Coronavirus Helicopter Money

I write this letter early Friday morning after a week in New York visiting with many fellow market participants. And lots of phone calls, both to analysts and medical experts. I had originally planned a completely different letter but circumstances changed.

Humility is a good thing to have when you’re forecasting the economy or markets. You never know what relevant facts you might be missing, so it’s best not to be too confident.

In my annual and decade forecasts, published just two months ago, I said recession probably wouldn’t happen this year, absent an exogenous event. Now, thanks to COVID-19, I am far less confident in that forecast. We have an exogenous event underway that might change everything.

Today we’ll consider where this is all headed and what could happen—not medically (others can address that) but economically. The coronavirus could take us all someplace we really don’t want to go.

Policy Shocks

Some of my libertarian friends like to say the best thing the government can do is nothing. I believe there are some things only governments can do. One of them is respond to viral epidemics. So far, the government response has been, let’s just say, not up to par. That finally seems to be changing.

The Federal Reserve injected some $600 billion into the market yesterday and promised a great deal more. The analysts I trust have reached a consensus that US rates will soon be near or at the zero bound. All well and good in a financial or business cycle recession, but that’s not what we have today. We have a biological pandemic (the WHO has finally begun to use that word) that is clearly changing consumer behavior patterns. Low-interest rates and easy money are not going to change those patterns.

I am a believer in the free market and individual decisions. I don’t blame anyone who decides it is in their best interest to stay home and avoid crowds. That is their own personal decision. However, the collective decision of many consumers to reduce their activities has the very real probability of causing a recession soon.

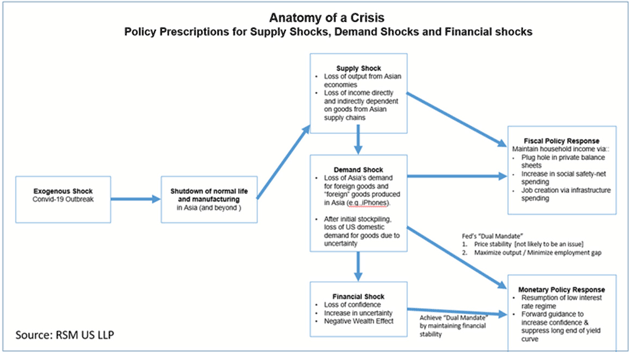

RSM economist Joseph Brusuelas produced a handy flowchart showing how these situations tend to evolve (click the link below for a larger image).

(Click on image to enlarge)

Source: Real Economy

We have three different shocks underway.

The supply shock will become more visible in the coming weeks as the Asian export pipeline runs dry, with unpredictable but possibly widespread effects on US businesses.

The demand shock is already hitting as travel slows, people avoid large gatherings, and consumers reduce discretionary spending.

The financial shock is well underway in the markets, as you are probably aware. The last few weeks brought volatility we haven’t seen in a long time.

The response to all these shocks is both monetary (central banks) and fiscal (governments). The monetary side is quite limited in what it can do. Interest rates are already near zero and below zero in some places. Plus, easier credit doesn’t address the problem. Cheap financing won’t speed up the supply chain or make people want to travel again. Nor will it help corporate earnings if customers aren’t spending.

In this scenario, the policy response is mostly fiscal. When Milton Friedman talked about “helicopter money,” he was referring to central banks, but governments have helicopters, too. And the engines are revving up everywhere coronavirus strikes.

In China, the central bank has avoided macro stimulus measures but Beijing and local governments show little restraint otherwise. They are cranking up all kinds of infrastructure projects and subsidizing businesses to pay workers for the containment periods. Banking regulators are letting small businesses delay debt payments. Some are also being exempted from social insurance taxes for the next few months.

Hong Kong is simply giving away cash, with every adult set to get the equivalent of $1,285. I suspect this is about more than virus relief, though. It might also reduce some of the recent protests.

Japan is allocating trillions of yen to subsidize workers who were forced to stay at home, often with children whose schools the government closed. Small companies will get zero-interest loans. Prime Minister Shinzo Abe promises more is coming, too.

In hard-hit Italy, Prime Minister Giuseppe Conte says he will deliver “massive shock therapy” to an economy that, in theory, should be practicing fiscal austerity. That era seems to be over. The government is planning a debt moratorium, including mortgages. How they will do that in one of the world’s weakest banking systems, and still stay in the eurozone, is unclear.

The ever-flexible European Union is preparing to relax limitations on “state aid” its members can provide. They may (shudder) even create a “coordinated” fiscal stimulus package.

Will the US do likewise? I think it’s inevitable. The Trump team and Democrats are already floating ideas. Wall Street people and various industry leaders are practically begging for help. The pressure will only grow as more companies lose revenue and more people find themselves unable to work. This being an election year, some sort of package will pass with bipartisan support. The worse this gets, the larger it will be.

Note, all this will be on top of whatever they allocate to pay for coronavirus testing, treatment, and (eventually) vaccines. It also doesn’t count the various “automatic stabilizer” programs that will kick in as more people lose jobs and income. And it will all happen as tax revenue falls for the same reasons.

Whether or not all this helps the economy or not, it will certainly expand a federal deficit that was already set to exceed $1 trillion this year. I suspect it will end up doubling that number even if the coronavirus threat recedes soon. The politicians now have a perfect reason to spend more money and they are going to seize it. That is just how it works.

My Best Guess on the Future

As bluntly as I can put it, this is not a financial recession (yet). We are in a biological crisis and it is creating panic. Much of that panic is simply because of the “unknown unknowns” surrounding COVID-19. We know it is more contagious and it appears to be more lethal. We are not really sure how lethal, but clearly none of us want to get the virus. This is introducing an enormous amount of uncertainty into the markets and the business world, neither of which like uncertainty.

Disclaimer: The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One ...

more

Timely article. Of course real helicopter money is Fed driven and would avoid the incredible surge in bonds that fiscal stimulus creates.