The USD Index (DXY shown below since 1980) above 110 today is a 20-year high not seen since April 2002.

(Click on image to enlarge)

The Euro (58% of the dollar index) is below par and at the lowest since July 2002, while the Japanese Yen (14%) is at the lowest since 1998, and the British Pound (12%) is at the lowest since 1985. The Canadian dollar (9%) at 1.3182 is the weakest against the greenback since October 2020.

Outside the dollar index, other major trading currencies are also weak. Today, the Chinese offshore yuan broke below the key 7 per dollar level last seen in July 2020. Several other Asian currencies (Malaysia and the Philippines) touched record lows today, and the Korean won hit a 13-year low.

The US dollar is the primary funding currency for global trade and financial markets, and spikes in its relative strength have historically coincided with instability and an earnings compression for US multinationals that garner some 40% of their revenues from foreign sales/currencies.

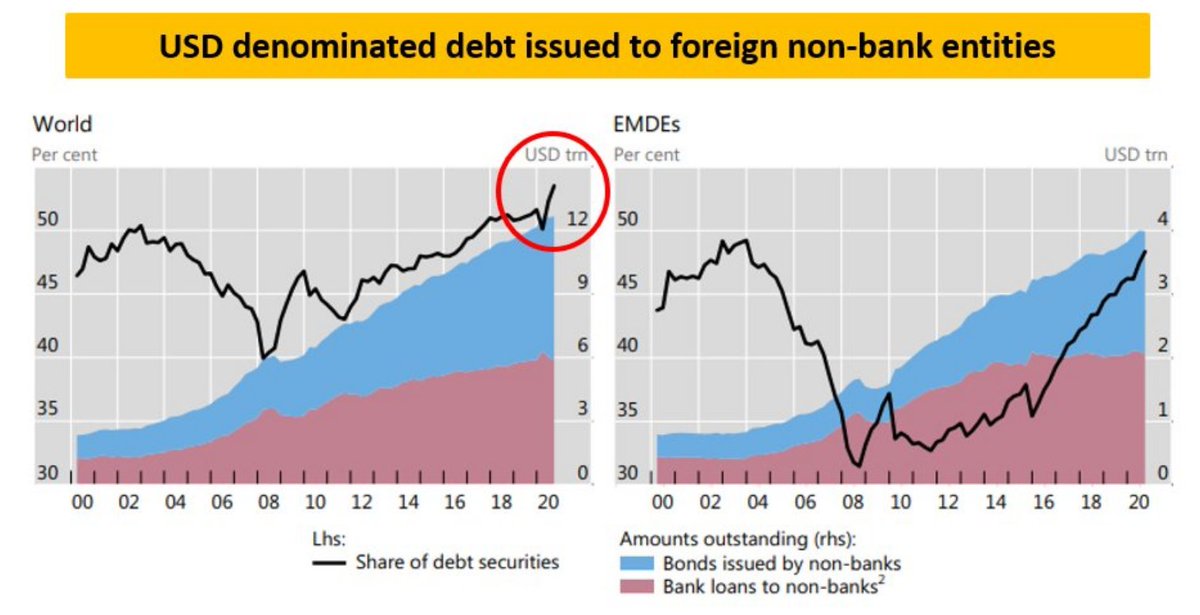

Dollar strength is disinflationary for US imports and inflationary for other economies dependent on commodity imports (nearly all priced in U$). Moreover, debt-servicing capacity for foreign borrowers of US-denominated debt drops as the dollar rises. As shown below, courtesy of macro analyst Alfonso Peccatiello, the level of USD-denominated debt globally is higher today than at any time in the last 22 years and near a 20-year high for emerging market/developing economies.

(Click on image to enlarge)

Economic downturns are self-propelling as they reduce spending and American import demand, sending fewer greenbacks into foreign coffers and intensifying the dollar cash crunch globally. Naturally, commodity demand is already tanking along with shipping rates and supply bottlenecks.

A 16% increase in the dollar index from October 1996 to April 1998 led to debt defaults in Asia and Russia. The subsequent Long Term Capital Management (LTCM) implosion in September of 1998 prompted the Greenspan-led Fed to broker a deal to backstop financial intermediaries and markets. The ‘central bank put’ has persisted through a stream of increasingly extreme central bank interventions in the 24 years since.

Far from backstopping risk markets this time, though, central banks are reacting to the late-great inflation spike of 2020-2022 with the most aggressive monetary tightening efforts in 4o years.

As the Bank of Canada hiked its policy rate to 3.25% today–up 300 basis points since March–and the highest since 2008, the Canadian dollar and Canadian Treasury yields turned lower along with Canada’s economic outlook.

Recession and job losses are set to replace inflation as the dominant concern in 2023.

More By This Author:

Quantitative Tightening Is Supposed To Step Up 5.5x This Month

Chinese Property Strife Is Contagious

Housing Has Led The Deepest Economic Contractions Historically

Comments

Log in or sign up to join the conversation.