Headline inflation in February inched slightly lower, still remaining below the upper limit of the central bank’s tolerance band. However, we still see two rounds of reflation this year, mainly driven by base effects.

Food prices in Hungary have risen by a mere 0.2% MoM, bringing the annual food inflation rate to the lowest level seen post-Covid

| 3.7% |

Headline inflation (YoY)ING estimate 3.7% / Previous 3.8% |

| As expected |

Disinflation is slowing as favourable base effects evaporate

Inflation in Hungary continued to fall in February, with the Hungarian Central Statistical Office (HCSO) reporting a lower inflation rate than the market consensus. This matched our own expectations exactly. Compared with January, headline inflation fell by 0.1ppt to 3.7% year-on-year, bringing inflation a little closer to the central bank’s 3.0% inflation target.

The monthly repricing in February was 0.7%, matching the repricing seen in the previous month. At the same time, core inflation rose by 0.2% month-on-mont, suggesting that price pressures were markedly lower among items included in the core basket.

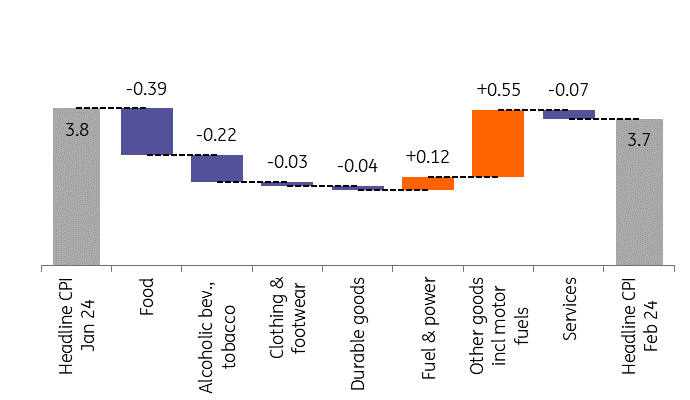

Main drivers of the change in headline CPI (%)

(Click on image to enlarge)

Source: HCSO, ING

The details

- Food prices rose by a mere 0.2% MoM, which brings the annual food inflation rate to 2.2%. This is the lowest level in the post-Covid era. On a monthly basis, both unprocessed and processed food price developments were subdued.

- Fuel prices surged by 6.7% MoM, which alone explains 0.4ppt out of the 0.7% monthly repricing for headline inflation. This is on the back of the significant excise duty increase. At the same time, household energy prices increased on a monthly basis, along with a 1% MoM rise in alcoholic beverages and tobacco prices.

- Prices of durable goods declined by 0.5% MoM in February, which can likely be explained by the easing of global inflationary pressures combined with weak external demand.

- Services prices rose by 0.6% MoM, which brings the annual services inflation rate to 10%. In terms of the annual headline inflation rate, the services component explains 71% of total inflation. This is typical at this point in the disinflation cycle, but it shows that there is still some work to be done.

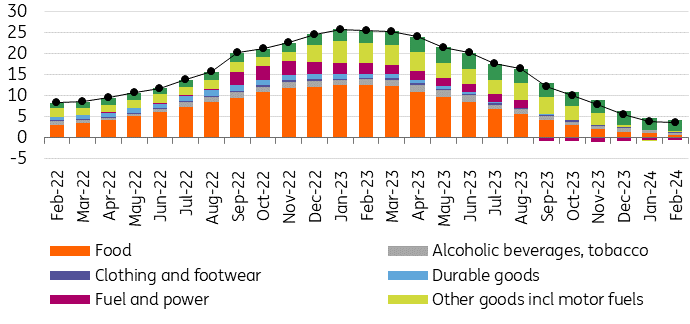

The composition of headline inflation (ppt)

(Click on image to enlarge)

Source: HCSO, ING

Core inflation drops markedly as the monthly repricing remains muted

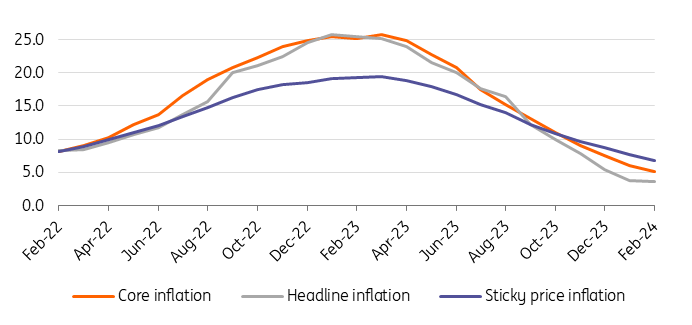

Core inflation decelerated by 1ppt to 5.1% YoY in February. The National Bank of Hungary's measure of inflation for sticky prices also decreased, displaying a reading of 6.8% YoY. This is the result of a 0.2% MoM increase in core inflation, which is completely in line with the 3% inflation target.

Price pressures in the services sector are certainly an area we'll be watching closely, especially as we expect backwards-looking price adjustments in March and April in the financial and telecom service sectors, which could mean double-digit price increases again in these areas.

Headline and underlying inflation measures (% YoY)

(Click on image to enlarge)

Source: HCSO, NBH, ING

We expect two rounds of reflation this year, driven by base effects

Going forward, we expect monthly repricing to be somewhat lower, with headline inflation hovering around 3.3-3.5% YoY in the coming months. Services inflation is likely to remain the main driver, and the rise in fuel prices should add to the monthly price adjustment. However, the generally benign inflation picture will not last too long; we expect two rounds of reflation this year.

The first round is expected to start in May and the second in October. As a result, our inflation forecast for December 2024 remains in the 5.5-6.0% range, but our point estimation is currently closer to the upper limit of the band. For the time being, however, it is indeed rather difficult to make forecasts for the second half of the year. The Hungarian economy appears to be showing a rather weak performance, as indicated by the latest fourth-quarter GDP stagnation and the incoming January hard data. On top of this, the tightness of the labour market have eased, which may put downward pressure on wage growth. Even though confidence has improved slightly, this doesn't mean that households will suddenly start a spending spree. All these factors may act as a drag on inflation in the second half of the year and therefore pose downside risks to our forecast.

On the other hand, the fiscal situation is quite worrying as growth prospects dampen, and we do not rule out the need for a fiscal adjustment in the second half of the year to achieve the 4.5% (still unofficial) deficit target. In case of adjustments, these measures could be partially pro-inflationary, as companies can pass on additional costs quite quickly and aggressively when faced with such a situation.

The macroeconomic fundamentals would indicate another 100bp cut

From a monetary policy perspective, the latest data provides the central bank with additional ammunition on the macroeconomic side to push for another 100bp rate cut at the March meeting. The combination of today's favourable inflation and core inflation data, the improvement in the external balance in January, the mixed picture of economic activity in January (which tended to show signs of weakness), and the negative labour market developments could justify maintaining the pace of easing. However, with only roughly two weeks to go before the next decision (26 March), developments in financial markets, especially in the FX market, could reshape the risk and inflation outlook and limit the central bank's room for manoeuvre.

More By This Author:

Key Events In EMEA Next Week Of March 11Monitoring Turkey: Balanced Economy Still Some Way Off

US Jobs Report Hints At A Gradual Cooling Despite A Strong Headline

Comments

Log in or sign up to join the conversation.