hedge funds were generally not prepared for the regulatory shift and its impact on share prices. Within the China ADR universe, BABA is the most popular hedge fund holding, and this quarter represents the 17th consecutive quarter in which BABA has ranked among the top 10 stocks in our Hedge Fund VIP list. However, this is the first quarter in three years that it lands outside of the top five. The other most popular China ADRs: JD, BIDU, DIDI, BILI.

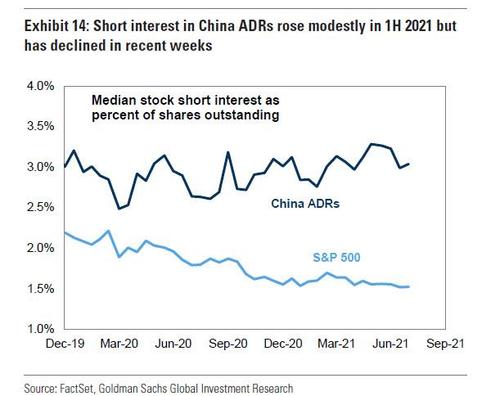

While hedge fund ownership of China ADRs was more widespread than ever at the start of 3Q 2021, some signs of rotation away from these stocks began late last year (especially among a handful of funds prudently got out of China as we noted earlier this week). The share of hedge funds with a long position in a China technology ADR peaked in 3Q 2020, well before share prices began to decline in February 2021. Similarly, short interest in the median China ADR has trended higher since last summer, in contrast to the decline in short interest across S&P 500 companies. In the last few months, however, short interest in China ADRs has declined alongside falling share prices.

The most popular China ADRs among hedge funds outperformed less popular ADRs in 2H 2020, but have sharply underperformed YTD, suggesting selling pressure as funds reduced their exposures. The 25 China ADRs with the largest number of US hedge fund owners outperformed in 2H 2020 but returned -7% in 1H 2021, compared with +42% for the 25 least popular ADRs. Since the start of 3Q, however, each group has declined by roughly 30%.

Summarizing, the table below shows the most popular China ADRs in US hedge fund long portfolios at the start of 3Q. In addition, it shows the stocks with the largest net increases and decreases in ownership during 2Q 2021, calculated as the number of funds adding new positions or increasing existing positions less the number of funds reducing or eliminating positions.

Extensive China exposure aside, the other key factor behind the hedge fund drubbing is the continued overexposure to tech and growth. As shown in the chart below, the “FAAMG” stocks are the top five names in the Hedge Fund VIP list. Within the group, AMZN ranked as one of the “Rising Star” stocks with the largest increase in hedge fund popularity last quarter while MSFT landed in Goldman's “Falling Stars” list of declining popularity (one wouldn't know it judging by its performance today).

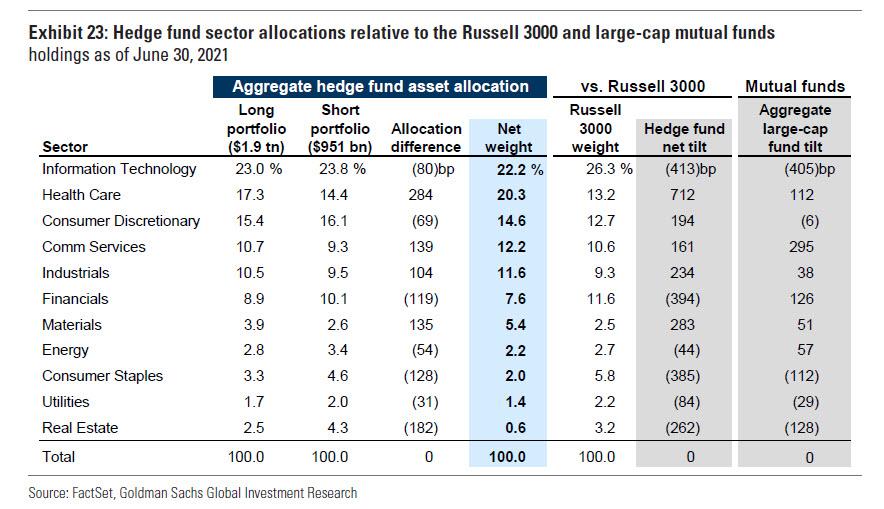

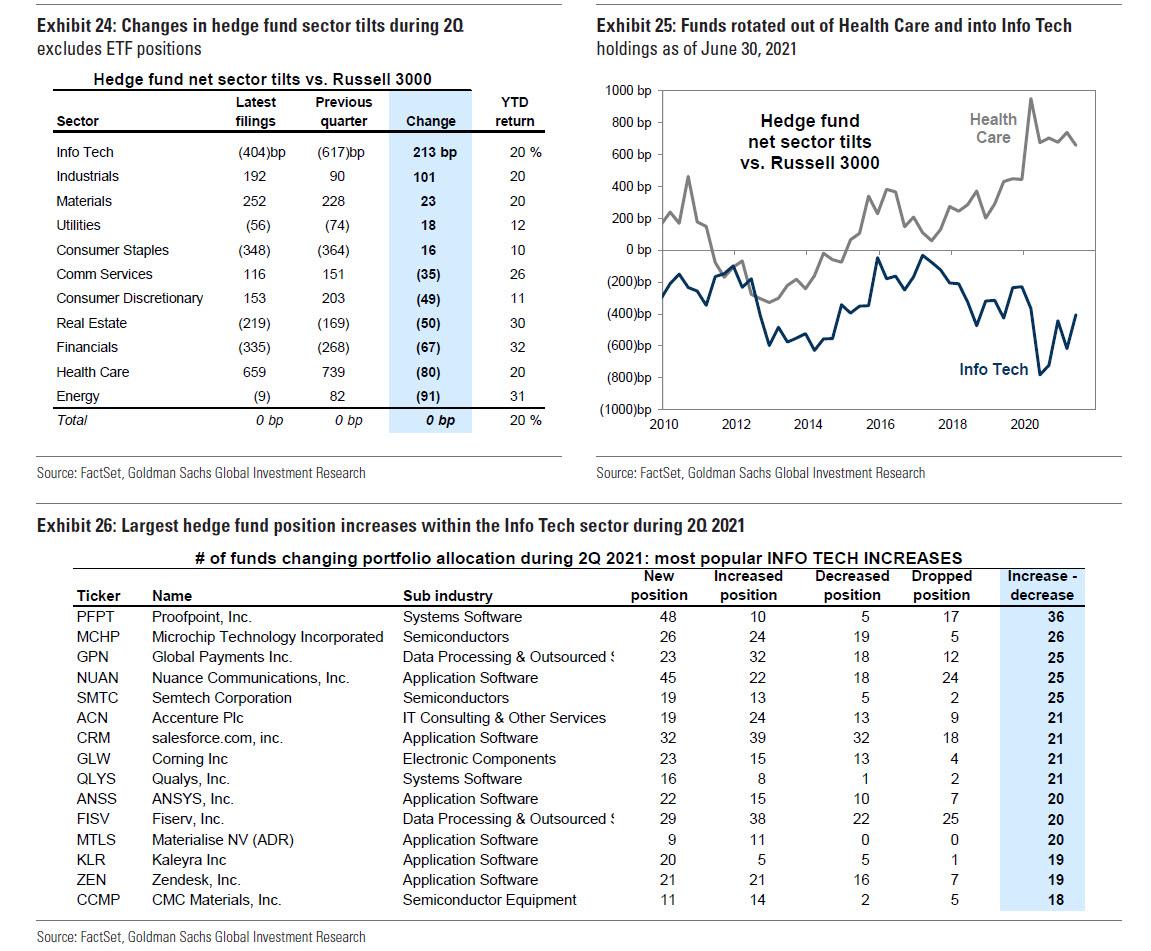

With the 5 most popular hedge funds stocks all FAAMGs, it's not surprising that Info Tech represented the largest sector net exposure (22%) on a sector basis, but the largest underweight (-413 bp) relative to the Russell 3000. Health Care Tech represents 20% of funds’ net exposure and is the largest overweight (+712 bp). Hedge fund and mutual fund sector tilts are generally in the same direction, with Financials representing a notable exception: Mutual funds carry a large overweight in the sector, but hedge funds have a net underweight tilt relative to the Russell 3000.

In Q2 hedge funds further increased their tilts in Info Tech and Industrials but rotated away from Energy, Health Care, and Financials. Changes in hedge fund net tilts this quarter were inconsistent on a style basis. Funds lifted exposure to pockets of cyclical, secular, and defensive stocks, reflecting the heightened ongoing degree of investor uncertainty regarding the macro outlook.

The 213 bp increase in the net Info Tech tilt came partially at the expense of Health Care, consistent with the recent trend. The rotation into Info Tech was primarily driven by Software, as funds piled back into secular growth favorites amid the decline in interest rates. Eight of the 15 Info Tech stocks with the largest net hedge fund additions in the quarter (new positions + increased positions - cut positions) were from the Application Software and Systems Software subindustries (Exhibit 26). Funds still carry a large underweight in Info Tech relative to the Russell 3000 as a result of its large weighting in the index.

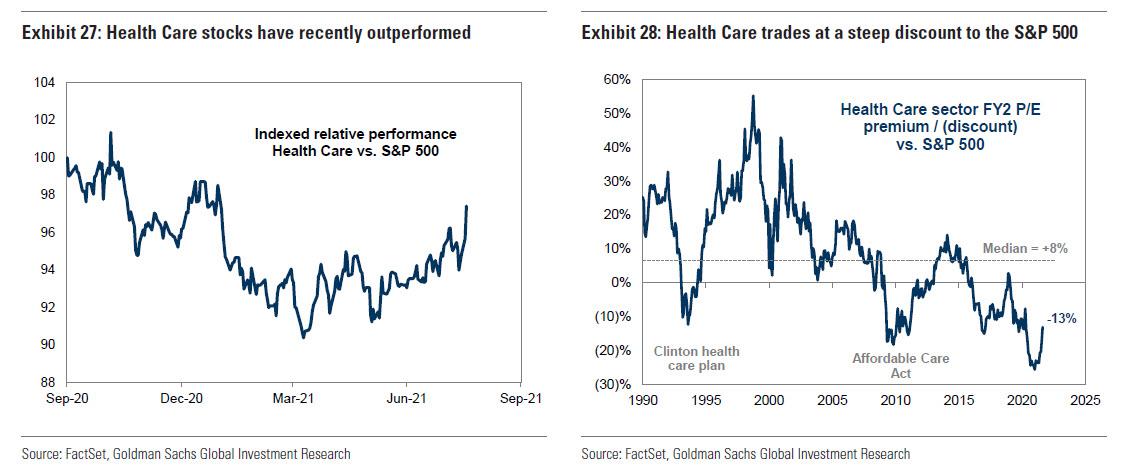

While nowhere near as sexy as tech, Health Care has outperformed the S&P 500 by 7% since June, boosted in part by economic growth concerns. Even following its recent outperformance, Health Care trades at a 13% P/E valuation discount to the S&P 500, close to the largest discount on record and rivaled only during other periods of regulatory policy uncertainty.

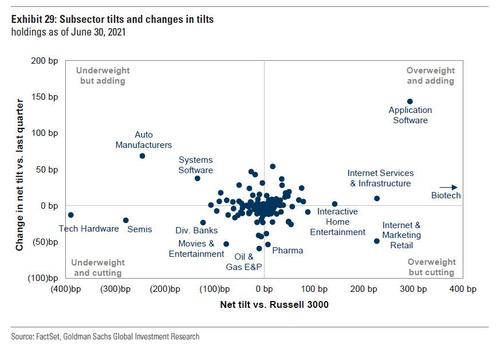

At the subindustry level, hedge funds generally increased length to areas with perceived secular growth, consistent with the broad factor rotation noted in Exhibit 9. Funds added to overweights in Application Software and Systems Software while cutting exposure to cyclical subindustries such as Oil & Gas Exploration and Production, Diversified Banks, Tech Hardware, and Semis.

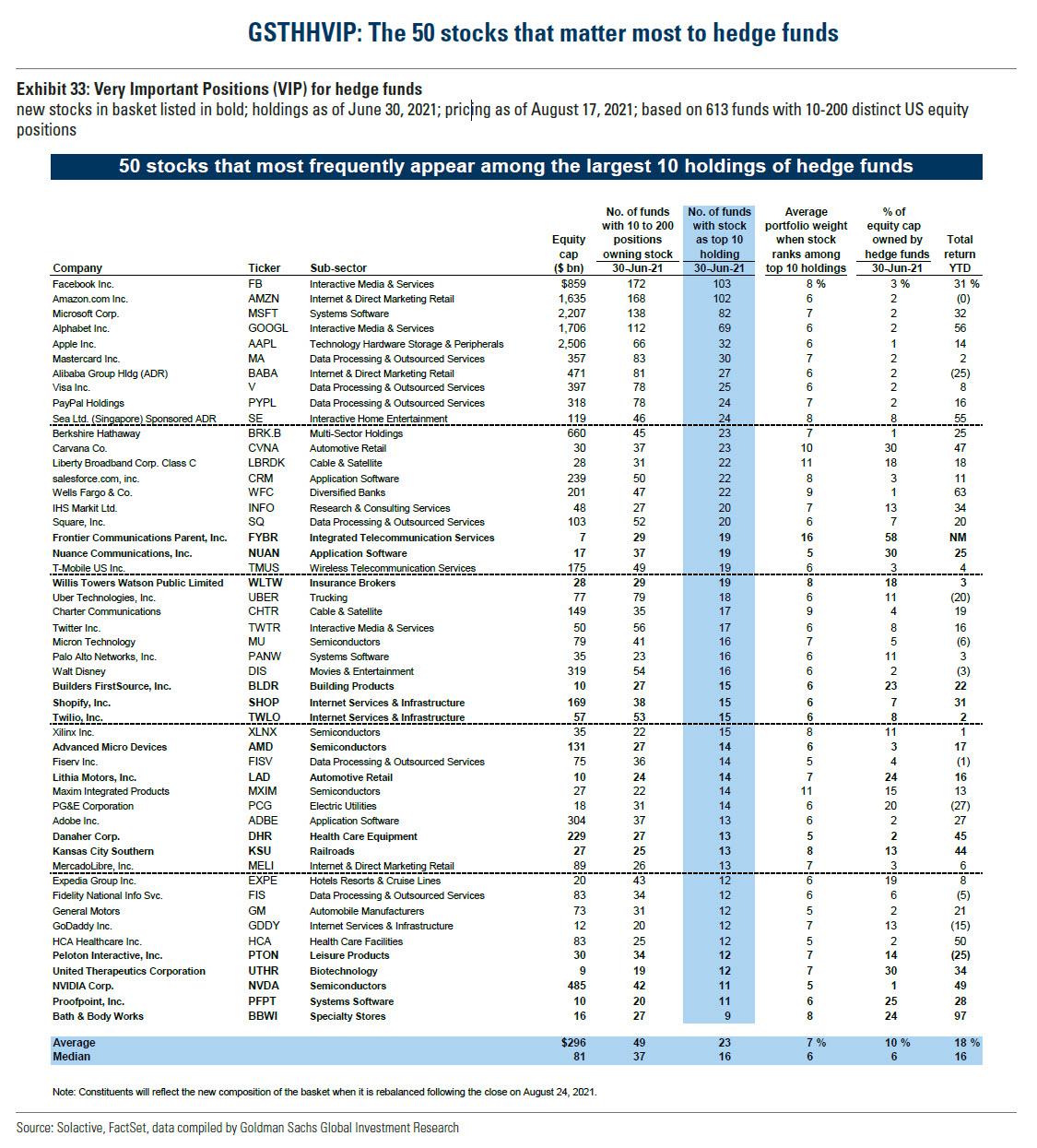

Finally, we get to what matters most: the Hedge Fund VIP List (ticker: GSTHHVIP) which contains the top 50 long positions of fundamentally-driven hedge funds. These “stocks that matter most” are the positions that appear most frequently among the top 10 holdings within hedge fund portfolios.

And so without further ado, here are the 50 most popular VIP names for hedge funds:

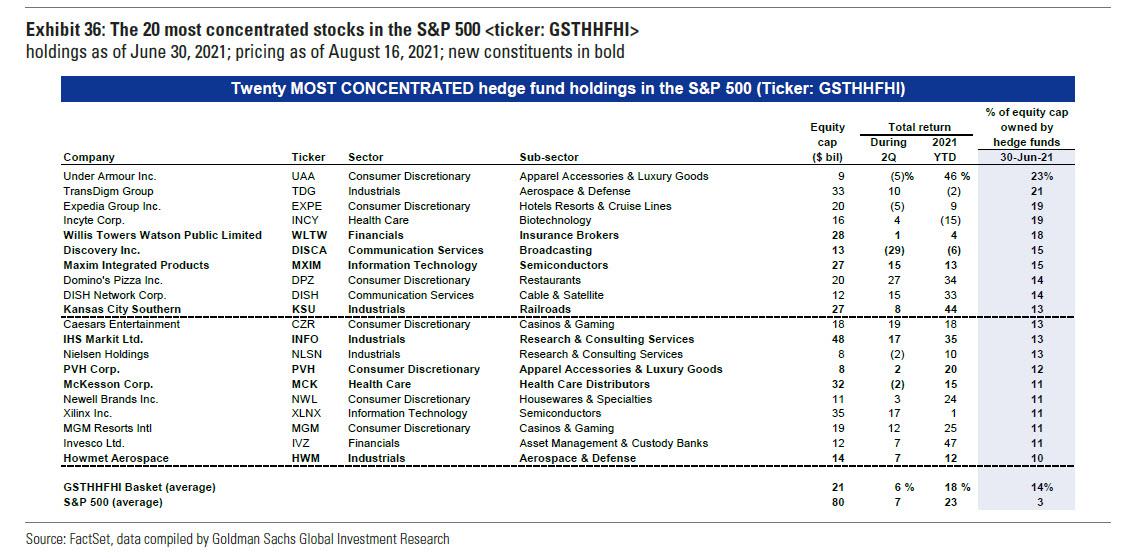

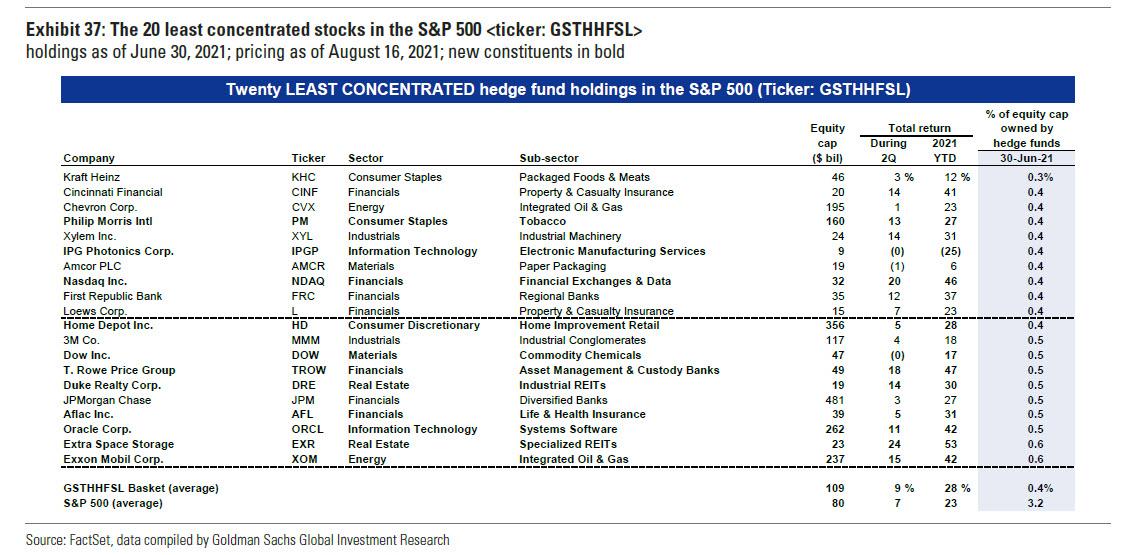

Separately, here are the 20 "most concentrated" names, those stocks who have the highest hedge fund % ownership of their market cap.

Of course, regular readers will know that the best trade here is to continue shorting these extremely popular and/or crowded names in a pair trade with either a long basket of Goldman'st least concentrated names...

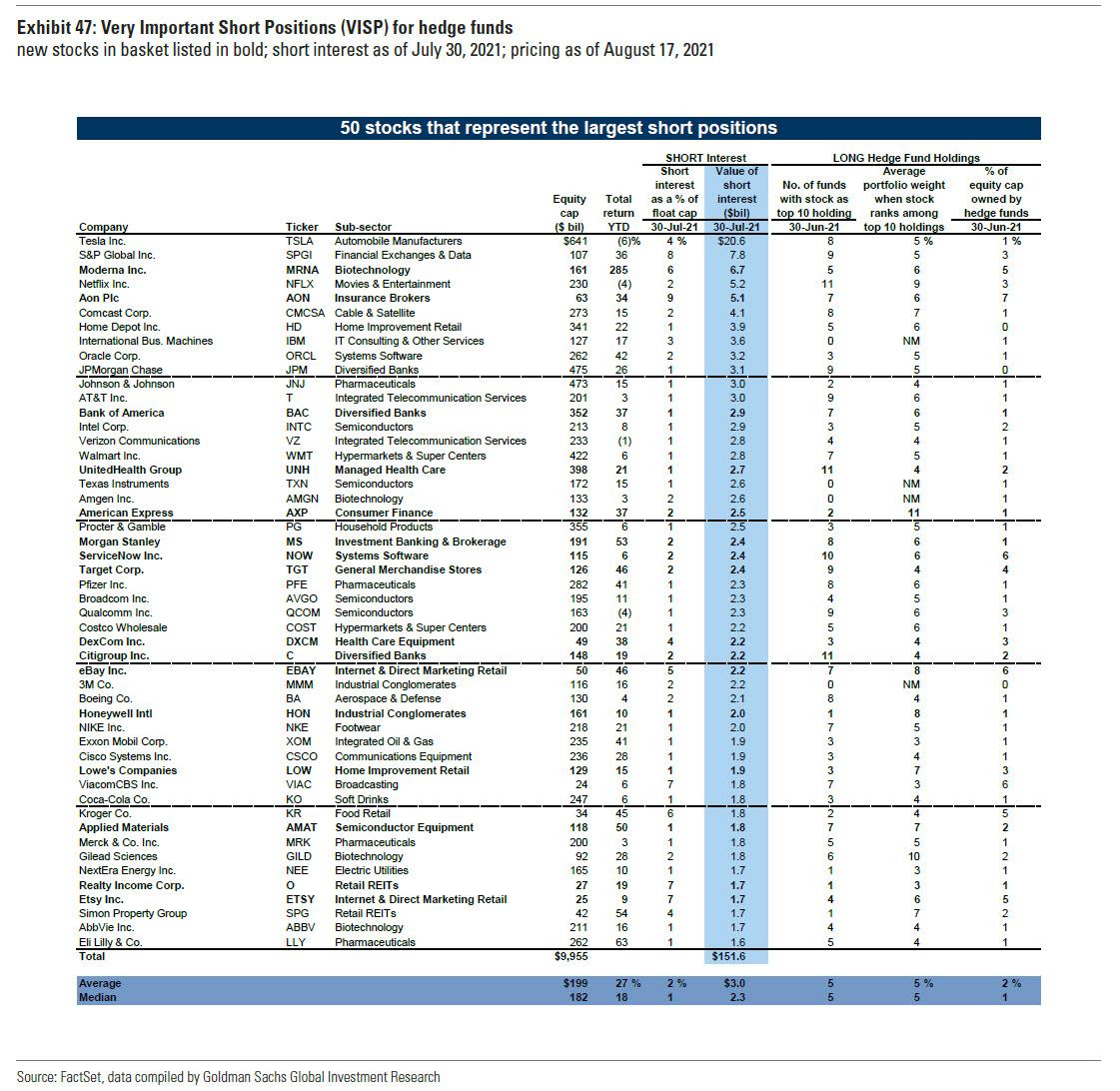

... or the most shorted ones, shown below.

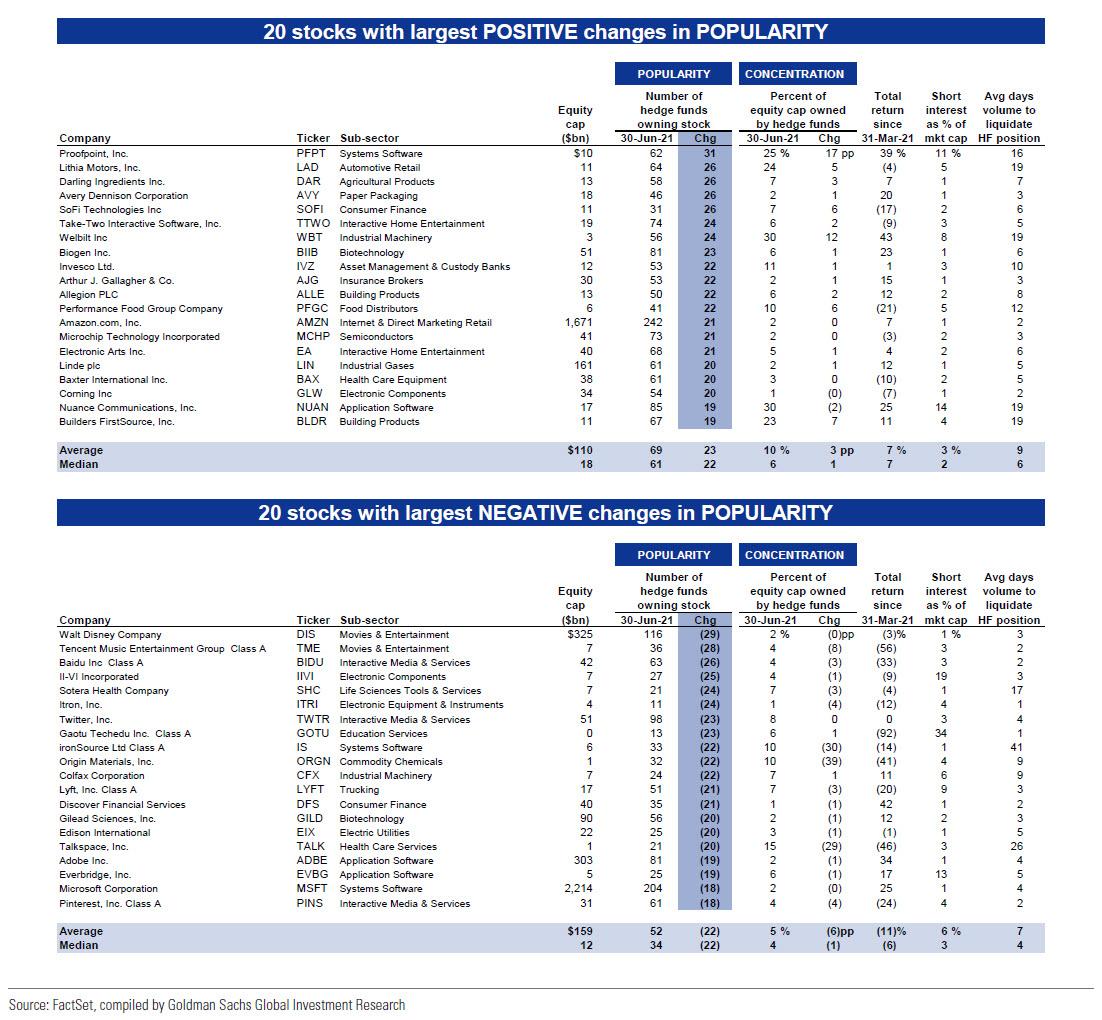

One bonus chart: here is the list of the 20 stocks with the largest positive and negative changes in popularity.

Comments

Log in or sign up to join the conversation.