Defensives are out, animal spirits are in… again. Or so the latest rotation among US equity sectors suggests, based on a set of ETFs through Monday’s close (Nov. 11).

The recent rush into utilities stocks (XLU) has reversed in recent days while prices have surged for communications services (XLC) and financials (XLF), which are now neck and neck as the top-performing equity sectors year to date.

What’s changed? Donald Trump’s election victory last week.

“The stock market loved the election outcome. But there is nervousness in the bond market. It’s more worried about the size of deficits and the possibility of inflationary tariffs,” says David Kotok, co-founder and chief investment officer at investment management firm Cumberland Advisors.

Ark Invest CEO/CIO Cathie Wood wrote on X yesterday: “Deregulation (defanging the SEC, FTC, and others), government spending cuts (making room for the private sector), tax cuts, and a focus on technologically enabled innovation are likely to turbocharge the US economy more powerfully than during the Reagan Revolution.”

Meanwhile, Yardeni Research president Ed Yardeni predicts the S&P 500 Index will surge by two-thirds by the end of the decade. “We’re just seeing a more pro-business administration coming in that undoubtedly will cut taxes,” Yardeni tells Yahoo Finance. “And not only for corporations but also for individuals. Lots of various kinds of tax cuts have been discussed. And in addition to that, a lot of deregulation.”

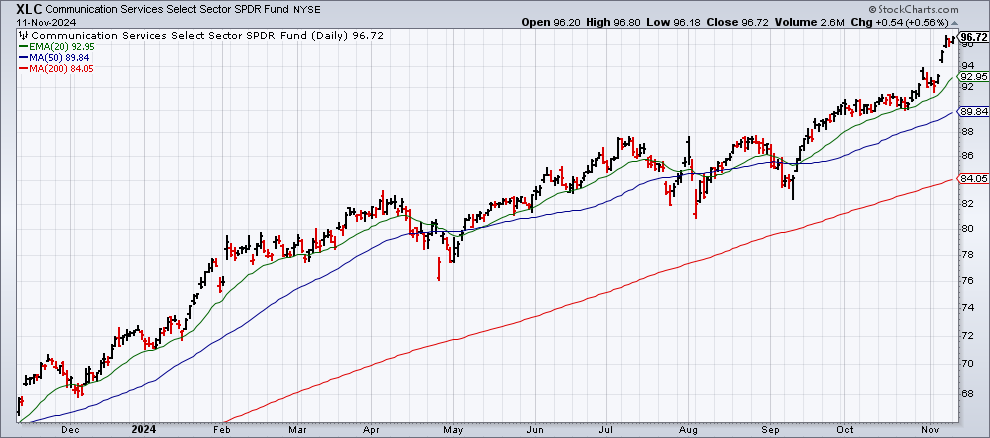

Changes in sector leadership appear to be on board with the bullish attitude adjustment. The Communication Services Select Sector SPDR ETF Fund (XLC), which holds the consumer-driven likes of Meta, Alphabet and Netflix, gapped up in recent days and is now up a sizzling 34.2% this year, fractionally ahead of financials (XLF) and well ahead of the broad market (SPY) and utilities (XLU).

What could go wrong? A the top of the list of troublemakers: fiscal and inflationary headwinds may dent if not derail some of Trump’s plans for policy.

“The top priority is extending the Trump tax cuts and the signature part of his program. I think that should be easy to pass in Congress, particularly if the Republicans control the House as well,” says former Donald Trump Treasury Secretary Steve Mnuchin.

The challenge is that tax cuts and other policy priorities that Trump advocates – raising tariffs and deporting millions of immigrant workers – could juice inflation. Add in heightened concerns about the US government’s deepening budget deficit and it’s fair to say that the Trump and Republicans face a tricky path next year in terms of reaction in the bond market, which is growing concerned about inflation and fiscal risk.

Another potential concern for the market is the politicalization of monetary policy. Trump believes he should a degree of influence over the Federal Reserve. “I think I have the right to say, ‘I think you should go up or down a little bit [for interest rates,’” the president-elect said at the Chicago Economic Club last month. “I don’t think I should be allowed to order it, but I think I have the right to put in comments as to whether or not the interest rates should go up or down.”

For the moment, the stock market is paying little if any attention to the recent pop in Treasury yields. The 10-year yield has increased 70 basis points since mid-September to 4.31%. That’s still well below the 5% peak for this cycle to date reached in late-2023. But if the benchmark rate continues to approach its previous high, the bond market could take away the punch bowl at the stock market’s party.

More By This Author:

Will Reflation End The US Bond Market’s Recovery?

Risk-On Sentiment For US Stocks Accelerates

How Will Trump’s Election Win Change The Macro Outlook?

Comments

Log in or sign up to join the conversation.