Image by Andrew Martin from Pixabay

I’ve said it before, 2023 has been a heck of a year. In just five months, four large regional banks and one major global financial institution shuttered, marking the second-worst year for bank failures. Only the Great Financial Crisis of 2007 to 2009 (GFC) was worse. Understandably, many have tried to draw comparisons between the two periods in an attempt to contextualize today’s investment landscape. Yet, I find most to be unsatisfying. The concrete causes and potential effects of bank stress today are quite different from the GFC’s. They share only broad, systemic commonalities often omitted from discussions.

“History doesn’t repeat itself but it often rhymes.” Mark Twain’s famous quote infers that general principles hold across different concrete scenarios. Today’s market landscape is significantly different from the GFC. Banks that failed this year did so differently than in the GFC’s. Yet, they do share a broad cause. Banks in both periods suffered from breakdowns in asset liability management (ALM). However, in neither case were they individualized. Rather, system-wide centralization created the ALM problems.

Today is not the GFC

Popular comparisons of today’s bank failures and the GFC’s are, in many ways, superficial. Banks and market turmoil, alone, are not sufficiently common. They often occur together. Financial markets depict the interconnections of financial firms. The former reflects the latter’s various buying and selling activities as changes in asset prices. Thus, market volatility and financial company stress go hand in glove. They cannot be separated.

Many incorrectly blame the GFC on subprime housing. To be sure, it played a role. However, realized losses from housing-related investments did not cause the crisis. Rather, it was the broad role that housing-related investment securities played in the financial system that created the GFC. Liability surprises—not misjudged asset risks—caused the GFC.

Firms failed in the GFC due to sudden collateral shortfalls. Companies borrowed against large quantities of highly-rated structured securities. These short-term and secured borrowing arrangements provided access to cheap capital. Since financial firms are carry trades—they profit from investing borrowed money—lower borrowing costs increased their investing profits. The higher the ratings, the less collateral firms had to post, the more profitable highly-rated securities were to use in these funding schemes.

Problems only started when the Nationally Recognized Statistical Rating Organizations (rating agencies)—such as Standard & Poor’s (S&P), Moody’s, and Fitch Ratings (Fitch)—downgraded these securities. Their lower ratings triggered margin calls requiring borrowers to post additional capital to keep their lending facilities in place. However, many financial firms had none to pledge. They instantly became insolvent.

The unrealized market valuation losses on AIGFP’s super senior credit default swap portfolio increased in 2008 compared to 2007 due to significant widening in credit spreads and the downgrades of RMBS and CDO securities by rating agencies in 2008 driven by the credit concerns resulting from U.S. residential mortgages and the severe liquidity crisis affecting the markets. In connection with the termination of $62.1 billion net notional amount of CDS transactions related to multi-sector CDOs purchased in the ML III transaction, AIG Financial Products Corp. paid $32.5 billion through the surrender of collateral previously posted … [Emphasis is mine.]

American International Group, Inc. 10-K

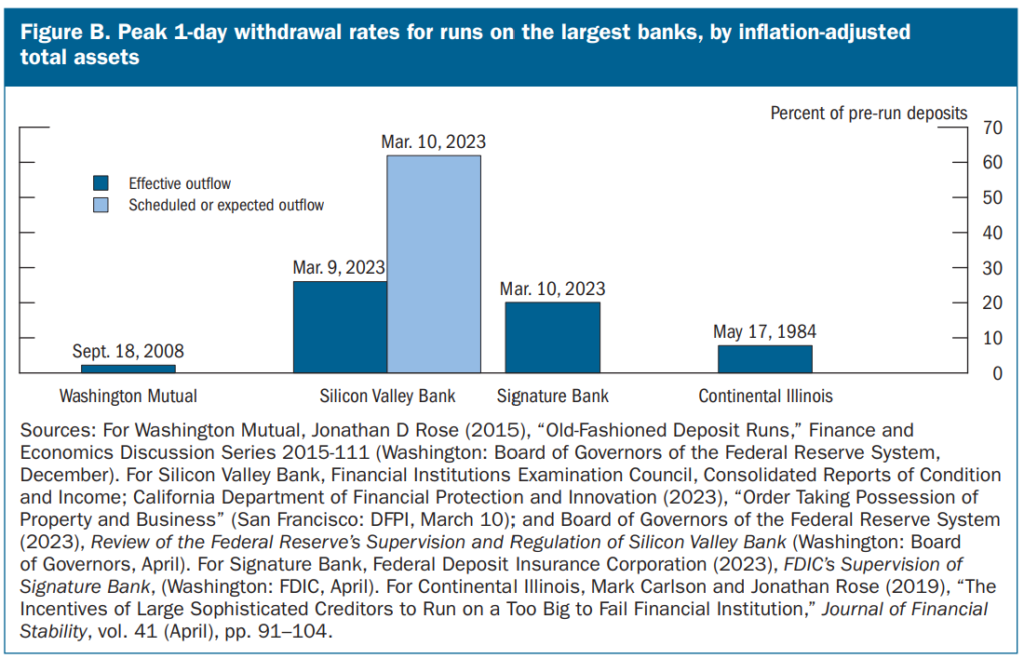

The five banks that failed in 2023 did so for other reasons. They faced large and unexpected customer deposit withdrawals. For example, Silicon Valley Bank and Signature Bank experienced unprecedented withdrawal rates of over 20% in just one day! Unable to meet those cash demands, they were forced to close. Bond ratings nor collateralized borrowing played roles. Instead, traditional bank runs killed these banks.

(Click on image to enlarge)

Silicon Valley Bank and Signature Bank experienced unprecedented withdrawal rates. Source: The Federal Reserve, Financial Stability Report

The similar principles at play

On the surface, bank failures and market consternation seem like the only attributes shared by today’s banking turmoil and the GFC. Their causes were substantially different: rating agency downgrades and deposit flight. Yet, these periods do share commonalities, just not what’s popularly discussed.

The failures in both periods were rooted in poor ALM. To be sure, no bank likely viewed its practices as deficient. After all, risk managers botched very common assumptions. In the GFC, companies believed that housing securities were rated correctly. Similarly, banks today thought they could raise sufficient cash from their high-quality and liquid securities portfolios to meet any fathomable depositor demand. Unfortunately, they were wrong in both periods. Risks surfaced and surprised these banks. These risks, it turned out, were systemic—both caused and hidden by centralization.

All corporate failures can (and should) be characterized as breakdowns in ALM. ALM is a business operation function tasked with ensuring that firms have enough cash from inflows to meet their required outflows. Ultimately, (only) cash shortfalls drive companies into bankruptcy. Management teams are generally competent. Thus, unexpected cash needs from liabilities typically cause failures, as discussed more here.

In both periods, banks faced large, sudden, and unplanned cash needs. Runs rendered them insolvent. Today’s banks did so in the traditional sense. Depositors withdrew money that banks could not deliver. In the GFC, financial firms faced runs on collateral pledged in various lending schemes. Rating agency downgrades (and declines in market values) erased security values used in secured borrowings, forcing companies to post more. Unable to meet their capital calls, they failed. Both instances exemplify poor ALM.

The GFC and today’s fragile banking environment also result from government-centralized risks. Centralization is a concept used in analyzing system stability. Specifically, it applies to the trade-offs between efficiency and resiliency. Concentrations limit options for participants. As a result, they increase the ease and efficiency with which participants can act. However, this comes at a cost. Centralization increases systemic fragility as redundancies are eliminated. For example, imagine a customer-supplier relationship. A customer purchasing all its products from a single source can benefit from volume discounts and efficient ordering processes. Yet, it also exposes the customer to its supplier’s problems. Having multiple sources can reduce supply chain risks, but would likely cost more. The customer must evaluate the costs and benefits of each option. See here for more.

The GFC highlighted the fragility created by the reliance on a few rating agencies. Regulations granted them de facto monopolies while others codified them into banks’ practices. In general, these rules penalize financial companies for holding risker—and thus lower-rated—securities.

Beginning in 2007, the three main rating agencies corrected their models’ faulty assumptions (related to the safety and correlations between housing markets). This resulted in the mass downgrades of mortgage-backed structured securities. Moody’s alone downgraded 36,346 tranches, nearly one-third of which were AAA-rated. These actions led to the collateral shortfalls described above. Regulations herded most financial companies into the same behavior.

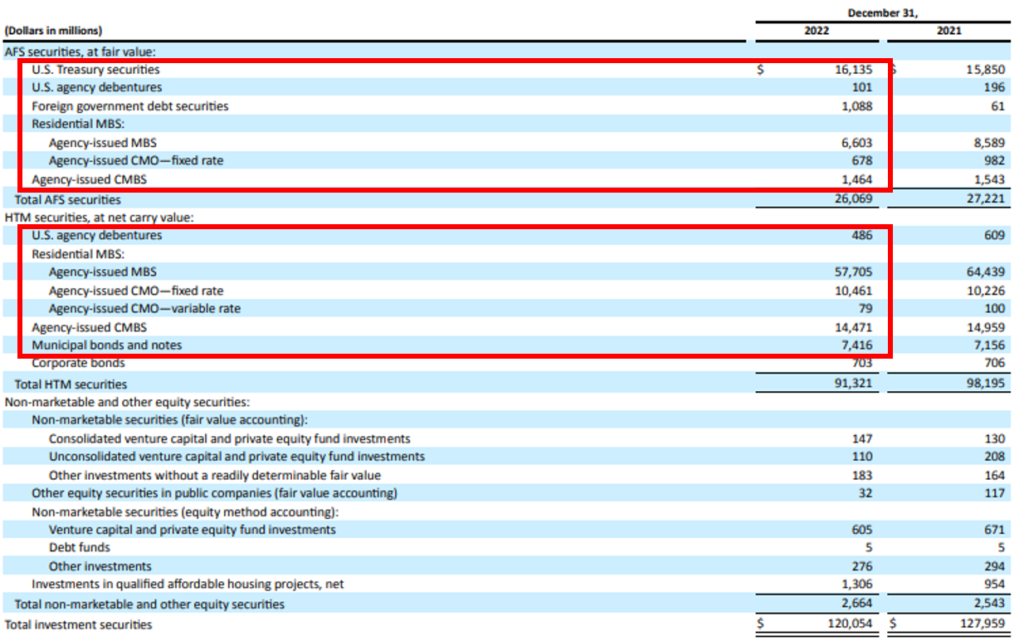

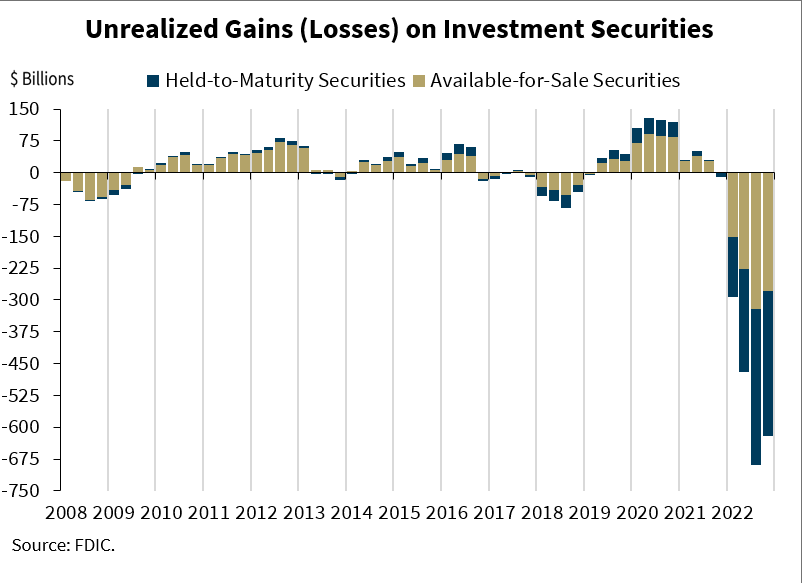

Banking regulations create another vulnerability related to interest rates, evident today. They incentivize (and require) banks to hold “high-quality” and “liquid” assets. As a result, many own large quantities of U.S. Treasury and mortgage-backed securities issued by U.S. government agencies (such as Fannie Mae). Most consider these securities riskless from a credit-loss perspective. However, their interest rate risk—a.k.a. duration—ballooned due to the protracted period of low-interest rates following the GFC. This only recently surfaced. Their prices sharply dropped as the Federal Reserve (Fed) began to raise its policy rate. As a result, banks began to amass large—though unrealized—losses in their high-quality investment portfolios.

(Click on image to enlarge)

About 97% of SVB’s portfolio was invested in high-quality government bonds (including agencies and municipalities). Source: SVB Financial Group 10-K

On their own, unrealized losses were not problems for the banks that failed. However, they became catastrophic in light of depositor flight. Needing cash for customer withdrawals, banks liquidated underwater bond positions thus realizing those otherwise-unrealized losses and blowing holes in their balance sheets. They instantly became insolvent.

Central banking turns interest rates into a systemic issue. Their sole discretion over benchmark rates exposes all investors to their decisions. Thus, central banks concentrate duration risk thereby increasing financial system fragility.

Systemic fragility raised to the fore

Today’s investing environment shares important traits with the GFC. However, large bank failures and market stresses are not them. Rather, these occurrences illustrate the broader and more fundamental risks inherent in the structure of our modern financial system. They surfaced systemic weaknesses created by centralizing regulations and laws which were (ironically) established for protection.

During the GFC, margin calls from collateralized lending facilities resulted in financial-company insolvencies. Today’s banks failed due to ordinary depositor runs. On the surface, these are very different causes.

Yet, they share important underpinnings. Both the GFC and today’s banking problems represent breakdowns in ALM. Companies failed due to their inability to meet large, and unexpected, cash outflow needs with inflows. Furthermore, centralizing regulations herded companies into similar behaviors masking the systemic nature of these risks. The GFC illustrated this with rating agencies and capital requirements. Today’s banking failures show how banking regulations and central banks concentrate duration risk.

I try to integrate my investing with my reading of the investing landscape. While I see systemic risk as high, I don’t believe it’s of the same nature as in the GFC. Thus, I’m approaching it differently, while still heeding the centralizing similarities.

More By This Author:

Hunting For Unknown Liabilities, Not Asset RisksSilicon Valley Bank’s Failure Highlights Systemically Combustible Conditions

The Fed’s Got Inflation Backwards

Comments

Log in or sign up to join the conversation.