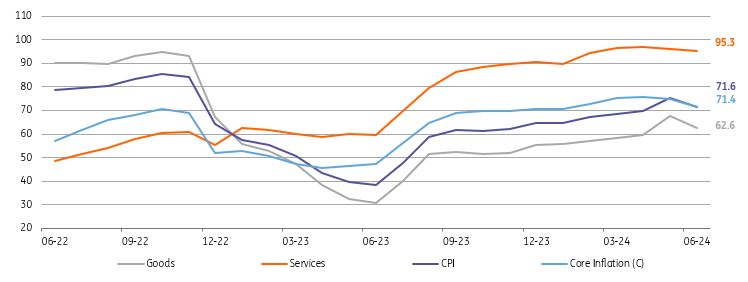

Turkish annual inflation dropped more than expected in June from its May peak, driven by both food and non-food groups. The data implies an improvement in the underlying trend.

With a lower-than-expected turnout for June (at 1.64% vs market consensus and our call of 2.2%), annual inflation in Turkey dropped from its cyclical peak of 75.4% to 71.6%. We saw 3.9% in June 2023, while the average for the same month in the 2003-based index was 0.6% – indicating that the base effect was especially favourable for this year. Cumulative inflation in the first half reached 24.7% against the Central Bank of Turkey's 38% forecast for this year.

PPI, on the other hand, stood at 1.38% month-on-month, showing a drop to 50.1% year-on-year vs a month ago, with the large base in the same month last year. The data implies that cost pressures could be moderating as currency developments have been supportive lately. Global commodity prices – which have been on an increasing path since the beginning of this year – will likely remain the key determinant of the PPI trend ahead.

Evolution of Annual Inflation (%)

(Click on image to enlarge)

Source: TurkStat, ING

Core inflation (CPI-C) came in at 1.7% MoM, moving down to 71.4% on an annual basis. This was supported by the relatively flat FX basket following the local elections (0.7% in June alone), though pricing behaviour and inertia in services have been the main factors continuing to put pressure on inflation. When it comes to the underlying trend, the CBT sees a decline in seasonally adjusted monthly inflation to around 2.5% on average in the third quarter, and slightly below 1.5% in the last quarter of the year. On a seasonally adjusted basis, the headline figure showed a marked improvement in June thanks to the goods group, and inched closer to the central bank’s forecast for the third quarter. However, the underlying trend in services has remained elevated, confirming lingering challenges in the path to disinflation.

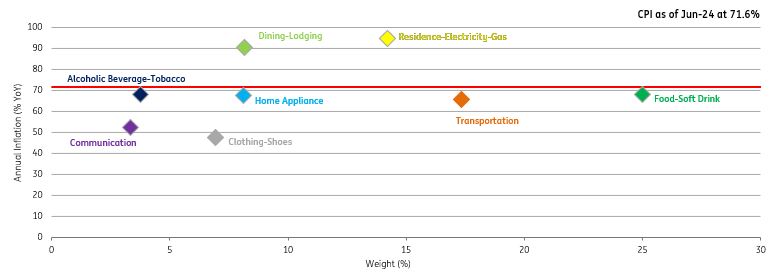

In the breakdown, the housing group turned out to be a major contributor at 0.55ppt, with a rise in water fees and continuing upside pressure in rents. Accordingly, annual inflation rose further to 94.7%. Food inflation was the second largest contributor, pulling the headline up by 0.44ppt – although the monthly outturn was lower than expected. This was largely due to unprocessed food (other than fresh fruit and vegetables) despite higher processed food inflation compared to the same month last year. Closely linked to food prices, catering services were the other key driver, lifting the headline rate by 0.28ppt.

On the flipside, clothing and transportation were negative contributors thanks to exchange rate developments, reducing the monthly figure by 0.04ppt and 0.02ppt respectively. As a result, goods inflation moved down to 62.6% YoY, while core goods inflation – which is a better indicator of the trend – inched down to 50.6% YoY. Services, an area which is less sensitive to currency movements but more heavily impacted by domestic demand and minimum wage increases, remained broadly unchanged above 95.0% YoY. This was mainly due to transportation and telecommunication services.

Annual inflation in expenditure groups

(Click on image to enlarge)

Source: TurkStat, ING

Overall, annual inflation in Turkey dropped more than expected in June from its May peak, driven by both food and non-food groups. For the remainder of the year, it's expected to drop rapidly thanks to the large base – especially in July and August. The extent of the decline will be determined by administrative price adjustments, just as we saw at the beginning of this month with a 38% increase in electricity prices. Its cumulative effect on the headline rate is expected to be around 1ppt.

In addition to a possible hike of the natural gas price, revisions in special consumption tax on certain products in the PPI release for the first half of the year is set to weigh on the pace of the decline. However, the lagged effects of monetary tightening on credit and domestic demand, together with the continued real appreciation of the Turkish lira, are likely factors that will keep the underlying inflation trend on a downward path.

We think that inflation may be close to upper band of the CBT’s forecast range at 42% by the end of 2024, assuming currency stability and no exogenous shocks. The CBT will closely watch both the inflation path and inflation expectations. We think it will maintain its tight stance with the policy rate at 50% in the near term, while keeping the funding cost and ON repo rate close to the policy rate via liquidity policy.

More By This Author:

The Commodities Feed: Tight US Inventories Support OilFX Daily: US Data And Fed Minutes In Focus

U.S. Jobs Market Reverting To Pre-pandemic Norms

Comments

Log in or sign up to join the conversation.