US Trade Deficit Boosts Growth Outlook

$49.4bn US trade deficit for February 2019

Trade boost for 1Q GDP

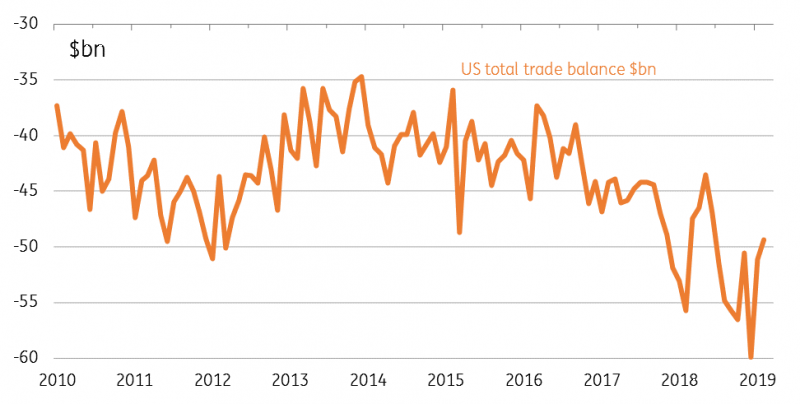

The US trade deficit narrowed to $49.4bn in February, the best reading since June 2018. This is $1.752bn less than January, with imports growing just 0.2%MoM as exports increased 1.1%, led by a 4.3% jump in auto exports. This comes after an $8.8bn decline in the US trade deficit in January resulting primarily from a 3% MoM drop in imports.

The US’ trade position had deteriorated sharply through the latter part of 2018, which we attribute largely to US firms ramping up imports from China ahead of anticipated tariff increases from 1 January 2019. The tariffs were postponed in mid-December by President Trump, but businesses could not have known that would happen and given the time it takes to ship products across the Pacific, they had unsurprisingly ordered fewer imports for January and February.

We suspect there will be a renewed deterioration in March, but with inventory levels looking reasonably high we expect it to be modest. In any case, this better than expected trade situation creates a really good platform for 1Q GDP growth. The Atlanta Fed GDP Now model based on data released up until last week points to 2.3% GDP growth for 1Q19, but today’s trade figures means 2.5% is looking achievable.

US monthly trade deficit (US$bn)

(Click on image to enlarge)

Source: Bloomberg, ING

But twin deficits to weigh on dollar

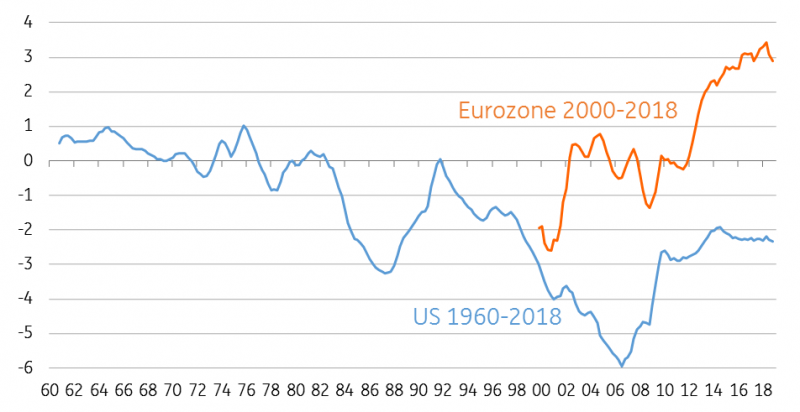

The improvements in the US trade balance in the first two months of the year suggest a decent chance of a narrowing in the current account deficit that hit $138.4bn in 4Q18. As a proportion of GDP, it could edge down to 2.2% of GDP in 1Q19 from 2.3%, which isn’t bad relative to recent history.

However, thanks to President Trump’s expansionary fiscal policy - through both aggressive tax cuts and spending increases - the fiscal deficit is soon going to be up at 5%. When combining the fiscal and the current account balances together the 'twin deficit' issue is a clear headwind for the US dollar. Europe has a large current account surplus and a far more modest fiscal deficit and in an environment where both the Federal Reserve and the ECB are signaling little prospect of interest rate rises.

Our FX team look for EUR/USD to hit 1.18 by year-end.

US & Eurozone current account deficits (% of GDP)

(Click on image to enlarge)

Source: Bloomberg, ING

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more

So we can't afford to buy Chinese stuff, and that means we are in growth mode?