Image Source: Unsplash

The market has been running on the high-octane fuel of expected rate cuts. That belief was the engine behind Monday’s record highs, powering indexes as if the road ahead were wide open. But by midweek, the gears began to grind. Powell tossed sand into the machinery when he remarked that valuations looked “fairly highly valued.”It wasn’t a hard brake, but it was enough of a drag to remind traders the Fed isn’t blind to how stretched this rally has become—and how much it has already loosened financial conditions.

Then came the data. GDP revised up to 3.8%, jobless claims scraping the floor, and spending still firm. In the upside-down world of markets—where bad news is good and good news is bad—resilience suddenly became the problem. Strength in the economy stripped away the urgency for cuts, siphoning oxygen from the very narrative that had been propelling risk higher.

Friday’s rebound provided a reprieve. The S&P 500 and Nasdaq managed to claw back some ground, dip-buyers returned, and the week didn’t end in outright wreckage. But the bigger picture was clear: a three-week winning streak snapped, momentum lost its grip, and the rally stalled like a car spinning its wheels on slick pavement. Relief, yes. Conviction, no.

The inflation readout only reinforced that sense of stasis. Core PCE at 2.9%, headline at 2.7%, monthly inflation at 0.3%—mile markers landing exactly where the map said they would. Predictable, uninspiring, and ultimately offering traders little more than the status quo, but enough to keep two rate cut hopes alive. With no upside surprise in the data, fast-money traders simply drifted back into the very positions they had abandoned the day before—like sheepishly punching another blue ticket to reverse the pink one they’d just entered.

The Mag7 nearly stumbled too. The AI rhythm faltered, momentum names slipped, and for a moment the parade looked ragged. By Friday, though, the headliners had mostly recovered, masking the fact that the equal-weighted S&P barely budged all week. Once again, it was the generals who dictated the tape, while the foot soldiers held their ground.

Globally, fault lines widened. Europe faced labor unrest, drone incursions across the Baltic, and Macron’s fragile government stuck in another budget squeeze. Asia weathered an actual storm—typhoon Ragasa pounding southern China—yet markets there barely blinked as Alibaba pledged $50 billion into AI and teamed with Nvidia, underscoring that the global tech arms race remains the one melody investors refuse to abandon.

So we close the week still trapped in paradox. Rate cuts remain the lifeblood traders crave, but every sign of economic resilience tightens the tourniquet. Friday’s rebound soothed nerves, but gravity has not been repealed. The next release—jobs, inflation, or Powell’s next aside—could determine whether this market drifts higher on a double-barrel shot of Fed boost juice, or if there’s only one squeeze left in the tank this year and gravity then pulls the market lower.

The “New” Economy’s Funhouse Mirror: Growth Without Jobs

This week, markets were trying to square an absurd contradiction: a GDP print roaring with strength while the jobs engine at the NFP level sputters. It’s the kind of split-screen economy that leaves traders blinking, unsure which side of the tape to trust. Growth looks like it’s sprinting ahead, yet labor drags behind, as if we’ve stumbled into a funhouse mirror where reflections don’t line up and the old compass bearings no longer apply

The latest GDP revision was a thunderclap—3.8% growth, miles better than anyone expected, powered by consumers who refused to stay home. It wasn’t a trickle of data; it was a flood that re-wrote the quarter. Services surged, household spending lifted, and durable purchases rolled forward like shoppers racing to beat higher tariffs and disappearing incentives. And yet, all of this played out in the very months confidence was supposedly collapsing, payrolls were softening, and tariffs threatened to choke sentiment.

How do you reconcile those puzzle pieces? Disposable incomes were growing at a brisk 3.1% pace, financial conditions were easing as if the Fed had already swung the axe, and record-high equities made the wealthy feel invincible. The rich didn’t just spend—they accelerated big-ticket buying. Cars, travel, lifestyle services—all pulled forward. In an inflationary world, waiting is the most expensive option. Buy today, because tomorrow will cost more.

This new rhythm highlights a more uncomfortable truth: not all boats are rising. High-income households are driving the parade while the majority watch from the curb. Retail and services data show those earning above $100k are the growth engine, while those below are falling behind. It is an economy tilted toward wealth effects, asset owners, and financial winners. Narrow leadership can keep GDP aloft for a while, but it leaves the system brittle—one stumble at the top and the music stops.

And so we arrive at the central paradox. A surging economy with pockets of consumer stress. Equities at all-time highs while payroll growth erodes. Inflation still above target, credit spreads near tights, fiscal deficits yawning wide—and yet whispers grow that the Fed must rush to cut. That is the fork in the river: either policymakers see resilience and step back, or they capitulate to the labor narrative and flood the system again.

Here’s the rub. Cutting too soon while consumption is being juiced by wealth effects would be like pouring gasoline on already hot coals. Risk assets would soar further, liquidity would slosh, and inflation could return with teeth, at a time when the dragon is stirring. The bond market would not take that kindly; yields would climb, deficits would sting sharper, and the Fed’s compass would spin once again.

We are sailing in uncharted waters, where GDP can roar while jobs falter because productivity is no longer human. AI and automation have quietly reshaped the keel of the ship, allowing output to rise without labor keeping pace. The economic textbook is out of date. As Dylan said, The Times They Are A-Changin’. Traders need to stop scanning the old maps and start sketching new ones, because the landmarks have shifted.

This weekend isn’t about chasing the next tick or fade. It’s about wearing the economist’s hat, not the trader’s and staring into the funhouse mirror and asking: if GDP can sprint while jobs stumble, what does that mean for policy, for inflation, for markets built on yesterday’s models? The Fed is no longer our North Star—it is a ship itself, drifting without the charts it once relied upon. And that makes the seas ahead both more dangerous and more fascinating.

When Stars Refuse to Align: USDJPY and the October Reckoning

The yen is caught between two conflicting weather systems: the jet stream of U.S. data that keeps blowing hot, and the still-hesitant monsoon clouds of the Bank of Japan. On one side of the Pacific, GDP revisions and jobless claims have ripped through the short-dollar camp like a sudden squall, forcing traders to cover and sending the dollar surging against every G10 peer. On the other hand, Japan’s policy mandarins are staring at the Tankan survey as if it were a celestial chart, searching for the one constellation that justifies pulling the trigger on a decisive rate hike.

The positioning is precarious. Short-dollar bets are piled high, a tower of tinder waiting for the spark of another upside surprise in U.S. data. The economic surprise index is already glowing, suggesting resilience where the market had braced for softness. That puts next week’s payrolls at the very center of the stage: come in weak, and the Fed’s cutting bias reclaims the narrative; come in firm, and those short-dollar players will be forced to capitulate, lifting USDJPY like a kite into the typhoon.

At the same time, Tokyo’s own script is shifting. The July minutes read like a diary of hawks circling the roost — Tamura and Takata openly dissenting in favor of an immediate hike, others hinting they’ve had enough of “wait and see.” The Tankan, released on October 1st, is no minor report; it is the BoJ’s weather vane, catching the winds of sentiment across autos, metals, and inflation expectations. If the survey shows stabilization — or better, a modest recovery on the back of tariff relief — the argument for hesitation collapses.

That’s where politics creeps in. Japan’s ruling party is choosing a new leader, and the outcome shapes the BoJ’s room to maneuver. A moderate victory would give Governor Ueda the cover to push for liftoff at the October 30th meeting. A win for more nationalist forces would muddy the waters, complicating both Japan’s diplomatic balance and the central bank’s appetite for sudden policy tightening.

Meanwhile, the dollar’s charge toward 150 is both a threat and a gift. Break that barrier, and Tokyo is forced to respond. Intervention talk will flare, but the more durable defense lies in finally hiking — proving that Japan’s monetary anchor still has teeth. The irony is that the stronger the U.S. data, the more intense the pressure on the BoJ to abandon its caution. The higher USDJPY climbs, the stronger the case for a rate move that could slam the door on speculative momentum.

This trade is not about a single data point or election result; it is about the choreography of multiple actors moving in imperfect rhythm. The Fed’s timeline, U.S. resilience, Japanese politics, and BoJ conviction must all intersect in a narrow window. Stars aligning, or refusing to align, is the right metaphor. If payrolls undershoot, if a centrist takes the LDP crown, if Tankan steadies and Ueda finds his voice, then USDJPY will not hold above 150. The repricing of Japan’s curve will snap it back, and shorts will finally have their reward.

But that is a lot of ifs. In the meantime, every tick toward 150 is like a drumbeat of pressure — on traders, on policymakers, on the fragile balance between hope and capitulation. This is not a tape for the faint of heart. It’s a market daring the BoJ to step up, and daring dollar shorts to hang on a moment longer.

Chart Of The Week

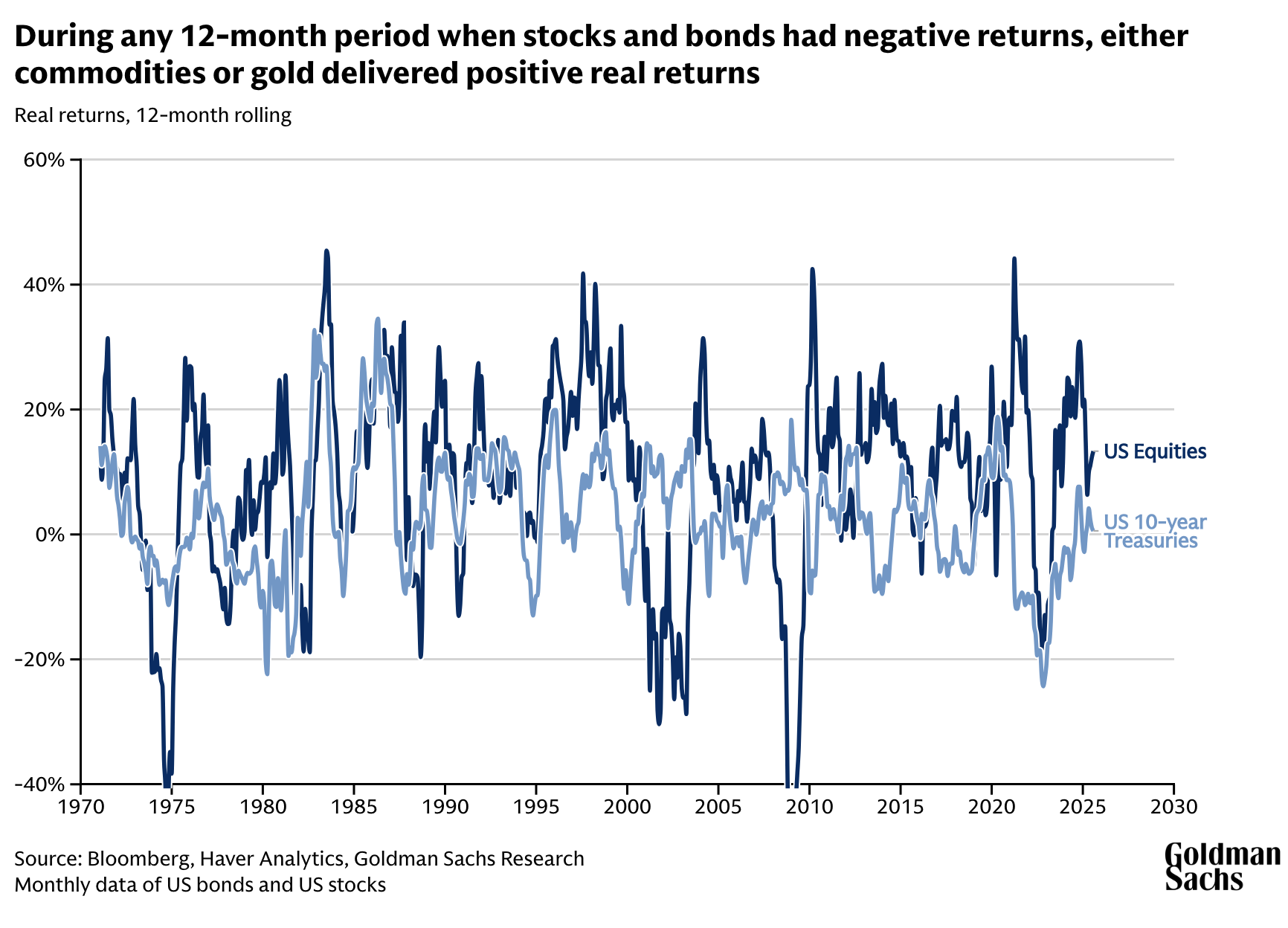

Why Investors Should Hedge with Gold and Other Commodities?

Goldman Sachs Research analyst Lina Thomas notes that in every 12-month stretch where both equities and bonds posted negative real returns, either commodities or gold managed to generate positive performance. The pattern highlights how commodities can serve as a crucial diversifier, especially in environments defined by slower growth and persistent inflation risk.

Commodity diversification can be particularly important for investors when global policy uncertainty is elevated (e.g., markets debating the central bank’s ability to contain inflation) or when the economy is hit by a supply shock (such as a sudden interruption in energy supplies).

Goldman Sachs Research also notes the increasing concentration of commodity supplies and the growing use of these resources as geopolitical leverage. This, again, highlights commodities’ part in helping investors to hedge their portfolios of stocks and bonds.

RUNNING UPDATE

This week has been a bit of a mixed bag on the running front. On the bright side, I’ve finally settled back into my Zone 2, holding effort right at the top of that band—it’s when the fun gets put back in run. The challenge has been less about the legs and more about the skies. The weather has been erratic, and today’s plan for a long run (12–15 km) was washed away by an unexpected deluge, likely the tail end of the typhoon that clipped Hong Kong. Light rain I can handle, but heavy sheets turn familiar paths into treacherous ones, so I sat it out.

The harder call, though, was deciding not to run Sam Ao on October 5. The prep was there, but a senior family member isn’t doing well, and right now I need to be closer to home. I’ll keep the rhythm going, treating a long effort on my favorite park-and-village loop as a “mock race day.” It won’t be the same, but it will keep me sharp, grounded, and in the groove—exactly where I need to be for now

More By This Author:

Euphoria To Crosswinds: Wall Street Slips Into Turbulence

Rally Hits The Pause Button As Fed Policy Confusion And AI Doubts Weigh

Powell’s Caution Clips The Market’s Wings

Comments

Log in or sign up to join the conversation.