December US manufacturing and industrial output data beat expectations and with upward revisions to November and lead surveys pointing to ongoing improvements there might finally be signs of a turn in the sector. Nonetheless, tariffs will present challenges for those with international supply chains and significant export exposure.

| 0.9% MoM |

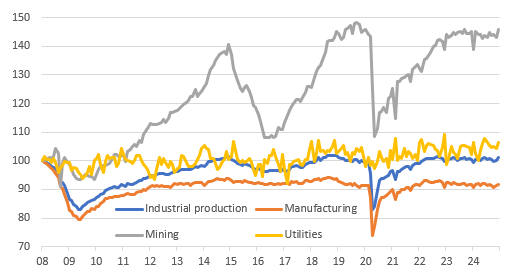

December US industrial production |

| Higher than expected |

Encouraging data point to an upward turn in US industry

US industrial production jumped 0.9% month-on-month in December versus the 0.3% consensus while November's growth rate has been revised up to +0.2% MoM from an initially reported -0.1%. The component breakdown shows manufacturing grew 0.6% after an upwardly revised 0.4% in November with utilities output up 2.1% and mining up 1.8%.

Hours worked in the goods producing sector had fallen 0.3% MoM according to last Friday's jobs report, which explains why economists had expected a weaker outcome, but the ISM report had suggested that new orders and production had finally returned to growth. The ending of the Boeing strike did help by boosting aerospace output by 6.3% MoM and there were also decent gains for apparel & leather (1.2%). Elsewhere the report was more mixed with machinery output, motor vehicle, furniture and miscellaneous production all falling.

Industrial output component levels (2008=100)

(Click on image to enlarge)

Source: Macrobond, ING

Awaiting President Trump's trade plan

Nonetheless, for now, year-on-year industrial production is only up 0.5% and manufacturing still flat on the year so we are only in the very early stages of a potential shift in trajectory with trade policy a key determinant of what may happen next. President Trump's threat of tariffs should help make US manufacturing more price competitive on the domestic stage, but exporters will remain wary of reprisals from foreign governments and global supply chains for US producers will also be vulnerable to the threat of protectionism. Markets will be keenly awaiting for signals on how aggressive President Trump will be after Monday’s inauguration.

More By This Author:

Czech Producer Prices Rise As Agriculture Drives Food Costs Higher

FX Daily: All Eyes On Monday’s Inauguration

Asia Week Ahead: BoJ Decision And GDP From Korea And Taiwan

Comments

Log in or sign up to join the conversation.