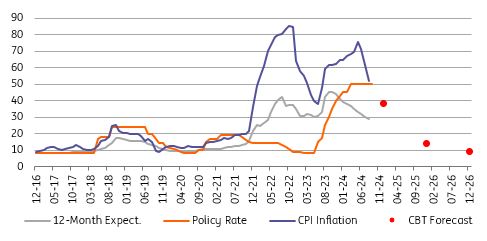

With slightly better-than-expected August inflation at 2.47%, the annual figure continues to fall, to 52% from 61.8% in July. The significant drop in the headline figure is attributable to the large favourable base effect (as it was 9.09% in August 2023) associated with food and transportation despite adjustments in administered prices. Cumulative inflation in the first eight months of this year, on the other hand, reached 31.8% vs the 38% Central Bank of Turkey forecast for this year.

PPI stood at 1.68% month-on-month, a drop to 35.75% YoY vs a month ago. The data imply moderating cost pressures with supportive currency developments (USD/TRY up by 15% on a year-to-date basis, despite an acceleration in August versus the previous months). Global commodity prices that have been broadly supportive this year will likely remain the key determinant of the PPI trend ahead.

Core inflation (CPI-C) came in at 3.0% MoM, moving down to 51.6% on an annual basis, supported by the relatively slow-moving FX basket after the local elections. While cost-push pressures are easing as evidenced by the PPI data, pricing behaviour and inertia in services have been key risk factors, adversely affecting disinflation.

Inflation outlook (%)

(Click on image to enlarge)

Source: TurkStat, CBT, ING

Regarding the underlying trend, the Turkish central bank foresees a decline in seasonally adjusted monthly inflation to around 2.5% on average in the third quarter, and slightly below 1.5% in the last quarter of the year. The August headline figure, on a seasonally adjusted basis, showed a month-on-month decline, mainly driven by the goods group (despite higher core goods), while services have remained elevated, showing no meaningful signs of improvement yet and confirming the challenges for the disinflation process.

A look at the breakdown reveals:

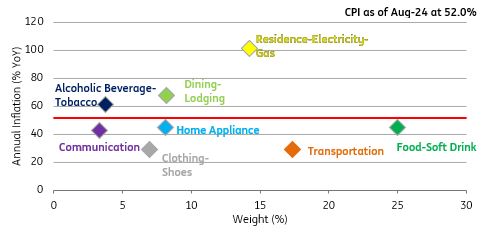

- The housing group turned out to be the major contributor at 1.31ppt as the 38% hike in natural gas prices which implies a 24.4% rise in average natural gas prices applied to households, according to the energy regulator, added around 0.6pp to monthly inflation in August. Monthly rent increases exceeding 7% in July and August with the removal of the cap (at 25% annually) also contributed to housing inflation.

- Transportation, pulling the headline up by 0.48ppt, was the second contributor, reflecting the impact of transportation services despite the price decline in oil products.

- Annual inflation in education hit the 120% level with more than an 11% monthly increase due to seasonality that will likely continue in September.

- On the flip side, food prices reduced the headline by 0.27ppt, thanks to the supportive impact of unprocessed and processed food. For the former, it was the lowest August reading in the current inflation series at 4.9%.

As a result, goods inflation moved down to 42.1% YoY, while core goods inflation, a better indicator for the trend, inched down to 28.9% YoY likely due to base effects and exchange rate-related factors. Services, which is less sensitive to currency movements but more impacted by domestic demand and minimum wage increases, fell to 77.8% YoY.

Annual inflation in expenditure groups

(Click on image to enlarge)

Source: TurkStat, ING

Overall, annual inflation continues to fall despite administrative price adjustments and no respite from services. The downtrend will likely continue as the lagged effects of monetary tightening on credit and domestic demand and the continued real appreciation of the lira will keep the underlying inflation trend on a downward path for the remainder of this year. We see end-year inflation close to the upper band of the CBT’s forecast range.

In addition, the FX deposit expansion accelerated lately as we saw a US$2bn increase in residents’ FX deposits, and $1.9bn outflows from foreign holdings of TRY assets, which resulted in a $2.5bn decline in the CBT’s net FX reserve position. Accordingly, the bank introduced a series of macroprudential tightening measures last week to contain the increase in FX demand from locals. These measures are in line with the CBT’s guidance that it will deliver additional tightening if needed. We continue to expect the policy rate to remain flat until November and at 45% by the end of the year.

More By This Author:

Rates Spark: A Week Of Decisive US Data AheadItalian GDP Growth Confirmed At 0.2% In Second Quarter

FX Daily: An Important Week For The Dollar

Comments

Log in or sign up to join the conversation.