The annual increase in the Consumer Price Index (CPI) ticked up in July, after two months of big drops, revealing that price inflation might be down, but it certainly isn’t out.

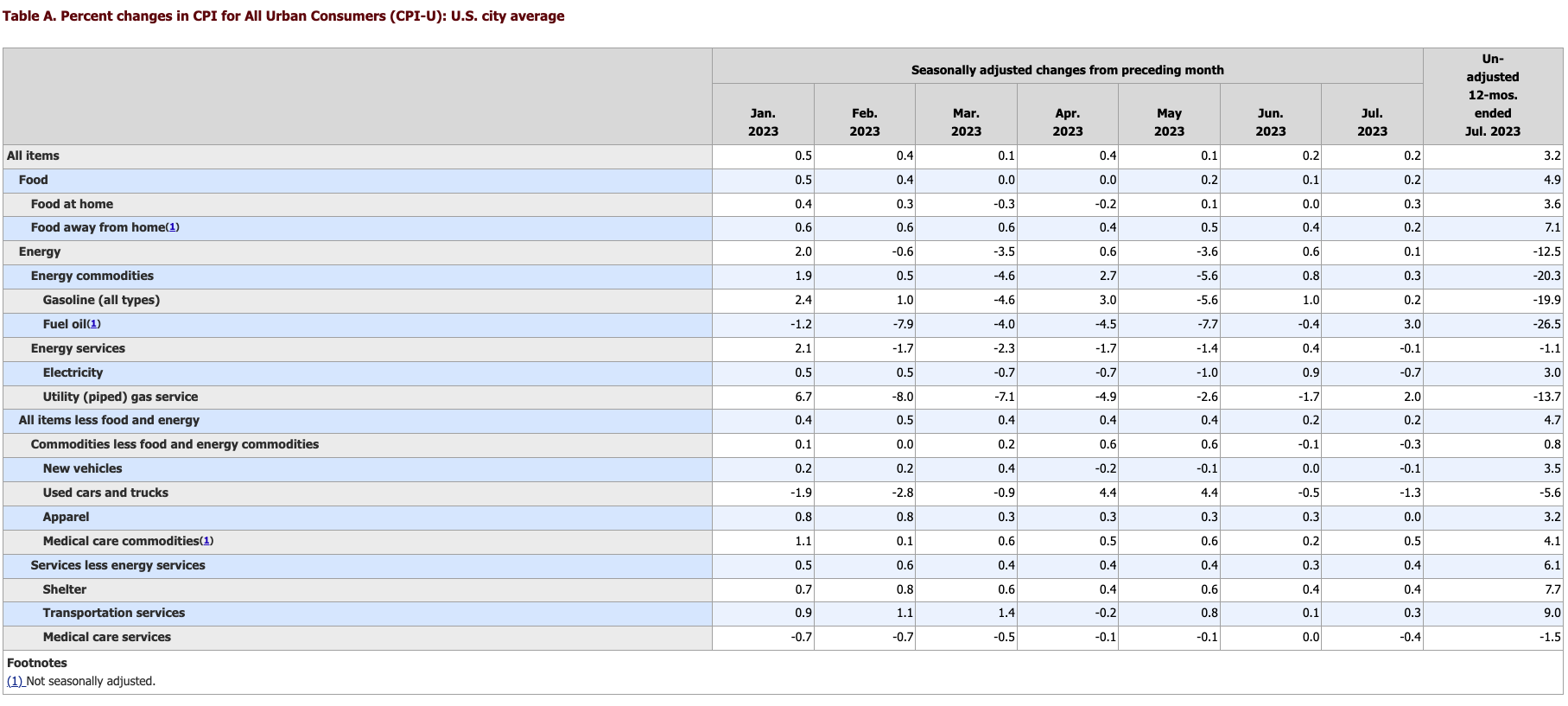

On an annual basis, CPI rose 3.2% in July, a tick higher than the 3% yearly increase in June, according to the latest data from the Bureau of Labor Statistics.

Month-on-month, prices rose 0.2%, the same pace as in June.

Stripping out more volatile food and energy prices, core CPI is still pretty hot, but continues to show some signs of cooling. Month-on-month, core CPI rose 0.2% for the second straight month. The annual core increase came in at 4.7%, down a notch from 4.8% in June.

All of the numbers were basically in line with mainstream projections.

Looking at the monthly increases so far in 2023 reveals that core CPI remains sticky, the last two months notwithstanding. On a monthly basis, it rose by 0.4% in January, 0.5% in February, 0.4% in March, 0.4% in April, 0.4% in May, and 0.2% in June and July. That averages to 0.36% per month or 4.32% annually – still more than double the Fed’s 2% target.

You will notice that all of these numbers are above the Fed’s 2% inflation target.

Keep in mind, inflation is worse than the government data suggest. This CPI uses a formula that understates the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers.

Falling energy prices continue to push overall CPI lower. The energy index decreased by 12.5% for the 12 months ending July, and gasoline prices are down 20.3% year-on-year.

But that trend is reversing as oil prices are on the upswing. Crude is now trading well above $80 a barrel and is up around 30% since it bottomed in May. It’s only a matter of time before consumers feel that pain at the pump. We’re already seeing the impact, with July prices rising 0.3% in July. In the months ahead, this bull market in oil with put upward pressure on the CPI.

The food index increased 4.9% in July over the last year. Food prices rose 0.2% from June to July.

(Click on image to enlarge)

Digging Deeper

When we got the big drop in the headline CPI number in May, we warned that it was partly a function of math and we would see it creep up again in July. That’s exactly what happened.

Keep in mind, huge 0.9% and 1.2% month-on-month increases from a year ago dropped out of the calculation in May and June, bringing the yearly headline number way down.

As we warned after the release of the April CPI data, math has now turned on the CPI calculation.

The CPI last April was 0.4% which means the drop is due to a bigger number coming off the board. This will likely play into the May and June CPI especially as 0.92% and 1.21% fall off the YoY calculation. This will greatly help the CPI YoY come down further over the next two months.”

Moving forward, the monthly increases dropping out of the calculation will be much smaller, meaning the headline annual number will not drop as quickly moving forward. And it will quickly rise with any big monthly jump in prices.

This reveals that price inflation isn’t cooling nearly as quickly as the headline CPI numbers last two months seem to indicate. The fact that core CPI is barely dropping at all further reveals that price inflation remains sticky.

Nevertheless, the mainstream perceived this CPI report as another indication that the Federal Reserve is winning the war on inflation.

Stocks surged on the news as markets anticipated the data will give the Fed the excuse it needs to end rate hikes. The markets now put the likelihood that the Fed will not raise rates in September at 90%. Many in the mainstream also seem to think that an end to tightening now means the economy can glide into a soft landing and avoid a recession.

But most people have a memory that goes back about four weeks. They forget that the Fed stopped tightening around this same interest rate in 2006. By 2007, the central bank was already cutting rates. It wasn’t until 2008 that the economy finally collapsed.

In other words, the Fed has already done enough to pop the bubble economy. The financial crisis it already kicked off continues to bubble under the surface, and it’s only a matter of time before something else in the economy breaks.

The Fed’s rate hikes and modest balance sheet reduction have succeeded in tightening credit and cooling the economy. This has taken some of the upward pressure off prices. We see that in the CPI data. If the Fed could stay this course indefinitely, it might be able to eventually beat price inflation down. But 5.5% interest rates and a small reduction in the balance sheet aren’t enough to counteract nearly 15 years of artificially low-interest rates and a more than $7 trillion expansion of the balance sheet since 2008.

And the Fed can’t stay on this course indefinitely in an economy addicted to easy money.

This is why I keep saying cooling inflation is transitory. The moment the economy collapses (and maybe even before), the central bank is going to go right back to artificially low interest rates and quantitative easing — in other words creating inflation.

In reality, the end of the inflation problem today means the beginning of a new inflation problem tomorrow because the Fed hasn’t addressed the root cause – an economy addicted to easy money.

More By This Author:

Another Recession Signal: Plunge In Demand For Gold In The Electronics SectorDebt Chickens Are Coming Home To Roost

Australia Ratcheting Up War On Cash

Comments

Log in or sign up to join the conversation.