The brief banking panic is behind us (at least until we get the next one). In front of us is a Fed on a holding pattern, and a May cut is now being questioned. As the Fed strip nudges higher so too does the US 10yr yield. The 4.25% to 4.5% area is one where it will dawn on the market that it has gone too far. But for now, there is little to object to having that test.

Image Source: Pixabay

With the banking story gone quiet, an overshoot higher in yield remains probable

The follow-through since the payroll report has been resolute. The push for higher yields in part reflects an initial reaction to the strong payrolls report, a first reaction that was in fact not that dramatic. The initial reaction took the 10yr to above 4%. The subsequent second wave has taken it back to the 4.15% area. The local high for 2024 was just short of 4.2%. It feels right to be back up here, threatening to take out that high, and making a path to the 4.25% area. The area between 4.25% and 4.5% is one where it will begin to feel like things have gone a bit too far, and one big catalyst can see us crashing back below 4%. We are just not at that tipping point yet.

The New York Community bank fall is behind us now, and the big falls in the Regional Bank Index have stalled. Until we get some clear sight of material follow-through angst in this space we move to a point where we effectively ignore the risks, just like we ignore major geo-political calamity risks (until they hit us). It leaves us with two items ringing in the ears. First, the payrolls report confirmed maintenance of a strong labor market. Second, a Fed cut in March is now a no go. These are factors forcing yields higher.

In fact, the next question is whether the Fed can cut in May – that’s now a toss up from the market’s perspective. The unwind of the May rate cuts discount and the upward drift in the Fed funds strip correlates with the ratchet higher in the 10yr Treasury yield. That can continue at least until something happens to negate it.

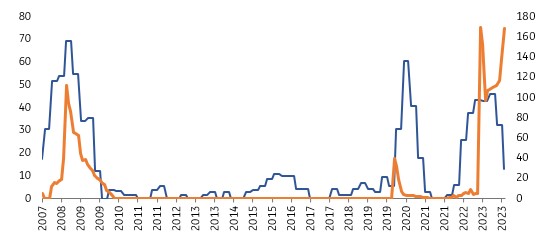

Loan Officers tightening standards (blue) versus total Fed support for banks (orange)

Less tightening than before, but actually getting tighter on aggregate...

Source: Macrobond, ING

The latest Fed’s US senior loan officers survey showed a slowing in the degree of tightening, and even though this does not mean a loosening in credit standards, it still factors in as an excuse to question dramatic need to rate cuts. A deeper analysis of the report provides a better understanding of the elevated pressures on the availability of credit (especially for lower rated borrowers), but that will be factored in more by the market when things begin to turn a bit more sour than we currently see. See more on the lending report here.

Tuesday's key data and events

It's quiet for US data on Tuesday. There will be some attention paid to the 3yr auction, which should be fine. It’s a high yielding part of the curve, and should get lots of central bank support on the buy side. From Europe, there’s mostly second tier data due, but also interesting to look at the European Central Bank’s 1yr and 3yr inflation expectations readings for December, currently running at 3.2% and 2.2% for November. Both fell significantly last time. More of that would clearly be comforting for the ECB. And eurozone supply out of the Netherlands and Austria features.

More By This Author:

ISM Services Rebound, But Continue To Track Weaker Than Official U.S. Data

FX Daily: Flip Flop

Key Events In Developed Markets And EMEA - Week Of Monday, February 5

Comments

Log in or sign up to join the conversation.