The latest CPI report for the United States suggests that the inflation spike after 2020 was transitory in the rather weak sense that I understood the term “transitory”. I am curling in a bonspiel over the next few days, so I do have a long time to spend on this article, so I just want to outline my thinking on the topic of “transitory”.

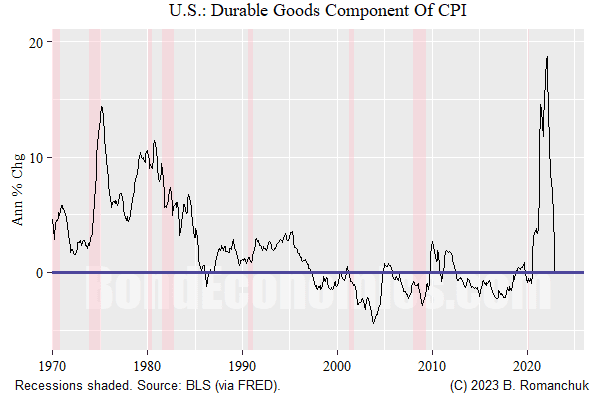

The figure above shows the annual inflation rate of the durable goods component of the CPI in the United States. The spike in the inflation rate has reversed to a roughly flat annual inflation rate. This component is somewhat cherry-picked, but I think it is a somewhat “clean” sub-component of the CPI. It avoids the construction lag of the housing component of the CPI and dodges highly erratic energy prices (which we all know about).

For me, the “transitory” nature of inflation was that after the spike subsided, inflation rates would resume at a level similar to the pre-spike levels. This is different than the 1970s. We can see the spike in the mid-1970s, and then the inflation rate stabilized around 5% — which was near the peak of the early 1970s. It then marched higher. The problem in the 1970s was not that inflation went up continuously, rather the underlying trend across cycles was higher.

Obviously, the people who argued that inflation would subside in late 2021 — which was a consensus view, including central bankers — were wrong. I certainly had some sympathies with their views — but I am not claiming to be a forecaster, and my view always was that there was massive uncertainty around the post-lockdown economic trajectory. The forecasting issue during the lockdown period was the uncertainty about firm failures — we dodged the massive failures that were possible. Once it was clear that those failures were not going to happen, it was not rocket science to predict that inflation would be perky given the supply chain disruptions.

However, I am not going to say that inflation is dead and buried — the labor market is still relatively tight when compared to the experience of recent decades. We still have “late cycle” inflation concerns, but the inflation prints are likely to remain closer to the rest of the post-1990s experience — and not the 1970s.

At this point, people will want to give central bankers credit for the turnaround in inflation. The problem with that is that this requires some selective editing of the 1970s experience — the central bankers did raise rates, the alleged problem was that real rates were negative. Guess what? In this cycle, real rates were massively negative — at least until inflation rates reversed. Even forward nominal rates were below spot inflation, so forward real rates being positive were still predicated on an inflation reversal.

I have another draft section on the recent inflation experience (for my book) in the works, and I hope to get it out relatively soon.

More By This Author:

The Difficulty Of Modelling Banking

Yield Curve Control Sustainability

Yield Curve Control Blues

Comments

Log in or sign up to join the conversation.