The Erosion of Risk Trends Via S&P 500 Paired Against the Uncomfortable Stoicism of VIX

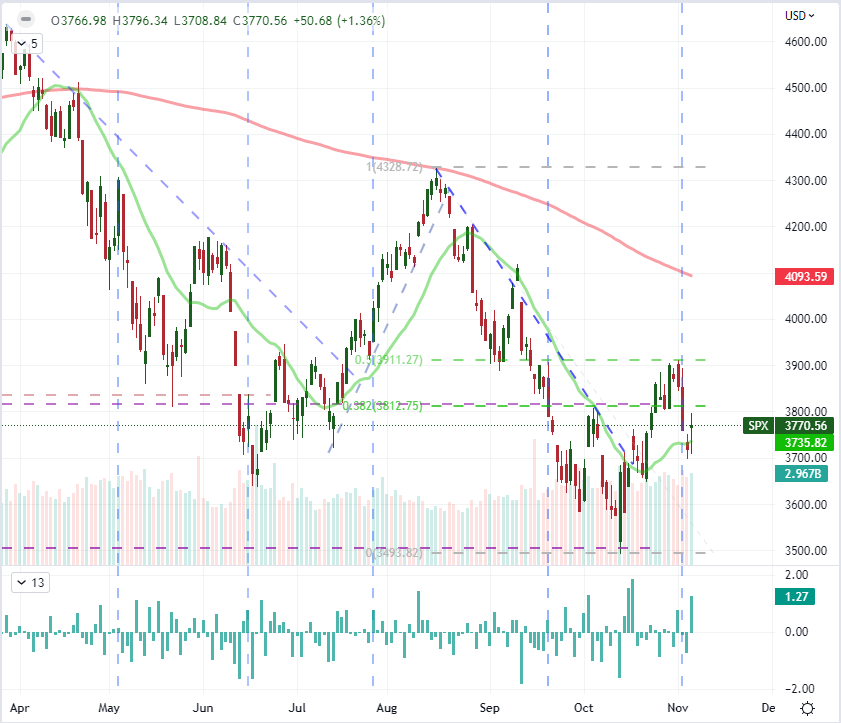

The Federal Reserve managed to extend the market’s anxiety rather than offer the relief many were expecting after various peers throttled back on their inflation fight. While Chairman Powell and other Fed members speaking soon after the fourth 75 basis point (bp) rate hike was announced were making the effort to throttle back expectations for further ‘front loading’ of monetary policy – big rate hike in other words – the warning that a longer regime of tightening would take its place was quick to follow. Whether or not that is an improvement in course or not for risk trends remains to be seen, but the seasonality may be a market force that shores up the bias for bullish drift. Notably, this past week, the S&P 500 (my preferred, imperfect measure of convenient ‘risk’ update) ended with a Friday rally following four days’ slide. That said, the overall week rendered a slide that reversed from the midpoint of the August to October bear leg. I don’t see enough here to suggest conviction is solidifying among the speculative rank.

Chart of S&P 500 with 20 and 100-Day SMAs, Volume and 1-Day Rate of Change (Daily)

(Click on image to enlarge)

Chart Created on Tradingview Platform

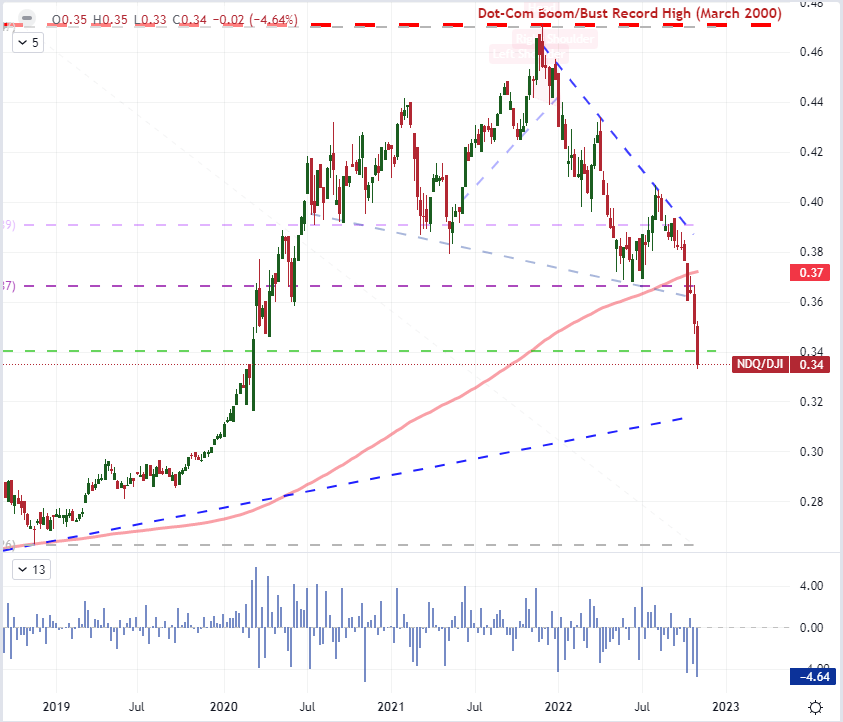

While the benchmark S&P 500 is essentially chopping in a range established over the past weeks between the broader bear trend of 2022 and the ever-persistent pressure of speculative hope, the internal dynamics of risk appetite continue to erode. I believe it is important to look at sentiment through both breadth and depth. Looking for sentiment through a wider picture; global indices seemed to firm up relative to the S&P 500 through Friday while emerging market, junk bonds and even carry trade firmed. That is a very tentative jog higher and it comes notably with very limited fundamental backdrop for the larger market participants to draw from, but the anticipation will be building with the additional seasonal expectations around the 45th week of the year and November overall. Meanwhile, I continue to monitor the falling out of favor of the benchmarks treated as the torchbearers for ‘risk trends’. Beyond the S&P 500 (and its many derivatives), the demand for top market cap stocks (which happen to be the tech giants in the FAANG grouping) has stood as a proxy for risk on and risk off. That is a problem considering the Nasdaq 100 / Dow ratio continued its collapse this past week.

Chart of the Nasdaq 100 – Dow Ratio with 100-Day SMA and 1-Weeky Rate of Change (Weekly)

(Click on image to enlarge)

Chart Created on Tradingview Platform

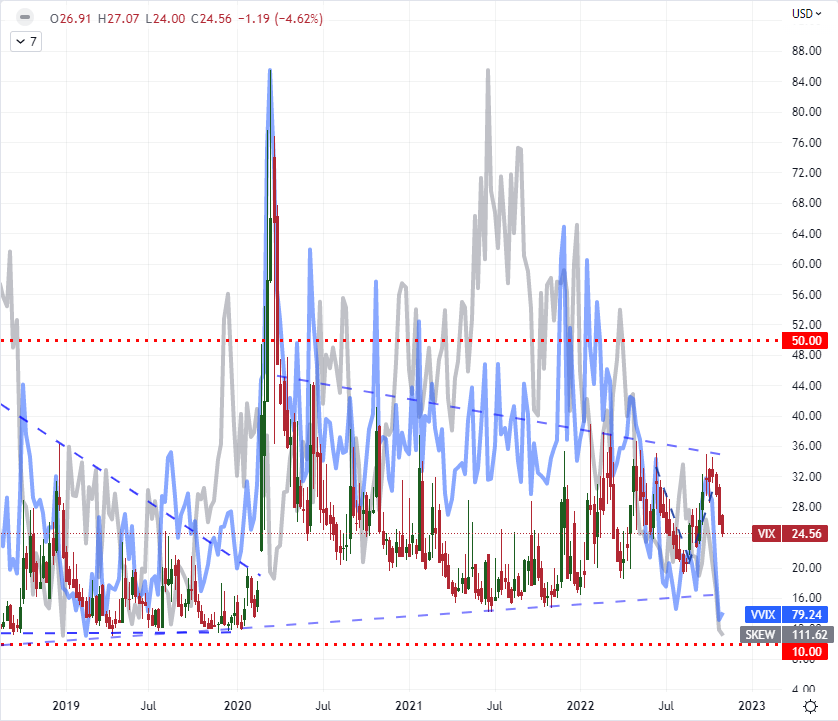

Another point of concern of mine is the seeming utter lack of effort among market participants to hedge against systemic threats like recession risks, financial crises or simply a strong reaction to the next major event (eg the US CPI on Thursday). In fact, with this past week’s underlying market volatility around the FOMC rate decision, the VIX volatility index continued its slide to account for a more than 20 percent retreat in the span of the last 20 trading days, equivalent to one trading month. We have yet to see anything that could be reasonably be construed as capitulation – something I would consider akin to a surge for or above the 50 threshold. Thus far, it has all been remarkably orderly despite the lows in the underlying. This situation alone I could perhaps suppress any serious concern around, if not for the extraordinary readings from the volatility of volatility index (VVIX) pushing a three-and-a-half year low while the SKEW tail risk measure stands at record lows.

Chart of the VIX, VVIX and SKEW Volatility Indices (Weekly)

(Click on image to enlarge)

Chart Created on Tradingview Platform

The Extraordinary Slip from the US Dollar

This past Friday’s volatility was extraordinary for a number of different reasons and markets. One such surprise came from the US Dollar. On the final day of the trading week, the DXY Dollar Index registered a -1.9 percent tumble – the worst single-day loss since December 3rd, 2015 and before that March 18th, 2009. Seven years ago, the spark for the index was the smaller than expected easing update from the ECB, leveraging the Dollar’s largest counterpart higher temporarily. With the March 2009 slump, the catalyst was an explicit 75 basis point rate cut from the Fed. I wouldn’t say anything of that same magnitude was on the radar through the end of the past week. NFPs was better than expected and thereby supports the fight against inflation, but Fed speak did remind that the policy path was moving away from large, front-loaded hikes and towards a longer path to a higher terminal rate. When it comes to the US Dollar, I consider three major factors to be a boon to the currency: its relative safe haven status, a top rate forecast through the medium term and a relatively steadfast economic forecast compared to the likes of the Eurozone or UK. That said, the run will eventually come to an end given enough time and circumstance.

More By This Author:

Bitcoin And Ethereum Forecast For The Week Of Mon, November 7Gold And Silver Technical Outlook: Modest Gains In The Cards?

Gold Prints a Triple Bottom, NFPs Could Cap Further Gains

Comments

Log in or sign up to join the conversation.