Federal Reserve: A Material World

No change from the Federal Reserve with a reinforced message that material change is required for them to deviate from this stance. We believe risks are skewed towards weaker growth amid a benign inflation backdrop and see the opportunity for a couple more rate cuts in early 2020.

Source: Shutterstock

Federal Reserve monetary policy unchanged

After the 25bp rate cuts in July, September, and October, Federal Reserve officials had indicated a preference to pause barring “material” changes in the economic outlook. With the latest data flow suggesting that there is little threat of imminent recession, equity markets hitting new highs and the Treasury yield curve having steepened there was next to no prospect of any change to policy this month. That is of course what we have got – a unanimous decision to leave the Fed funds target range at 1.5-1.75%.

The accompanying press release removes reference to "uncertainties" around the outlook, says that rates are "appropriate" with the FOMC stating that " the Committee will continue to monitor the implications of incoming information for the economic outlook, including global developments and muted inflation pressures, as it assesses the appropriate path of the target range for the federal funds rate".

Mission accomplished?

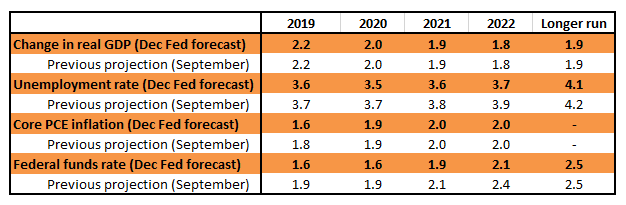

They have also provided updated forecasts which are little changed from their September projections aside from lowering their end-2019 Fed funds forecast to the current level – remember back in September they were not forecasting the October 30 rate cut. Additionally, the year-end 2019 unemployment rate forecast has been lowered to reflect the recent better numbers (see their forecasts versus September in the table below).

Federal Reserve Economic Projections

(Click on image to enlarge)

Source: Federal Reserve

It is also clear that the Fed thinks its “mid-cycle adjustment” has done its job, projecting that the next move in the policy rate will be a rate hike in 2021. We, like the market, continue to have our doubts and believe that with the US growth risks skewed to the downside and with inflation set to remain benign there remains a strong chance of further interest rate cuts in 1H 2020.

Headwinds to persist

While last Friday’s payrolls report painted a picture of a vibrant jobs market, other data suggest that the US economy is slowing. After all, capital expenditure has contracted in both 2Q and 3Q19 with the durable goods report hinting at a likely third consecutive fall in 4Q19. Meanwhile, the latest ISM business surveys softened again while the external environment remains weak with German industrial numbers and Asian trade data reinforcing this message. Given this situation, we suggest that the pace of jobs growth seen in November is unsustainable and that economic growth will moderate.

Trade tensions also remain a key issue. It may well have been that optimism after President Trump announced a phase 1 deal with China back in October gave a lift to recent sentiment and activity data. However, the fact we are now two months on and there has been no signed deal underline the message that trade remains a very challenging area.

President Trump has suggested he is prepared to wait until after next year’s election to conclude a deal while it remains unclear as to whether the proposed tariff hikes on US$155bn of consumer goods imports from China will go ahead on Sunday as planned. Uncertainty over trade seems unlikely to disappear anytime soon, which leads us to conclude that trade will remain a major headwind for growth in 2020 by disrupting supply chains, hurting profitability and damaging sentiment.

ING view: more to come from the Fed

Given ongoing trade uncertainty, weak external demand and the strong dollar we are comfortable to be on the softer side of market expectations for GDP growth (1.4% versus 1.8% consensus for 2020 GDP) and bond yields (targeting 1.4% in 1H20). Political uncertainty surrounding next year’s election could also see businesses taking a more cautious approach on expansion plans, with an emphasis on “wait and see”.

The Fed historically prefers to maintain established policy trends through elections so as to re-affirm their impartiality, but they are likely to feel much more pressure in this election cycle. If opinion polls suggest a tight contest President Trump won’t be shy to cast Jerome Powell and the Fed as the “bad guys” should growth disappoint and the Fed don’t cut rates. While this in itself is unlikely to sway the Fed, any negative feedback on market sentiment could.

As such, we suggest that if the Fed do feel as though a rate cut may be required at some point they are likely to try and move sooner rather than later to try and extricate themselves from political fallout. In any case, with inflation looking benign the Fed has the flexibility to respond to potential "material" weakness so we continue to see the potential for two 25bp rate cuts in 1H20.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more