Image Source: Unsplash

Today’s jobs report contained two pieces of information that suggest policy may be a bit too expansionary. First, payroll employment rose by a stronger-than-expected 272,000. (The household survey was weak, but that data is viewed as less reliable). Second, nominal wages grew at 0.4% (an annual rate of nearly 5%). If you think in terms of the Fed’s dual mandate, both data points slightly tilt things toward the view that policy is too expansionary. That doesn’t mean that we can be certain that policy is too expansionary, just that this claim is now a bit more likely to be true.

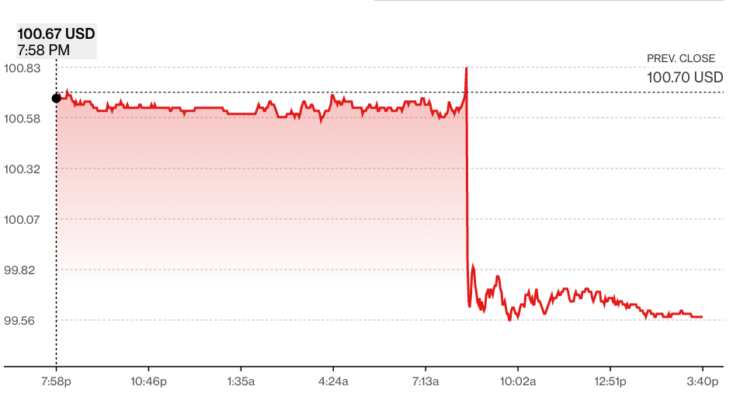

The 10-year T-bond market reacted with a sell-off, which means that longer-term interest rates increased:

Markets currently anticipate a Fed rate cut later this year. This might occur because inflation declines, or because the real economy is in danger of sliding into recession. Today’s news made both of those outcomes seem a bit less likely. Wage inflation has averaged 4.1% over the past 12 months, a rate that is not consistent with the Fed’s “price stability” goals, even if you define price stability as 2% inflation. Over time, wage inflation tends to run about 1% to 1.5% above price inflation. Unfortunately, progress on reducing wage inflation seems to have stalled over the past 10 months. The next two or three readings will be very important.

I do not have strong views on where the Fed should set its interest rate target at the moment. I do have strong views on past monetary policy, which has been far too expansionary over the past three years. The longer these policy overshoots last, the stronger the case for switching to a level targeting policy regime, where the Fed would commit to make up for previous policy errors. I had thought they intended to do that back in 2020, but it turns out that “average inflation targeting” was not an accurate description of their new policy regime.

This post is entitled “double trouble”, even though the payroll employment figure can be regarded as good news. The figures are trouble for a Fed that seems to be hoping that they will soon be able to lower their target interest rate. In my view, it’s a mistake for the central bank to root for lower interest rates, just as it was a mistake for the Fed to prefer higher interest rates back in 2015. They should not favor either lower or higher interest rates; they should favor macroeconomic (nominal) stability. Let the market decide what sort of interest rates are consistent with macro stability.

PS. This comment in the FT caught my eye:

Jason Furman, a former administration official now at Harvard University, said the uptick in joblessness could be the most important part of Friday’s data release.

“If we wake up next month and the unemployment rate is 4.1 per cent, I think that will get [the Fed’s] attention,” Furman said. “If you have an unemployment that is above 4, that would put a rate cut in play earlier.”

In the 1970s, the Fed assumed that a rising unemployment rate was a sign that money was too tight. That was not the case. The Fed should never target the unemployment rate, as no one knows exactly what the natural rate of unemployment is at any given moment in time. The Fed should target a nominal variable, preferably nominal GDP. It’s often true that rising unemployment is a signal that easier money is needed, but not if NGDP is growing at 5%.

More By This Author:

Lessons From A Non-RecessionA Glimmer Of Hope?

Double Vision: When Then Was Now

Comments

Log in or sign up to join the conversation.