Housing is among the most interest-rate sensitive sectors of the economy. It’s also one of the most cyclical and crucial inputs for the business cycle. On that basis, one could reasonably expect that the sharp runup in interest rates over the past two years would have crushed the trend in housing prices. For a while that was the effect, but the dramatic slide in the year-over-year change in US house prices is accelerating again. The reflation is moderate so far, at least compared with 2021-2022. But it’s notable that housing prices are once more looking resilient after the Federal Reserve’s most aggressive tightening policy in decades and before rate cuts have arrived.

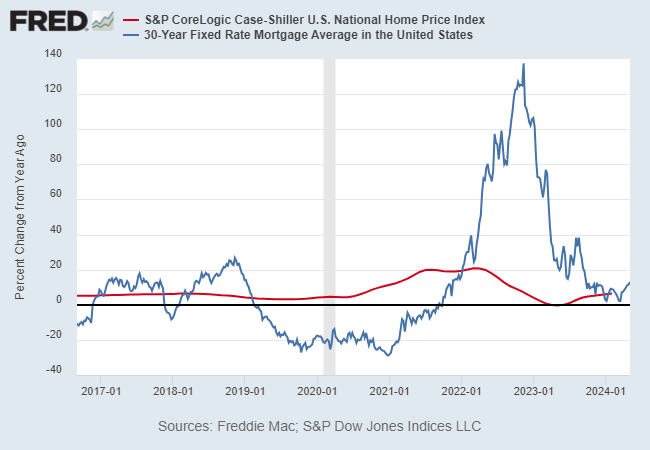

Recent history tells the story. After the Fed began raising interest rates quickly in early 2022, the 30-year mortgage rate rose sharply, more than doubling by late-2022 vs. its year-earlier level. The strong year-over-year rise in housing prices at the time soon took a hit, falling from roughly a 20% annual increase in late-2022 to flatlining in 2023. But in recent months housing prices have revived, and are increasing more than 6% a year, based on S&P Core-Logic US National Home Price Index.

The revival in a firmer housing price trend is striking for several reasons. First, it arrives before the Fed has started cutting interest rates. In fact, market expectations for rate cuts have been pushed further into the future and so any relief for housing in the form of lower borrowing costs is on track to be delayed.

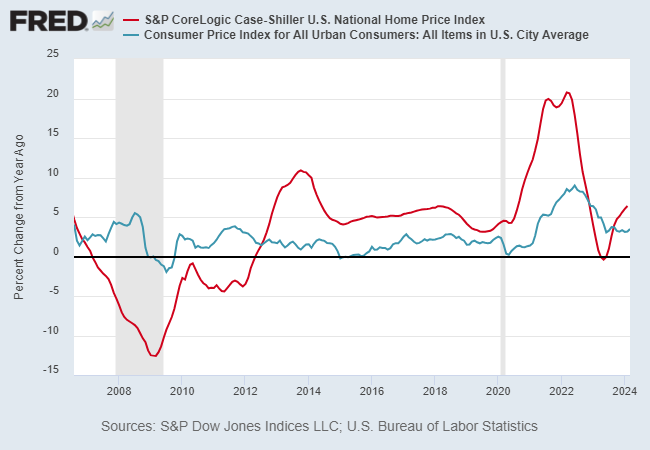

Meanwhile, the year-over-year change in housing is once again rising at a rate that’s faster than consumer inflation. That implies that housing is again a contributing factor to the sticky inflation problem the Fed is grappling with this year.

Another implication is that once the Fed starts cutting rates, which may start as early as September, according to Fed funds futures, policy easing could further strengthen the recent revival in housing inflation, which would contribute to the sticky inflation challenge.

The reflation in housing prices is also conspicuous because it’s again rising faster than year-over-year economic growth, based on nominal GDP. US output rose 5.4% in the first-quarter vs. the year-ago level – below the rate of growth for housing prices.

“The housing market is proving more resilient to that tight policy than it generally has in the past,” notes Neel Kashkari, president of the Minneapolis Fed, in an essay published on Tuesday (May 7). As a result, “I would need to see multiple positive inflation readings suggesting that the disinflation process is on track” to favor rate cuts, he said at a conference yesterday.

The challenge for the central bank is to set policy at a time when housing-prices remain resilient while economic growth is slowing. One reason, perhaps the main reason, that disinflation momentum has stalled is due to a revival in housing inflation.

One possible warning sign is that the housing prices are again rising faster than the shelter component in the consumer price index in year-over-year terms.

The challenge is exacerbated by the imbalance in housing supply and demand. “Housing is a real problem in the United States due to a huge shortage of affordable housing, and in part because of high interest rates,” US Treasury Secretary Janet Yellen tells Bloomberg News. “That said, I strongly believe — I think it is highly likely — that shelter costs, which have been pushing up inflation, will come down.”

For the moment, there’s no sign that Yellen’s belief is translating into hard numbers.

More By This Author:

Communications, Energy Are 2024’s Sector Leaders For US StocksWas April’s Correction Noise Or Signal For Global Markets?

Will US Economy Stabilize In Q2 After Two Quarterly Downshifts?

Comments

Log in or sign up to join the conversation.