Image Source: Pixabay

Jobs growth beat expectations in April with wages jumping and unemployment hitting new lows. Yet, significant downward historical revisions still point to a softening jobs trend and with lead indicators and tightening lending conditions adding to the downside risks, we unfortunately expect unemployment to end the year higher than it is today.

Labor market is more resilient than expected

The April labor report shows a strong headline US payrolls figure, but major revisions really cloud the narrative on this. Non-farm payrolls rose 253k versus the 185k consensus, but there were a net 149k of downward revisions to the past couple of months spread pretty evenly between February and March. Private payrolls rose 230k versus the 160k consensus, but this "beat" was completely offset by a 66k downward revision to March (123k versus 189k initially reported).

The details show April was yet another solid month for private education & health employment (+77k). This sector has really been the strongest growth engine for jobs over the past six months, averaging around 80k per month. The government was very firm again (+23k) while professional and business services were also good, rising 43k with manufacturing and construction adding jobs after seeing employment fall last month. Temporary help employment fell by 23,000, which was the third consecutive monthly fall.

The wage story is stronger with average hourly earnings up 0.5% month-on-month versus the 0.3% consensus, resulting in the year-on-year rate of wage growth rising to 4.4% from 4.3%. This follows three consecutive 0.3% MoM prints and will keep some of the more hawkish Federal Open Market Committee (FOMC) members nervous about inflation pressures emanating from the labor market. Rounding out the numbers we see the unemployment rate dipping to 3.4% from 3.5% to match the cycle low seen in January.

But challenges are mounting

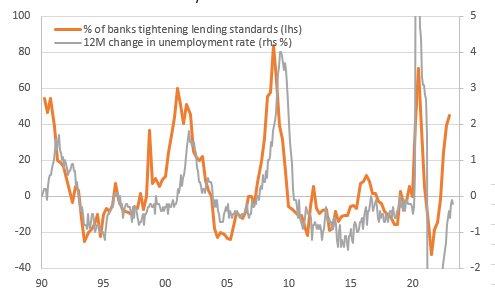

It is difficult to come up with a firm conclusion after these numbers, but we would make the point that labor market data is the most lagging of all the data and you do tend to get somewhat contradictory signals at turning points. Certainly, the lead indicators for the US economy are not pretty and the chart we keep referring to is the one showing banks tightening lending standards which always results in unemployment moving higher – banks pulling credit lines turns struggling businesses into failing businesses and unemployment climbs.

Tighter lending conditions mean unemployment will climb

Image Source: Macrobond, ING

We should get the Senior Loan Officer Survey for the first quarter of 2023 released next week and we are certain it will show banks are becoming more cautious about their lending practices given the Fed referenced this post the FOMC announcement. Recent bank stresses mean that things will be even worse today and deteriorating further in the coming months. Unfortunately, this leaves us to conclude that payrolls growth will continue to soften and unemployment will end the year higher than it is today.

More By This Author:

FX Daily: Tense Markets, But Dollar Bear Trend Should Win OutRates Spark: No Peak Rate In Europe, Not Yet Anyway

FX Daily: Transatlantic Divergence Keeping EUR/USD Bid

Comments

Log in or sign up to join the conversation.