<< Read More: Is The US Facing A Slow(er) - Moving Recession Threat? Part II

<< Read More: Is The US Facing A Slow(er) - Moving Recession Threat? Part III

Several usually reliable indicators in recent months have warned of elevated recession risk for the US, but so far the economy has proven resistant to the darker forecasts that are bubbling in some quarters.

Recent nowcasts of the first quarter gross domestic product suggest that recession risk is still low. Ongoing strength in the labor market and consumer sector is on the short list of reasons why several forecasters have been surprised.

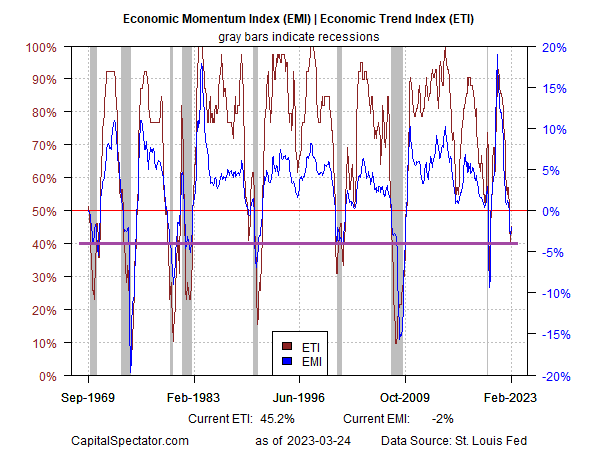

CapitalSpectator.com’s proprietary business cycle indicators have been warning of elevated recession risk, but so far those warnings have been surprisingly premature and may prove to be blatantly wrong. At the core of the challenge is the assumption, first made several months ago, that the fall of the Economic Trend Index (ETI) and Economic Momentum Index below their tipping points (50% and 0%, respectively, signaled the start of an NBER-defined recession. That was a reasonable view based on decades of history. But as recent events remind us, history is an imperfect guide to real-time economics analysis. (Note: ETI and EMI are comprised of 14 indicators that capture a broad measure of US economic activity and are included in the weekly updates of The US Business Cycle Risk Report.)

Consider the recent slide in ETI and EMI below their tipping points. In previous declines below these marks, a recession soon followed, if one wasn’t already in progress. The difference this time is that while ETI and EMI fell below their tipping points, the slide stalled.

Note that ETI and EMI decline below 50% and 0%, respectively, in previous years and continued to relatively low levels. By contrast, the descents to date have been moderate (purple line) and, more recently, given way to a slight rebound.

This behavior is unusual – nearly unprecedented, in fact, for ETI and EMI’s history since 1969. Rising recession risk, in other words, suddenly faded and deteriorating conditions gave way to a revival in economic strength.

Although ETI and EMI continue to hold below their tipping points, it’s significant that they haven’t fallen further and reached depths that previously marked troughs during recessionary conditions.

The question is whether the recent downturn in economic momentum is a temporary soft spot in an otherwise ongoing expansion — or the start of a slower-moving recession that eventually takes its usual toll. Both scenarios are plausible. Deciding which will prevail will require more incoming data.

In tomorrow’s follow-up I’ll take a closer look at the underlying data sets that comprise ETI and EMI in a bid to handicap where we go from here.

More By This Author:

Softer But-Still Resilient Growth Expected For US Q1 GDP

Trend Profiles Revive Outlook For US, Big-Cap And Growth Equities

Global Markets Rallied Last Week, Except For Property Shares

Comments

Log in or sign up to join the conversation.