Image Source: Pixabay

- PPI prints negative number to boost peak inflation narrative

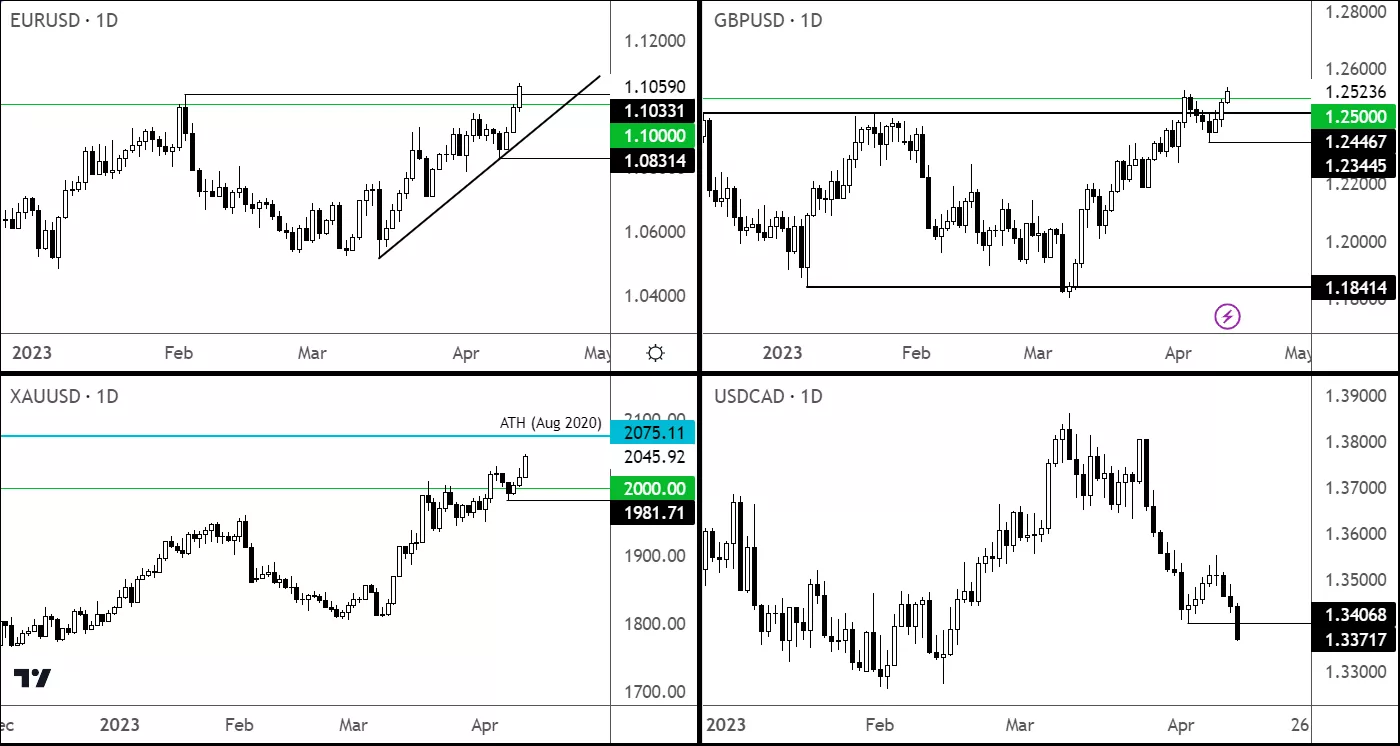

- EUR/USD above 1.10, GBP/USD above 1.25 and gold near record high

- Can US dollar rebound?

The US dollar continued to weaken on Thursday, mostly against currencies where the central bank still remains hawkish, or the economic backdrop is improving. The dollar has come under renewed pressure after more signs emerged that inflation has peaked. Traders are thus betting that the Fed will stop hiking interest rates, and soon it may even start loosening its policy again. We will have more US data in the form of retail sales and consumer confidence on Friday.

PPI boosts peak inflation narrative

Following Wednesday’s release of CPI data, investors were already feeling that we are now a lot closer to the peak in terms of interest rate hikes, now that the annual rate of consumer inflation has cooled to 5.0% and continued its sharp slide. Today, we had more data supporting this narrative as producer prices came in well below expectations. Accordingly, the odds of a 25-basis point rate hike in May have drop to 67%, according to the CME’s FedWatch tool.

- PPI -0.5% M/M, Exp. 0.0%, Last -0.1%

- PPI 2.7% Y/Y, Exp. 3.0%, Last 4.6%

- PPI Core -0.1% M/M, Exp. 0.2%, Last 0.0%

- PPI Core 3.4% Y/Y, Exp. 3.4%, Exp. 4.4%

On top of this, initial jobless claims rose to 239K when 235K was expected and following last week’s disappointing 228K print.

One more hike and done?

A growing number of analysts are expecting the Fed to either raise rates one more time before pausing the hiking cycle, or not hike at all at the Fed’s next meeting in May. Indeed, Goldman Sachs has lowered its terminal Fed target range to 5.0%-5.25% from 5.25% to 5.5%. This implies that, like most others, they see one more 25 bps hike in May but no longer predict a hike in June.

One of the main reasons why rate hike expectations have fallen so sharply is evidence that inflation is peaking. One of the biggest contributors behind the past inflation spike was rising shelter costs. But they have started to weaken like most other aspects of CPI.

What’s more, in the next few months we will see the impact of the big inflation spikes of last year come out the annual inflation measure. This means that without any further inflation setback, we will get a lot closer to the Fed’s 2% target especially if the economic output falls more significantly than expected in the months ahead.

FX majors testing big levels

Thanks to a weakening US dollar and following the release of more forecast-beating eurozone data (this time industrial production, which climbed by 1.5% versus 0.9% eyed), the EUR/USD has finally climbed above that 1.10 handle we were banging on about for days. At the time of writing its some 60 pips above that level. Elsewhere, the GBP/USD broke above 1.25 to hit its highest level since last June as it extended its gains for the 7th consecutive week. The USD/CAD, undermined by rising oil prices, dropped below 1.3400 to test its 200-day average. Gold and silver continued to push higher. XAUUSD is holding comfortably above $2K and XAGUSD is now well above $25.00 – in fact closer to $26 now.

(Click on image to enlarge)

Could the dollar find unexpected support?

In the short-term, the potential for profit-taking is there after the dollar’s extensive declines means some of the major currency pairs are technically “overbought” or “oversold,” especially given that we have some more data releases coming up on Friday.

Another factor that could possibly reverse the dollar’s trend is crude oil which remains supported after last week’s surprise OPEC decision to cut oil production sharply. If oil prices rise significantly to pose another inflation risk to the global economy, then investors might revise their expectations about interest rates again. Although, that being said, rising oil prices are also recessionary.

And yet another reason why the dollar index could find support is on the back of a potential reversal in equity markets, boosting the appeal of the safe haven dollar. So far, we haven’t seen any such signals. But the upcoming earnings season could be the trigger if company profits and revenues are weak. On tap for Friday, we are looking at earnings reports from JPMorgan, Citigroup, Wells Fargo and Blackrock.

What to watch out for, is something my colleague John Kicklighter has already written about:

These are major players with perspective on different financial segments that can upend different thematic. JPM is the 18th largest company by market cap and is considered a strong reflection of revenue and value generated through markets and trading. It also happens that CEO Jamie Dimon has been beating the fundamental drums warning that recession risks are rising and the recent financial stress – which he played a role in advising a resolution – are not behind us. Wells Fargo and Citigroup will offer a perspective on financial services effected by rising interest rates with the former still a dominant force in real estate financing and the latter drawing a bulk of its revenue from consumer banking accounts. BlackRock is more often overlooked in this macro review; but with a market cap larger than Citi’s and as the largest asset manager in the world, much can be drawn from the environment from the performance of this particular company. If revenues slipped, cash was set aside for future threats or the outlooks darken from these players given recent developments, it will not go unnoticed by the market.

US Retail Sales and UoM Consumer Confidence (Friday)

More US data is going to follow on Friday. The Fed’s rate projections have been cut sharply in recent weeks owing to weakness in US data and signs of peak inflation. Worries over the health of US consumers will intensify if we see a weaker print in either retail sales or consumer confidence, especially as they are going to feel the impact of higher gasoline prices in light of the OPEC’s decision to sharply cut crude production. Both headline and core retail sales are seen falling 0.4% month-over-month. The University of Michigan’s consumer confidence index is a more forward-looking indicator of consumer’s health and may thus trigger a sharper move in the dollar should we see a bigger-than-expected deviation from the expected 62.0 reading.

More By This Author:

Dollar Index Retreats Ahead Of Busy Week For US Data

EUR/USD Dips But 1.10 Visit Remains Likely

WTI Forecast: Crude Likely Heading Higher After OPEC+ Cuts

Comments

Log in or sign up to join the conversation.