Image Source: Pixabay

The US economy grew at a faster than expected 2.8% annualized rate in the second quarter and core inflation was also a little hotter than expected. The economy is facing more challenges in the second half of the year and with the Fed sounding more relaxed on the path ahead for inflation, we expect a growing focus on activity to deliver rate cuts from September.

GDP and inflation beat expectations

We’ve had a pretty solid set of US activity numbers today, but it isn’t having a major impact on market expectations for rate cuts, which are increasingly being seen as a done deal. GDP grew an annualized 2.8% in the second quarter of 2024, a little above our 2.5% forecast and more so against the 2% consensus figure while the core PCE deflator, the Fed’s favored inflation measure, rose 2.9% annualized versus the 2.7% expectation.

This latter figure, which is an improvement on the 3.7% jump in the first quarter, implies that tomorrow's month-on-month core PCE deflator will be 0.28% MoM, which seems unlikely based off the inputs from CPI and PPI so we suspect it will also involve upward revisions to the previous couple of months – originally reported as 0.26% and 0.08% MoM – but would still generate numbers consistent with delivering 2% year-on-year inflation over time.

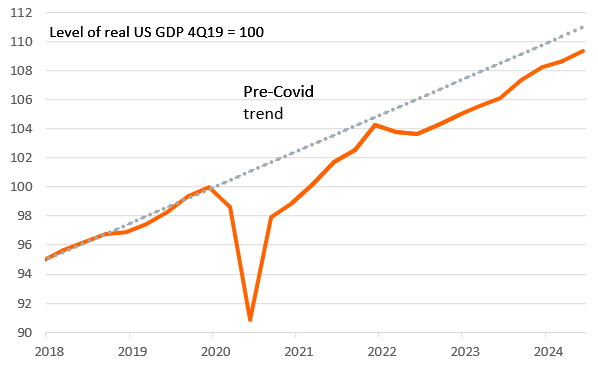

Level of real US GDP versus pre-pandemic trend

Source: Macrobond, ING

Second-half 2024 to experience slower growth, weaker inflation and rate cuts

In terms of the GDP detail, consumer spending rose 2.3% versus 1.5% in the first quarter, but this is still well down on the 3% rate averaged through the second half of 2023. Equipment investment jumped 11.6% after a very weak run with government spending increasing 3.1% and the increase in inventory building contributing 0.82 percentage points to the headline growth rate. On the negative side residential investment contracted and net trade subtracted 0.72pp from GDP growth as imports outpaced exports yet again. This is a decent rebound after the first quarter’s subdued growth of 1.4%, but the challenges for the economy are building.

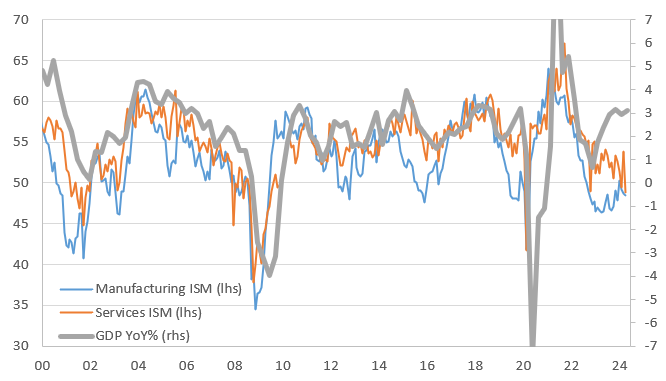

Business surveys are tracker much weaker versus GDP growth

Source: Macrobond, ING

Consumer spending is set to slow further in the second half of the year (weak real disposable income growth, reduced support from pandemic-era savings, rising loan delinquencies as the cost of credit bites harder and harder), while the investment climate will also be more challenging with firms looking more cautious at the outlook (weakening hiring and capex intentions, while slowing home sales points to more weakness in residential construction). Business surveys certainly point to a weakening outlook with today's numbers not swaying the market from their belief in a September Fed rate cut.

More By This Author:

Why We Still Expect A Bank Of England Rate Cut In AugustFX Daily: JPY Correction – Small, Medium Or Massive?

Does The US Have A Currency Problem, As Donald Trump Suggests?

Comments

Log in or sign up to join the conversation.