Embracing Bears

Anyone for a different song?

“Alternative views are dismissed not after consideration, but upon contact. Facts are rejected even as they are offered. Perspectives and evidence are repelled somewhat like a magnet repelling iron filings.”

Matthew Syed, Rebel Ideas.

This is an excerpt from the un-put-downable Rebel Ideas by Matthew Syed (link will take you to a relevant excerpt). The basic premise of the book is the increased collective intelligence of a diverse group of minds is something that everyone should embrace. However homophily, in essence the desire to associate with one’s own kind, is a powerful evolutionary defence mechanism which has become hard wired in human behaviour. To make the point Syed goes on to describe a psychological experiment where students are offered hard cash to read articles which are directly contrary to their own views; the upshot is even with a tangible reward they dont.

Don’t Upset Your Customers

So how do NMC, Burford, Kier Group, Fevertree and Cineworld link to this thought process. What does this motley crew have in common other than very disappointed investors? The answer lies in the analyst community that followed the stocks and was in charge of giving recommendations. Prior to the collapse of all these share prices, the vast majority of analysts paid to give forthright and independent views on the worth of these businesses rated them as buys: no one entertained a sell.

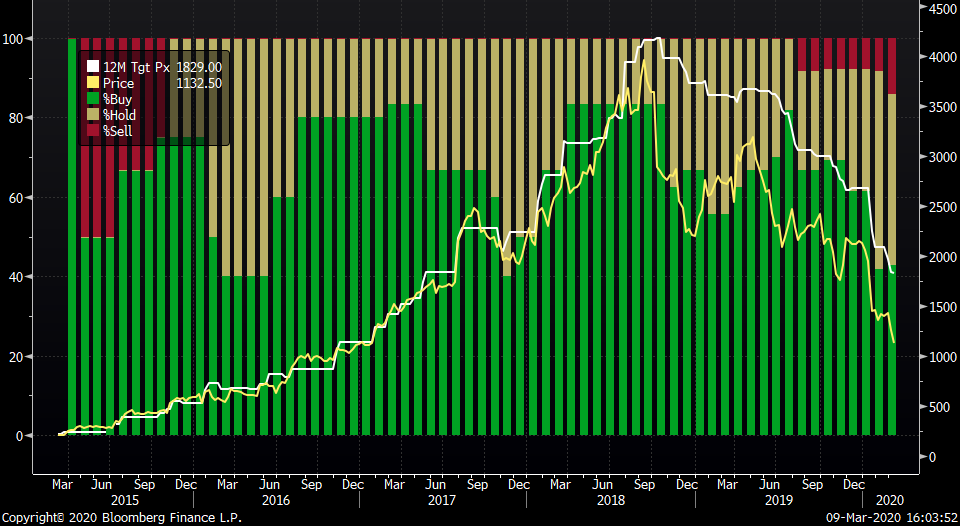

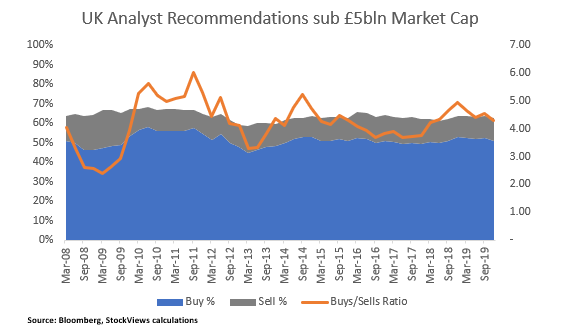

Fevertree Analyst Recommendation: Buy at the highs, Sell at the lows

Advocating that a stock is valued less than its current worth has never been a fashionable pastime in an industry that has made money out of growing asset bases. This is anathema to the whole concept.

- For a start the end user of the research recommendation, the professional investor, is ultimately paid a management fee on the absolute value of the assets they are holding, so you are implicitly telling them their fees are going to fall.

- Secondly, that investor generally has no choice but to deploy capital into markets. Telling that person to sell presents them with the conundrum of having to find something else to buy.

- Furthermore the bank employing that analyst will be hoping to undertake some form of primary capital market business with the company in question.

- Finally, assuming your firm has a trading business you are also lowering the ultimate commission “cut” you might make from any secondary trading…what’s the point!?

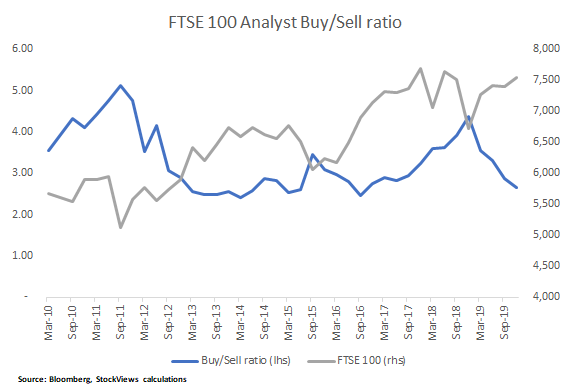

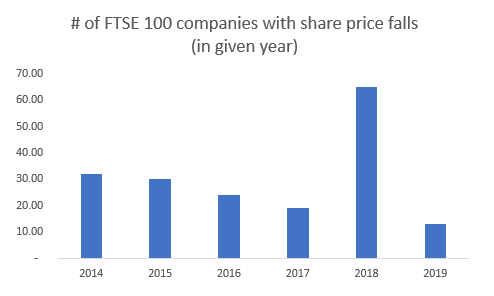

Hence the ratio of buys/sells for the FTSE 100 shown below hovers around 2.5x to 5x. Consider that at the beginning of 2018 the proportion of sells was 15% despite the fact that in that year 60% of companies saw a share price fall.

Midcap myopia

With the onset of Mifid2, the splitting out of research costs, this has exacerbated that situation, especially in the smaller market cap spectrum. In one sense commission trading is less linked to research recommendations, however the incentive skew has overwhelmed that potential positive.

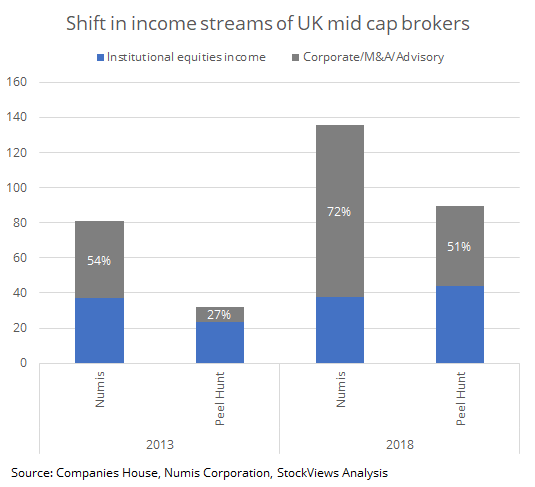

Due to the enormous reduction in the pool of “institutional equity income” (ie trading and research revenue), the corporate advisory and capital markets divisions make up the lion’s share of profits for many research firms (we have used this chart before in a post on Mifid’s unintended consequences but it seems relevant to bring it in again).

How many listed companies are going to choose a firm for primary business that actively recommends its share price should be lower? Certainly the CEO, whose large incentive package will be linked to some form of 3yr TSR, wont be too pleased. That is supported in the disclosures that research firms now give: for an unnamed European mid cap specialist 50% of recommendations are Buy (40% hold) but for corporate clients that rises to 77%, for a smaller UK specialist the number rises to 93% buys for corporate clients. This has led to the ratio of buys to sells in UK mid caps comfortably in the 4:1 to 5:1 zone.

Lessons from the Best

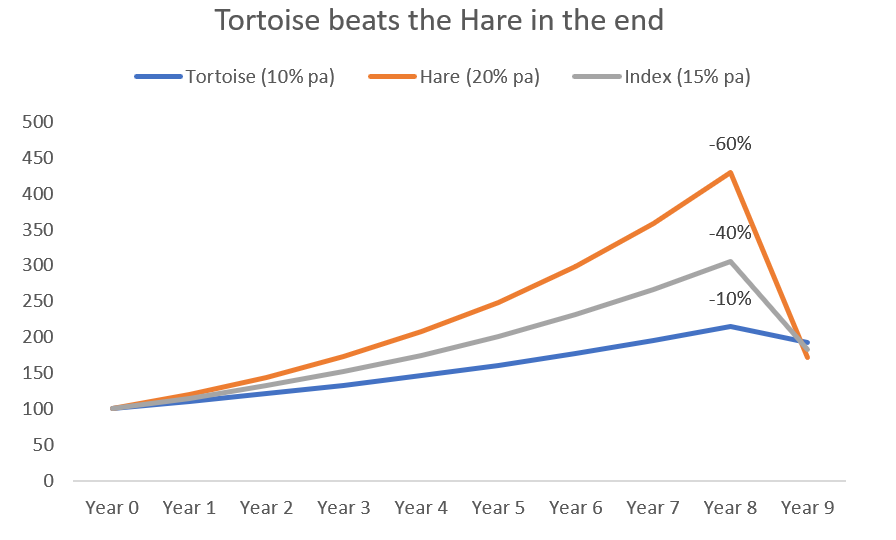

The bizarre thing is that history and mathematics show us that it is actually what happens in a negative year that really defines one’s long term track record.

Consider two funds: Hare and Tortoise against an Index Y. The index compounds at 15% per annum for 8 years. Tortoise Fund underperforms the index by 500bps every year compounding at 10% whereas Hare Fund blows the lights out, beating the index by 500bps, delivering 20% p.a. returns. At the end of year 8, Tortoise Fund has doubled your money up 114%, the index is a two bagger up 200% whereas Hare Fund looks like a hero; up 330%.

The problem comes in year 9, the index is -40% in a catastrophic year (they do happen) and Hare Fund falls -60% in that year because of owning all the stocks which everyone rushes to sell. Tortoise, having avoided a lot of the excess is -10% in that year. The outcome isn't immediately obvious but is shown in the chart below. Tortoise now comfortably leads the pack vs the index and Hare.

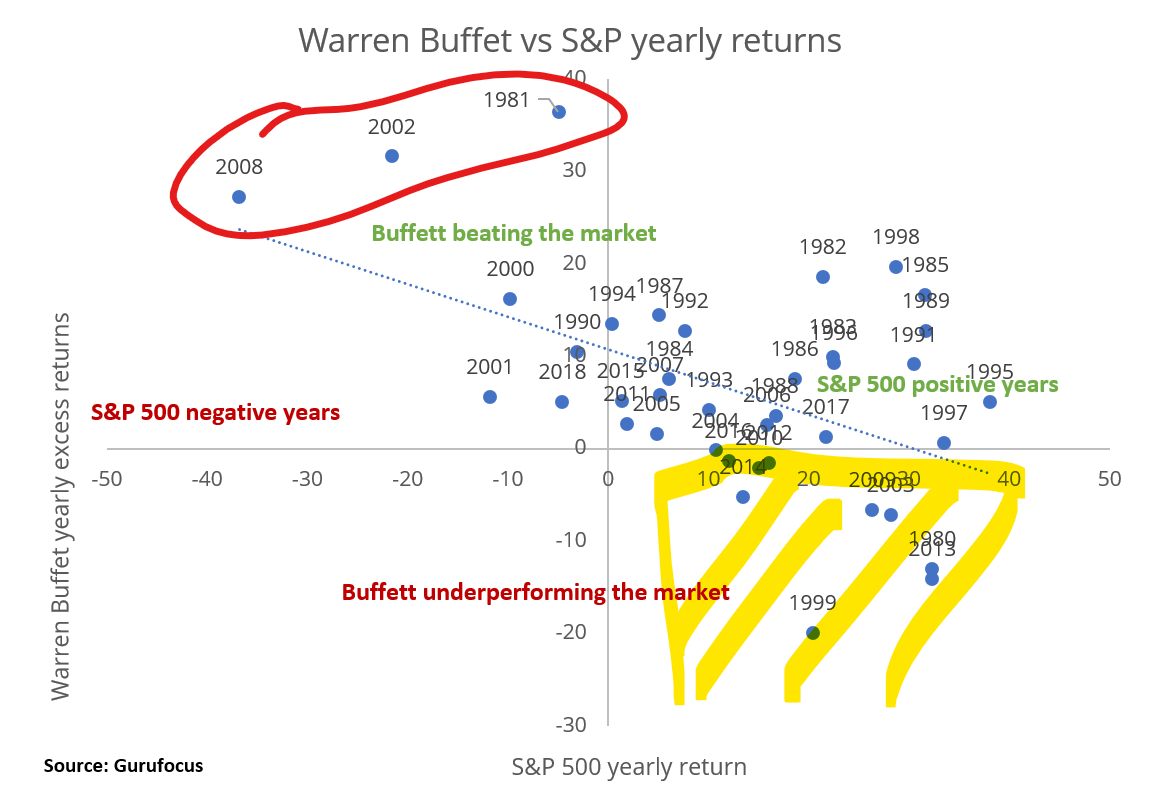

This illustrative example isn’t just that, but actually demonstrable in the returns of the greatest investor of our time Warren Buffet. If you look at the excess returns that Warren Buffet has delivered over the last 30+ years vs the S&P 500 you will find the following. That the three greatest years of outperformance were all in negative index years, secondly you will see that all the underperformance periods are found in positive index years. In other words it is no problem underperforming in up years, it is the down year when things matter.

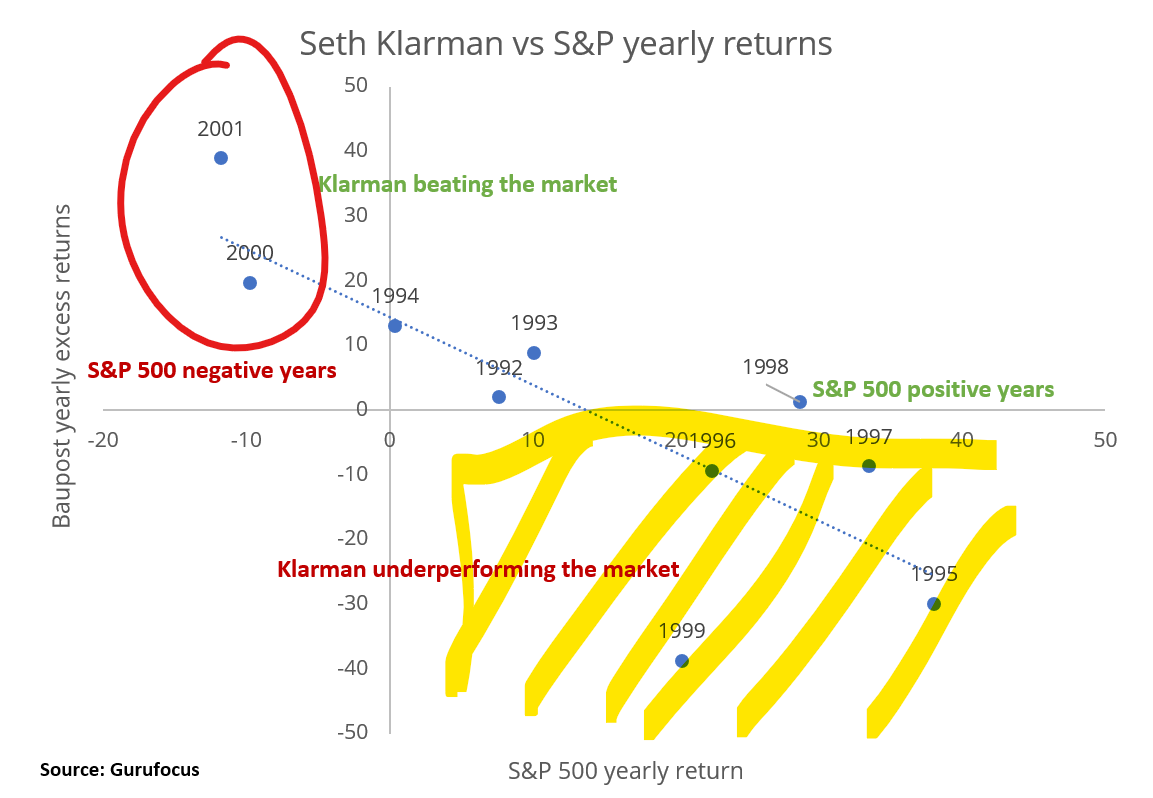

The same is visible in the data available on Seth Klarman’s Baupost. Klarman’s Margin of Safety approach is something we find very appealing at StockViews with this downside scenario valuation backstop a critical part of trying to understanding risk/reward trade offs. Again Klarman’s best years were during the unwind of the dotcom bubble.

Hugging a bear

Returning to the initial quotes on diverse thinking from Matthew Syed the practical point to make is that reading and listening to the views of those who have a contrarian opinion and believe a stock is a sell can only make you a better investor and thinker. Instantly shutting out that work is both dangerous to the construction of your portfolio and detrimental to one’s own development.

Final words come from another investment guru, Ray Dalio, via his recent Principles book which is full of wisdom encapsulated by the below:

“Being radically open-minded enhances the efficiency of those feedback loops, because it makes what you are doing, and why, so clear to yourself and others that there can’t be any misunderstandings…Being radically transparent and radically open-minded accelerates this learning process. It can also be difficult because being radically transparent rather than more guarded exposes one to criticism.”

Disclosure: None.

Have something to say on a recent acquisition or merger? Let us know your views on the StockViews platform!