January retail sales exceeded expectations, indicating that Polish consumers are more willing to spend on durable goods compared to 2024 when households were frugal despite a strong increase in real disposable income. Savings accumulated in 2024 should support consumption growth this year despite slowing wage growth and lower indexation of pensions.

Retail sales of goods increased by 4.8% year-on-year (YoY) in January, surpassing ING's forecast of 2.0% and the consensus estimate of 1.5%. This follows a 1.5% YoY rise in December 2024. Seasonally adjusted data indicates a 0.6% month-on-month (MoM) growth in sales.

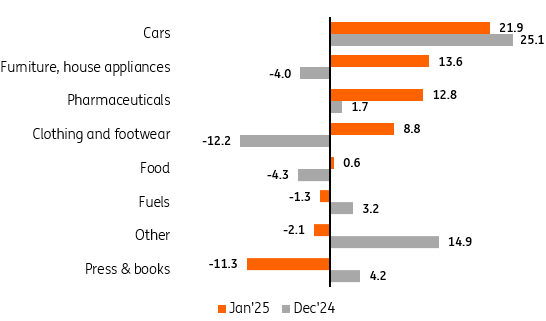

After a surprising downturn in September, likely due to floods, consumption began to recover. January showed particularly encouraging signs with a rebound in durable goods sales, which had been declining throughout 2024. Sales of furniture, electronics, and household appliances surged by 13.6% YoY in January, following a 4.0% YoY decline in December. Clothing and footwear sales also saw an 8.8% YoY increase, compared to a 12.2% YoY drop in December. Pharmaceuticals sales experienced high growth, rising by 12.8% YoY, up from 1.7% YoY the previous month. Car sales remained buoyant, growing by 21.9% YoY. However, food sales remained subdued with a 0.6% YoY increase, likely due to rising prices.

Sales of durable goods improved in January

Retail sales of goods (real), %YoY

(Click on image to enlarge)

Source: GUS.

The start of 2025 has shown promising signs in retail and a resurgence in household purchasing activity. January's data suggests a positive outlook for private consumption in the first quarter of 2025. However, we remain cautious in our forecasts for 2025 due to slower growth in real disposable income, driven by slower wage growth, lower pension indexation, and higher inflation.

Maintaining the consumption growth rate observed in 2024 will likely require households to tap into their savings from last year. We estimate that consumption growth could accelerate to 3.5% year-on-year (YoY) in the first quarter of 2025, up from 3.2% YoY in the fourth quarter of 2024, with GDP growth expected to be 3.0% YoY compared to 3.2% YoY, respectively.

More By This Author:

FX Daily: Euro Welcomes German Election ResultAsia Week Ahead: Japan Inflation Intrigue And Bank Of Korea Rate Decision

Eurozone PMI Shows Little Relief From Stagnation Just Yet

Comments

Log in or sign up to join the conversation.