S&P 500: The Spell of Bullish Morning Gaps Has Been Broken

Through the first half of this week, we were living on borrowed enthusiasm. Yet, the uneven climb that defies deeper fundamental hurdles may have finally hit its head on the invisible barrier of anticipation. With the economic docket next week representing an impressive density of thematic releases, it will be difficult to encourage progress on speculative appetite sans a traditional foothold. A critical slip seems to have already been registered this past session. Though there wasn’t much follow-through during the active trade of Wednesday’s New York session, the S&P 500 nevertheless opened the session with a -0.5 percent gap – quite the about-face following a series of escalating bullish gaps (including the biggest upside jump since November 2020. The correction is palpable but a conviction for the bears is not exactly confirmed. You could reference technical support – such as the 20-day SMA as former resistance new support – but it is the weight of anticipation for next week’s serious run event risk that looks more capable of capping a critical mass of conviction.

Chart of S&P 500 with Volume, 20-Day, 100-Week SMAs, and Daily Gaps (Daily)

(Click on image to enlarge)

Chart Created on Tradingview Platform

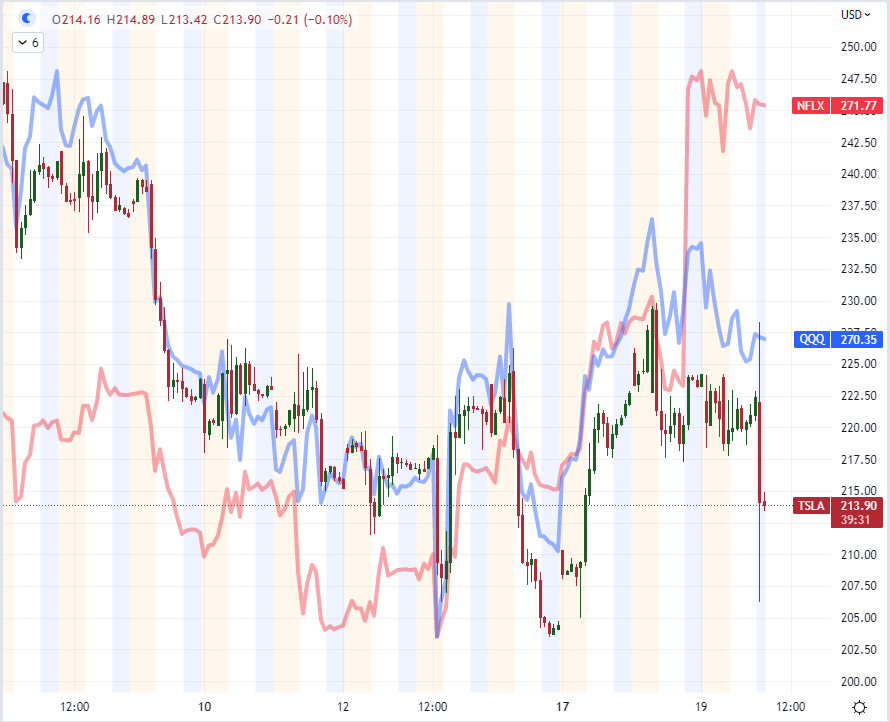

While the anticipation around FAANG earnings and US 3Q GDP next week may put the kibosh on medium and long-term trend development, for the time being, it doesn’t preclude short-term volatility. There are plenty of potential sources of volatility still unfolding. This past session’s tangible UK and Canadian CPI releases wouldn’t muster a serious Pound or Canadian Dollar response, but earnings are registering on the market’s Richter scale. The beat from Netflix Tuesday after the close ($3.10 EPS versus $2.20 expected) earned a gap higher equivalent to the after-hours trade, but nothing more meaningful in terms of follow-through for NFLX. What’s more, the Nasdaq 100 and QQQ ETF weren’t seriously moved by the performance. Should we expect anything more substantial from the Tesla report after this past session’s close considering that it would beat EPS with $1.05 vs $0.99 expected but on a miss on revenue? It is the sixth largest market cap company in the world, but the numbers and backdrop are ambiguous.

Chart of Netflix with 20 and 100-Hour SMAs with After-Hours Trade (Hourly)

(Click on image to enlarge)

Chart Created on Tradingview Platform

Dollar Strength and Other Systemic Drivers

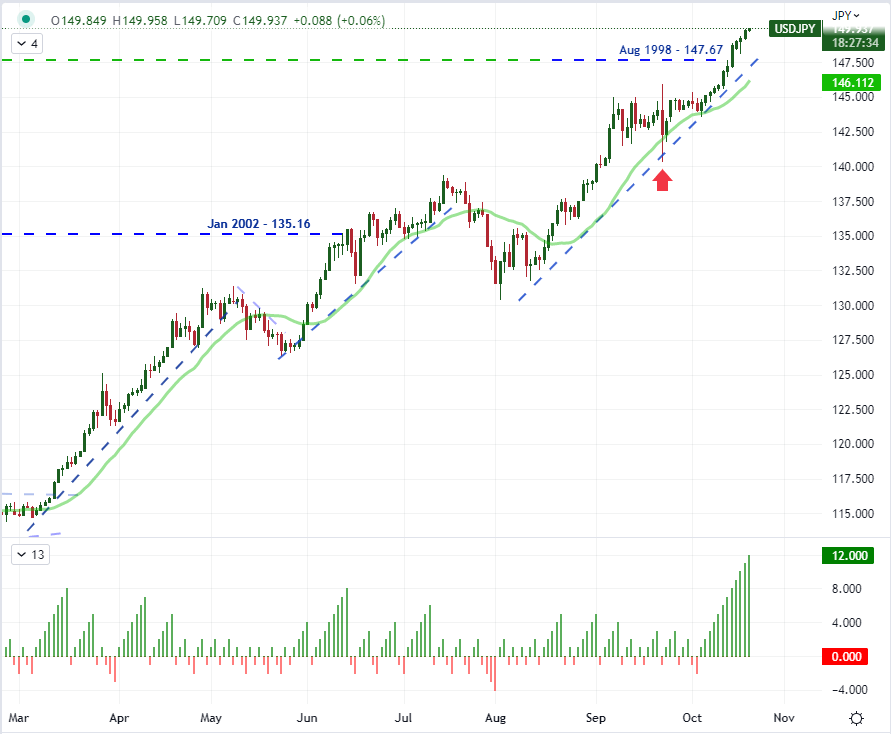

Without a stronger fundamental push in the interim, I believe it will be exceptionally difficult to push the market to a trend given the speculative gaze into the distance. If there were any source of overriding thematical pressure, it would seem that the systemically important abstractions are lurking threats. One such point of contention is the fallout from an unrelenting Dollar pressure. The DXY Dollar Index turned higher this past session, but that would bring new multi-decade lows to the likes of EURUSD nor GBPUSD. On the other hand, USDJPY has pushed to a fresh 32-year high. I don’t think the Greenback’s buoyancy was exactly necessary for this pair, but it certainly contributes through the channel of explicitly divergent monetary policy bearings, growth forecasts, and relative risk perception. The tension in this pair is extremely high from my perspective. Not only is it persisting with multi-decade highs, but the 11 consecutive session charge is the longest bullish stretch since 1973 and we are on the cusp of a loaded round figure (150) that is in absolute defiance of the wishes of the Japanese Ministry of Finance.

Chart of USDJPY with 20-Day and 100-Day SMAs and Consecutive Candle Count (Daily)

(Click on image to enlarge)

Chart Created on Tradingview Platform

Another Dollar cross that deserves a moment of reflection is USDCNH. The Dollar-Yuan exchange rate is not exactly the bastion of free-market reflection, but the balance between the two largest economies in the world carries enormous weight. That said, the cross pushed to its highest levels since early 2008 this past session which may or may not carry some degree of sanction by Chinese policy officials. There is an effort to keep the docket and newswires as passive as possible during the National People’s Congress (hence the delay in the Chinese 3Q GDP release), but this new high exchange rate isn’t truly subtle. Conspiracy theory could label this purposeful exchange rate influence to benefit an export economy, but it could also be argued that the economic outlook is taxing the key further. Amazon’s Jeff Bezos joined the fray in warning about a recession this past session, so perhaps the fear is starting to breach the membrane.

Chart of USDCNH with 20-Day SMA Overlaid with the Dow-FXI China ETF Ratio (Daily)

(Click on image to enlarge)

Chart Created on Tradingview Platform

Top Event Risk Through Week’s End and After the Weekend

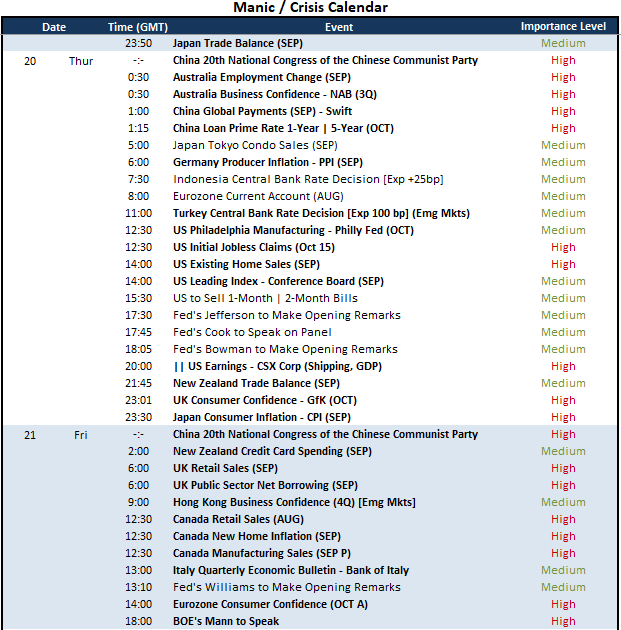

There remains considerable capacity for short-term volatility over the next few days, but my principal interest/concern is whether the market charge can override the anticipation of what will hit after the weekend. For today’s session, I will be watching capital flows in China, US housing activity reports, growth-oriented earnings (CSX), and perhaps a more focused potency or the expected Turkish central bank rate decision. There is potential for volatility for relative currencies and indices, but these don’t seem the depth charges for the broader financial system.

Critical Macro Event Risk on Global Economic Calendar for the Next 48 Hours

Calendar Created by John Kicklighter

Looking out beyond the weekend, the docket is loaded with high-profile events. Among the top listings on my calendar are: the October PMIS; FAANG earnings; US consumer confidence; the ECB and BOC rate decisions. US and German 3Q GDP and more. These are big-picture insights that lead back to questions of monetary policy potential, recession risks, and financial stability pressures. And, while the impact of this event risk can be loaded, the anticipation leading in can be even more consistent in curbing traction.

Critical Macro Event Risk on Global Economic Calendar for Next Week

Calendar Created by John Kicklighter

More By This Author:

Tesla Dips on Mixed Earnings Report, S&P 500 and Nasdaq 100 on Weak FootingFTSE 100 Stumbles to Support as UK Inflation Returns to 40-year High

Eurozone Inflation Narrowly Avoids Double Digits, ECB Next Week

Comments

Log in or sign up to join the conversation.