The Czech manufacturing PMI for June dipped below the previous month’s reading and market expectations. The upward trend has been broken, with the supply side still struggling.

Manufacturing unable to break through amid weak foreign demand

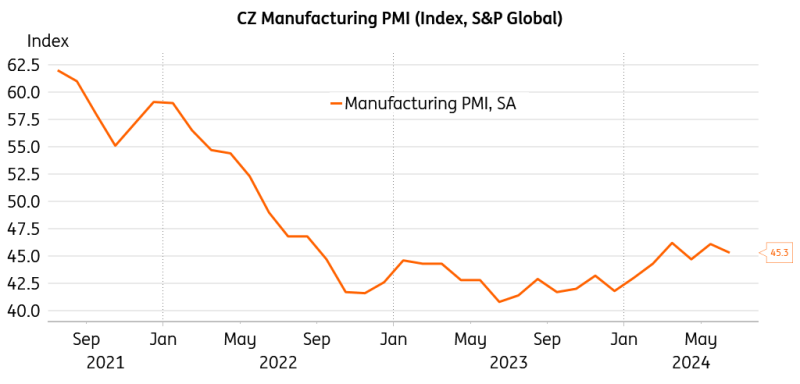

The Czech Republic's manufacturing PMI dropped lower within the contractionary area to 45.3 in June, breaking the positive trend observed in the first quarter. The PMI suggests that operating conditions in manufacturing have now deteriorated for 25 months in a row, and the production side of the Czech economy can't seem to gain a convincing lift off. The weak output performance was accompanied by a substantial reduction in employment, which points to considerable uneasiness amid signs of spare capacity. Challenging demand conditions in domestic and foreign markets are reported as the driving force of such malaise.

Upward PMI trend is broken

(Click on image to enlarge)

S&P Global, Macrobond

Tepid economic conditions in key export markets were reflected in declining new orders from abroad. The pace of contraction was, however, the second slowest seen in more than two years. Previous optimism has faded, with manufacturers seeing the worst yearly outlook since February.

Costs on the rise with pass-through limited by price competition

Costs along the supply chain have increased at the strongest pace in a year. However, producers did not fully pass these costs into selling prices. Price competition plays a crucial role in times of fading demand.

The continued weakness in PMI reflects the overall fragile recovery at home and in the economies of key European export partners such as Germany. With export-driven engines being crucial for propelling Czech growth, a hiccup in the expansion of main trading partners represents a serious risk to this year’s output. Our growth outlook for the Czech economy remains relatively conservative at 1.1% this year and 2.2% for 2025.

More By This Author:

FX Daily: French Politics Can Still Cap The EuroThe Commodities Feed: US Drilling Slows

Hungary’s Labour Market Continues To Improve

Comments

Log in or sign up to join the conversation.